Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

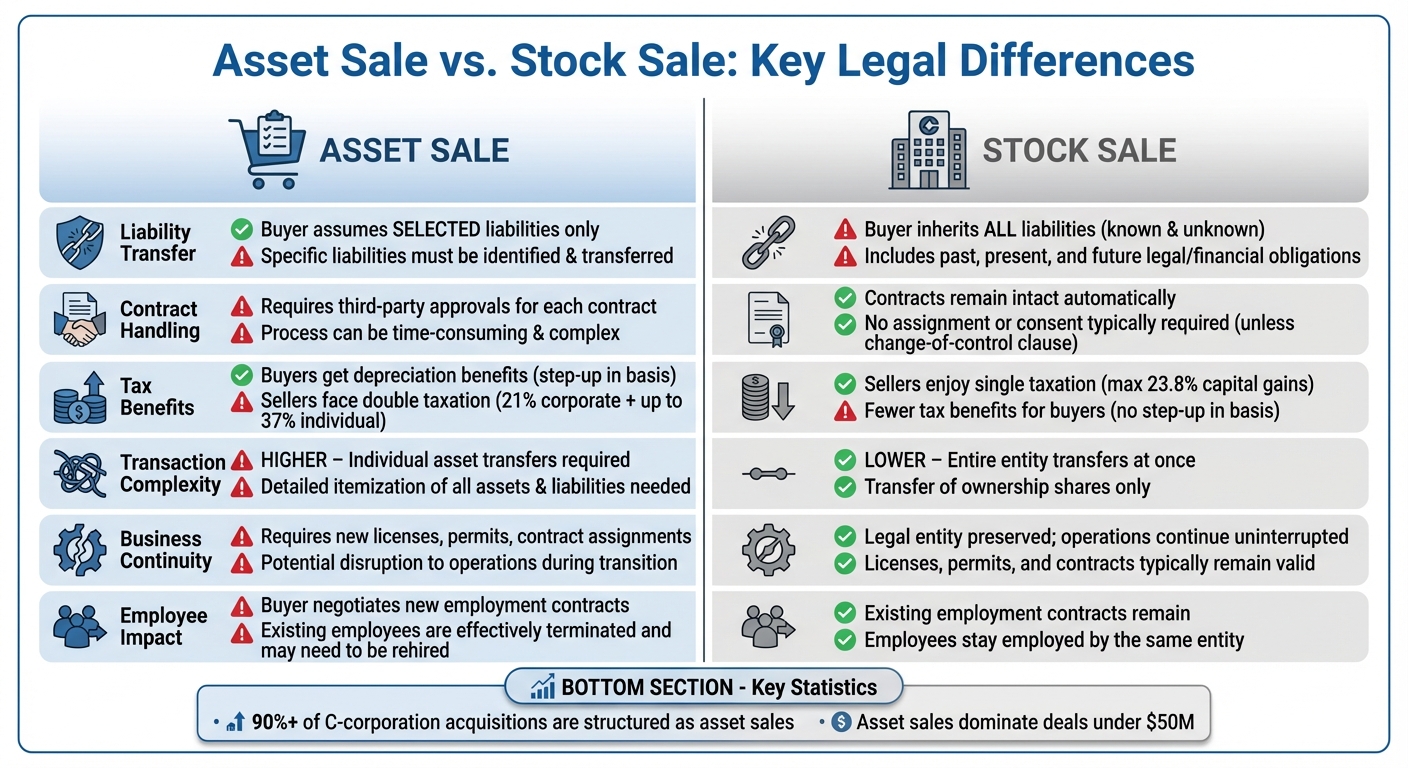

When buying or selling a business, the deal structure - asset sale or stock sale - matters significantly. It affects taxes, liability, and overall complexity. Here's a quick breakdown:

- Asset Sale: The buyer selects specific assets (e.g., equipment, inventory) and avoids unwanted liabilities. It's common for deals under $50M and offers tax advantages for buyers. However, sellers face higher tax burdens, and the process can be complex due to individual asset transfers and contract approvals.

- Stock Sale: The buyer takes over the entire company, including all assets and liabilities. This approach simplifies operations for sellers but exposes buyers to potential hidden risks. It's often preferred for businesses with hard-to-transfer assets like permits or contracts.

