Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

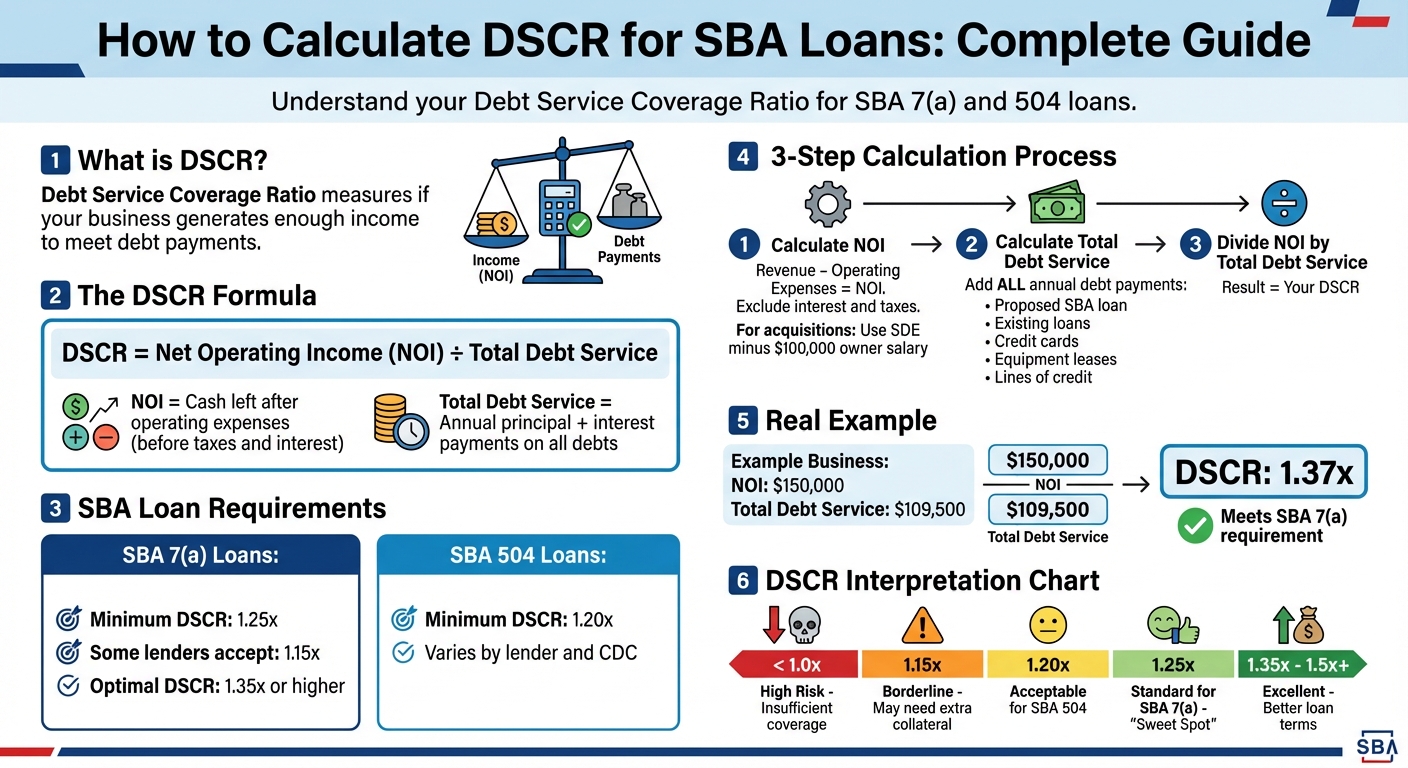

Debt Service Coverage Ratio (DSCR) is a key metric lenders use to assess whether your business generates enough income to meet its debt payments. For SBA loans, a DSCR of 1.25x or higher is typically required, meaning your business must earn $1.25 in income for every $1.00 of debt. Here's a quick guide to understanding and calculating DSCR:

-

DSCR Formula:

DSCR = Net Operating Income (NOI) ÷ Total Debt Service- NOI: Cash left after operating expenses but before taxes and interest.

- Total Debt Service: Annual principal and interest payments on all debts.

-

SBA Loan Requirements:

- SBA 7(a) loans: Minimum DSCR of 1.25x.

- SBA 504 loans: Minimum DSCR of 1.20x.

-

Steps to Calculate DSCR:

- Calculate NOI by subtracting operating expenses from revenue.

- Add up all annual debt payments (including the proposed loan).

- Divide NOI by total debt service to get DSCR.

-

Example:

- NOI: $150,000

- Total Debt Service: $109,500

- DSCR: 1.37x ($150,000 ÷ $109,500)

A DSCR below 1.0x means your business isn’t generating enough income to cover debt, while a higher ratio improves loan approval chances and may lead to better terms. Focus on accurate financial data and adjustments to ensure your DSCR meets SBA requirements.