Quick Comparison

| Feature | Asset Sale | Stock Sale |

|---|---|---|

| Liability Transfer | Buyer assumes selected liabilities | Buyer inherits all liabilities |

| Contract Handling | Requires third-party approvals | Contracts remain intact |

| Tax Benefits | Buyers get depreciation benefits; sellers face double taxation | Sellers enjoy single taxation, fewer benefits for buyers |

| Complexity | Higher; individual asset transfers required | Lower; entire entity transfers |

| Employee Impact | Buyer negotiates new contracts | Existing contracts remain |

The right structure depends on your goals, risks, and tax considerations. Buyers often prefer asset sales for control and tax benefits, while sellers lean toward stock sales for simplicity and lower tax rates.

Asset Sale vs Stock Sale: Key Differences Comparison Chart

Stock vs Asset Sale: What To Consider When Selling a Business (with Chad Huebsch, EA, CTP)

What Is an Asset Sale?

An asset sale involves a company selling specific assets - such as equipment, inventory, intellectual property, customer lists, or real estate - to a buyer, while the seller keeps ownership of the actual legal entity. Think of it as a kind of estate sale: the buyer picks and chooses what they want, and the seller retains the corporate entity itself. This process is guided by detailed legal agreements that ensure clarity in the transaction.

One key advantage for buyers in an asset sale is the ability to select which assets and liabilities they want to take on. Attorneys Jack R. Magee and Robert E. Futrell, Jr. from Wyrick Robbins explain it well:

"A benefit of an asset sale is that it allows the parties significant flexibility as to what assets and liabilities are included in the transaction. In particular, for a buyer this provides an opportunity to reduce its risk of assuming unknown liabilities of the acquired business."

This flexibility helps buyers manage risk by avoiding liabilities they might not be aware of, while sellers benefit from a clear outline of what’s being sold.

The details of what’s included in the transaction - assets and any liabilities the buyer agrees to take on - are laid out in the Asset Purchase Agreement (APA). Typically, cash isn’t part of these deals, and sellers often hold onto certain assets, like real estate or specific intellectual property, that they don’t want to sell.

Asset sales are commonly used in situations like selling off business divisions, distressed businesses, or small-to-mid-sized companies. They’re especially appealing to buyers who want to avoid the burden of historical liabilities tied to the business.

However, asset sales can be more complex than other types of transactions. Each asset must be transferred individually, which means handling bills of sale, intellectual property assignments, and obtaining third-party consents. This process requires careful planning and can take extra time to complete .

What Is a Stock Sale?

A stock sale happens when a buyer purchases the company's shares directly from its shareholders, effectively taking ownership of the entire business. Jacob Orosz, President of Morgan & Westfield, breaks it down:

"In a stock sale, the buyer purchases the seller's entity (Corporation, LLC, etc.). By purchasing the seller's entity, the buyer then owns the assets owned by the entity."

This type of transaction streamlines the process by consolidating everything into a single deal. Unlike an asset sale, which involves transferring individual assets piece by piece, a stock sale transfers ownership of the entire company in one go.

One of the key benefits of a stock sale is that the business retains its existing structure. The company name, tax ID, contracts, licenses, and permits remain unchanged - there’s no need for separate transfers. The buyer essentially steps into the existing framework and continues operations as they were.

Stock sales are particularly useful when a business owns assets that are hard to transfer individually, such as government permits, professional licenses, or customer contracts with clauses that don’t allow for easy reassignment. Sellers also tend to favor stock sales because they can provide a cleaner exit and may come with tax advantages, especially for C-corporations looking to avoid double taxation.

However, buyers should proceed with caution. When purchasing stock, the buyer takes on everything the company owns - assets and liabilities alike. This includes any pending lawsuits, unpaid debts, tax obligations, or other financial risks that might not be immediately obvious. Stock sales are most common with corporations (C-corps and S-corps), while LLCs and partnerships typically transfer ownership through the sale of membership interests.

This complete transfer of ownership highlights the importance of understanding the legal and tax implications that come with a stock sale.

Core Legal Differences

The legal frameworks of asset sales and stock sales lead to distinct outcomes for both buyers and sellers. Understanding these differences is crucial to navigating potential challenges before they arise. These distinctions also lay the groundwork for exploring tax considerations and strategic advantages.

Liability Transfer

Asset sales allow buyers to pick and choose liabilities. In this setup, buyers can decide which obligations - like an equipment loan or a vendor contract - they want to take on, leaving the rest with the seller. Attorney Aaron Hall explains:

"In an asset sale, liability transfer is generally selective, allowing the buyer to assume only specified liabilities explicitly agreed upon, thereby limiting exposure to unknown or contingent obligations".

Stock sales, on the other hand, transfer all liabilities. When buying a company's stock, the buyer inherits all liabilities, from those clearly documented to those that may be hidden. Jacob Orosz, President of Morgan & Westfield, highlights this risk:

"A contingent liability is a liability you do not know exists, so you do not know what you are inheriting. If you purchase the stock of the company, a number of unknown liabilities could exist".

To mitigate these risks, buyers in stock sales often rely on representations, warranties, and indemnification clauses.

Contract Assignments

Asset sales require manual contract transfers. Agreements with vendors, customers, and landlords don’t automatically transfer to the buyer. Instead, they must be explicitly assigned or novated. This process can be delayed by anti-assignment clauses that demand third-party approval.

Stock sales keep contracts intact. Since the legal entity remains unchanged, contracts generally stay in place. However, some agreements may include "change of control" provisions that require consent or open the door to renegotiation. As Jacob Orosz notes:

"Many contracts have a 'change of ownership' clause that states that if there is a substantial change of ownership of the stock in the company, this is treated as an effective change of ownership, and explicit consent is required".

Thorough due diligence is essential to identify and address these clauses in key contracts.

Legal Entity Continuity

Asset sales leave the legal entity with the seller. The buyer typically forms a new entity or uses an existing one to house the purchased assets. Meanwhile, the seller is responsible for winding down the original entity and handling any remaining obligations. While this creates a clean break, it can disrupt the business's identity.

Stock sales preserve the corporate structure. The buyer takes over the entire legal entity, including its name, tax identification number (EIN), bank accounts, permits, licenses, and customer relationships. This ensures the business can continue operating seamlessly.

Regulatory Approvals

Asset sales often require new permits and licenses. Because licenses and permits usually don’t transfer between entities, buyers may need to reapply with state or local authorities. This can extend the timeline for closing the deal.

Stock sales generally retain existing permits. Since the legal entity remains the same, most permits and licenses stay intact. However, regulatory agencies may require notification of ownership changes. In some industries, additional approvals may still be necessary, and larger transactions could trigger securities or antitrust reviews.

Employee Relationships

Asset sales give buyers flexibility with employees. The seller’s employees don’t automatically transfer, so the buyer must negotiate new employment agreements with those they wish to retain. For those not rehired, severance obligations may need to be addressed.

Stock sales maintain existing employment arrangements. Employees remain under the same employer, keeping their tenure, benefits, and contracts intact. While this continuity can be appealing, it also means the buyer inherits all employment-related liabilities, such as pension obligations and accrued benefits.

| Legal Aspect | Asset Sale | Stock Sale |

|---|---|---|

| Liability Transfer | Selective; buyer assumes only specified liabilities | Comprehensive; buyer inherits all known and unknown liabilities |

| Contract Assignments | Requires third-party consent or novation for each contract | Automatic transfer; legal entity remains unchanged (subject to change-of-control clauses) |

| Entity Continuity | Seller retains the legal entity; buyer uses a new/existing entity | Buyer acquires the entire legal entity; operations continue uninterrupted |

| Regulatory Approvals | Asset-specific permits/licenses may require reapplication | Existing permits typically remain; subject to securities and antitrust laws |

| Employee Relationships | Buyer selects which employees to hire; new contracts are required | Employees remain with the entity; continuity is preserved |

These differences help explain why asset sales are more common in deals under $50 million, as buyers aim to minimize exposure to unforeseen liabilities. These legal distinctions shape decisions around liability, contracts, and broader strategies for both parties involved.

sbb-itb-97ecd51

Tax Implications

When it comes to selling a business, the tax treatment of asset and stock sales plays a critical role in shaping both tax liabilities and deduction options for buyers and sellers.

In an asset sale, buyers enjoy a significant tax advantage through what's known as a "step-up" in tax basis. This means the cost basis of the acquired assets is adjusted to their fair market value at the time of purchase, allowing for greater depreciation and amortization deductions. According to Laura Chamberlain from Exbo Group, "in an asset sale, the buyer doesn't have a 'taxable event' - a transaction that results in tax being owed - at the time of purchase". Any excess purchase price over the value of tangible assets is allocated to goodwill, which can be amortized over 15 years. This setup can substantially reduce future taxable income for the buyer.

However, for sellers, asset sales often result in a heavier tax burden. C-corporation sellers face double taxation - once at the corporate level (currently at a 21% federal rate) and again when the proceeds are distributed to shareholders. Additionally, sellers may be subject to depreciation recapture, where gains from selling assets above their adjusted tax basis are taxed as ordinary income, with rates reaching up to 37%. As Joseph R. Luna from Jimerson Birr points out, "the choice between an asset sale and an equity sale is one of the most crucial yet frequently overlooked aspects of selling a business". Because of these higher tax costs, sellers often demand a premium on the purchase price in asset sales.

On the other hand, stock sales tend to be more favorable for sellers, but buyers see fewer tax benefits. Sellers are typically taxed only at the individual level, with a maximum federal rate of 23.8% (20% capital gains plus a 3.8% net investment income tax). Buyers, however, inherit the seller's carryover basis, meaning they miss out on the step-up in tax basis and cannot restart depreciation schedules or claim new deductions. As Oren Glass, Partner at PKF O'Connor Davies, explains, "The purchase of the company stock does not allow for any 'step-up' in the tax basis of the value of the assets purchased, and so the buyer does not get additional depreciation deductions".

A potential workaround for this disparity is the Section 338(h)(10) election, which allows a deal structured as a stock sale to be treated as an asset sale for federal tax purposes. This provides buyers with the tax step-up while maintaining the legal simplicity of a stock transfer. However, both parties must agree to this election and file it by the 15th day of the ninth month after the acquisition. It’s worth noting that this option is only available for qualified stock purchases, which typically involve at least 80% of the target company's stock. It applies to consolidated groups, affiliated groups, or S corporations. Despite these complexities, more than 90% of C-corporation acquisitions are structured as asset sales, as buyers often prioritize the tax benefits even if sellers are less inclined.

This nuanced tax analysis highlights why the structure of a business sale is such a critical decision for both buyers and sellers.

Pros and Cons for Buyers and Sellers

When choosing between an asset sale and a stock sale, both buyers and sellers must weigh the trade-offs that come with each option. These differences can significantly shape how the transaction unfolds.

Buyers often prefer asset sales because they allow for more control over which liabilities to take on, leaving behind any unwanted or unknown obligations. As Shelly Garcia from Nolo explains, "In an asset sale, the buyer acquires some or all of the contents of the business... and they don't have to take on any liabilities such as loan debts". This selective process shifts the focus of due diligence to verifying asset ownership and identifying any encumbrances. However, asset sales aren't without challenges. Buyers face the logistical burden of retitling assets, obtaining consents for contract assignments, and securing new licenses or permits. These steps can slow down the process and disrupt operations.

Stock sales, by contrast, are generally more straightforward for sellers but carry more risk for buyers. In a stock sale, the buyer takes over the entire legal entity, including all of its liabilities - whether they are known, unknown, or undisclosed. Garcia further explains, "Buyers in a stock sale get the business as is, including any known or unknown liabilities. Liabilities might include debts, accounts payable, unpaid wages, and lawsuits". This means buyers need to conduct extensive due diligence on the company’s history and compliance records. On the upside, stock sales preserve business continuity, as contracts, licenses, and relationships remain intact without the need for renegotiation or third-party approvals.

Here’s a quick comparison of the two approaches:

| Feature | Asset Sale | Stock Sale |

|---|---|---|

| Liability Exposure | Limited; buyer assumes only specified debts and obligations | High; buyer inherits all known and unknown liabilities |

| Due Diligence Requirements | Focused on specific assets, their titles, and any liens | Comprehensive; covers the entire corporate history and compliance records |

| Business Continuity | Lower; requires new licenses, permits, and contract assignments | Higher; the legal entity remains intact |

| Transaction Complexity | Higher; involves retitling assets and securing third-party consents | Lower; involves transferring shares rather than individual assets |

Jacob Orosz, President of Morgan & Westfield, notes, "Asset sales dominate smaller business sales because the buyer can write up the value of the assets and depreciate the costs". This makes asset sales particularly common for businesses valued under $50 million. For stock sales, buyers often include strong indemnification clauses or hold-harmless agreements to guard against any liabilities that may surface after the deal is closed.

How Kumo Can Support Business Acquisitions

Kumo streamlines the process of finding the right business acquisition by bringing together listings from marketplaces, brokerages, and proprietary sources - all in one platform. Whether you're exploring asset or stock sales, Kumo offers access to opportunities across global markets, simplifying what can often be a complicated search.

With custom search filters, you can zero in on the deal structures that match your strategic goals. For instance, if you're looking for the tax perks of an asset sale, such as goodwill amortization, you can narrow your search to asset-heavy businesses. On the other hand, if maintaining operational continuity is your priority and you'd rather skip the hassle of retitling assets or renegotiating contracts, you can focus on stock sale opportunities where the legal entity remains intact. This tailored approach ensures your acquisition aligns with your specific needs.

Kumo's AI-powered tools take it a step further by helping you quickly identify whether a target includes specific assets or the entire entity. This feature is especially helpful for assessing liabilities. For industries with significant contingent risks, you can prioritize asset sales, allowing you to selectively acquire only the assets you want. Meanwhile, for companies with critical non-transferable permits or government contracts, Kumo makes it easier to find stock sale opportunities that preserve these essential relationships.

To keep you ahead of the game, Kumo offers automated alerts based on your preferences, such as transaction type, industry, location, or deal size. This is particularly valuable for smaller asset sale transactions under $50 million, giving you more time to focus on due diligence and negotiations.

With its global reach, Kumo provides access to a wide range of transactions across various regulatory environments, ensuring you can find opportunities that fit your preferred deal structure and risk tolerance.

Conclusion

When deciding between an asset sale and a stock sale, the choice carries significant implications for pricing, tax outcomes, and future responsibilities. As attorney John D. Perry of Ward and Smith, P.A. aptly explains:

"Whether to structure a deal as an asset acquisition or a stock sale is often a threshold issue that, once determined, can influence and inform the parties' negotiation of nearly every other key aspect of the transaction, including the purchase price."

The two approaches come with distinct advantages and challenges. Asset sales allow buyers to pick and choose specific assets, leaving liabilities behind. On the other hand, stock sales transfer ownership of the entire legal entity, including its existing obligations. Tax considerations also play a central role: asset sales provide a stepped-up tax basis for depreciation, while stock sales typically result in single-layer capital gains taxation.

Ultimately, there’s no one-size-fits-all answer. Buyers often lean toward asset sales for better liability protection and tax benefits, while sellers favor stock sales to avoid double taxation and simplify their exit. The right structure depends on various factors, such as your entity type, industry-specific risks, and whether key contracts or permits are at stake.

Before committing to a Letter of Intent, it’s essential to grasp these distinctions and work with seasoned advisors to ensure your transaction aligns with your financial and strategic objectives.

FAQs

What are the tax differences between an asset sale and a stock sale for buyers and sellers?

In an asset sale, the buyer purchases specific assets and liabilities of the business. This approach allows the buyer to allocate the purchase price across the acquired assets, resulting in a "step-up" in tax basis. This step-up can be a big advantage because it lets the buyer claim depreciation or amortization deductions over time, which helps lower future taxable income. On the flip side, the seller faces taxes on the gain from each transferred asset. Gains on depreciated assets are often taxed as ordinary income, while gains on appreciated assets - like real estate or goodwill - are generally taxed at capital gains rates.

In a stock sale, the buyer acquires the seller's shares, effectively taking ownership of the entire business, including its existing tax basis in assets. Unlike an asset sale, the buyer cannot adjust the tax basis of the assets or claim new depreciation deductions. However, the seller usually benefits from capital gains tax treatment on the full transaction, which is often taxed at a lower rate than ordinary income. These tax differences can significantly affect the financial outcomes for both the buyer and seller, so it's important to carefully evaluate which structure works best for the deal.

Platforms like Kumo simplify the process of finding acquisition opportunities, making it easier to analyze whether an asset or stock sale structure might be the better choice.

What’s the difference in liability transfer between an asset sale and a stock sale?

In an asset sale, the buyer purchases only the specific assets and liabilities outlined in the purchase agreement. Any liabilities not explicitly listed - such as long-term debt or contingent obligations - are typically left with the seller. This approach allows sellers to offload selected obligations while holding onto liabilities they prefer not to include in the deal.

In contrast, a stock sale involves the buyer acquiring ownership of the entire business entity, along with all its liabilities - both known and hidden. This means the buyer assumes responsibility for existing contracts, debts, tax exposures, and any unforeseen obligations. Because of this, buyers usually perform detailed due diligence and often negotiate protections like warranties and indemnities to safeguard their interests.

Liability concerns play a major role in determining the structure of a deal. Sellers often lean toward asset sales to minimize their liability exposure, while buyers might opt for stock sales to retain existing contracts and streamline the transfer of assets. Platforms like Kumo simplify the process by providing access to a range of asset-sale and stock-sale opportunities, helping both buyers and sellers find the structure that aligns with their objectives.

Why do buyers often prefer an asset sale instead of a stock sale?

Buyers often lean toward an asset sale because it lets them handpick the assets they want to acquire while steering clear of the business's unwanted liabilities. This approach minimizes risk by excluding any hidden debts or legal issues that might come with a stock sale.

Another major draw of asset sales is the tax benefits they offer. For instance, buyers can enjoy a step-up in the tax basis of the purchased assets, which may result in depreciation and amortization perks. These perks can help reduce taxable income over time, making asset sales not just a safer choice but also a financially smart one.