How to Calculate DSCR for SBA Loans: Step-by-Step Guide

Understanding the Debt Service Coverage Ratio (DSCR) for Your SBA Loan

DSCR Requirements for SBA 7(a) and 504 Loans

SBA loan programs rely on the Debt Service Coverage Ratio (DSCR) as a key financial metric, but the specific requirements differ between the SBA 7(a) and 504 loan programs. These differences reflect the unique purposes and risk profiles of each loan type. Here’s a closer look at the DSCR requirements for these two popular SBA loan options.

Minimum DSCR for SBA 7(a) Loans

For SBA 7(a) loans, most lenders expect a minimum DSCR of 1.25x, as detailed in SOP 50 10 8 Section B, Chapter 1. This means your business needs to generate $1.25 in net operating income for every $1.00 of debt service. Some lenders, however, might accept a slightly lower ratio - down to 1.15x - depending on their underwriting policies and the strength of your overall loan application.

"A DSCR of 1.25x is widely recognized as the benchmark standard for SBA 7(a) loans, as outlined in SOP 50 10 8 Section B, Chapter 1: Credit Standards." - Pioneer Capital Advisory

The extra 25% above your debt obligations acts as a buffer, helping to absorb unexpected expenses or drops in revenue. If your DSCR climbs to 1.35x or higher, you may unlock benefits like lower interest rates, larger loan amounts, or more favorable repayment terms.

DSCR for SBA 504 Loans

SBA 504 loans, on the other hand, generally require a minimum DSCR of 1.20x. Unlike the 7(a) program, which adheres to more standardized guidelines, the DSCR requirements for 504 loans can vary by lender and Certified Development Company (CDC). This is because there’s no single universal standard for this program.

For 504 loans, the DSCR calculation focuses specifically on the project being financed. This includes the private first mortgage, the CDC/SBA second mortgage, and any existing business debt in the total debt service calculation. Since 504 loans are often used for real estate or heavy equipment purchases, lenders typically assess the cash flow generated by the financed asset rather than the overall business operations.

Additionally, the longer repayment terms available with 504 loans - up to 25 years for real estate - can make achieving a higher DSCR more manageable. This is often easier compared to the shorter 10-year terms common for 7(a) loans used for business acquisitions.

Key Components for Calculating DSCR

To figure out the Debt Service Coverage Ratio (DSCR) accurately, you need two main inputs: Net Operating Income (NOI) and Total Debt Service. Both are crucial for understanding your business's ability to manage its debt obligations.

Net Operating Income (NOI)

Net Operating Income represents the cash your business generates from its core operations after covering everyday expenses like rent, wages, and utilities - but before accounting for interest and taxes. Adam Hoeksema, Co-founder of ProjectionHub, puts it this way:

"Net operating income is the revenue left after all the day-to-day operating expenses like rent, wages, and utilities are taken out. But it doesn't include interest and tax expenses".

In many cases, NOI aligns closely with EBITDA. For business acquisitions, lenders might tweak Seller’s Discretionary Earnings (SDE) by deducting an estimated owner’s salary - often around $100,000.

Lenders also recast NOI by removing non-recurring items and non-cash expenses, such as depreciation, to focus on the cash flow your business reliably generates. However, it’s important to be cautious with these adjustments. As MidStreet advises:

"A small change in the cashflow will have a big effect on the DSCR and banks will scrutinize the addbacks heavily".

Now that we’ve covered NOI, let’s move on to Total Debt Service.

Total Debt Service

Total Debt Service includes all annual payments for principal and interest on both new and existing debts. This covers a wide range of obligations, such as:

- First and second mortgages

- Business lines of credit

- Credit card balances tied to the business

- Equipment or vehicle leases

- Invoice financing

- Short-term loans

When calculating this, don’t limit yourself to payments for a new loan - lenders evaluate your entire debt load. To improve your DSCR, consider paying off high-interest debts or trimming unnecessary expenses.

sbb-itb-97ecd51

How to Calculate DSCR Step-by-Step

The DSCR Formula

The formula for calculating DSCR (Debt Service Coverage Ratio) is:

DSCR = Net Operating Income (NOI) / Total Debt Service.

This ratio shows how many dollars of income your business generates for every dollar of debt payments. As AmpAdvance puts it:

"For every $1 you owe in loan payments, how many dollars of income do you have available?"

NOI is similar to EBITDA - it represents the cash your business generates before accounting for interest, taxes, depreciation, and amortization. Total Debt Service, on the other hand, includes all annual principal and interest payments for both current debts and the proposed SBA loan.

Here’s how to calculate DSCR step-by-step.

Calculation Process

-

Gather Financial Data

Start by collecting your most recent financial statements. Calculate your annual NOI by subtracting operating expenses - like rent, wages, and utilities - from your revenue, excluding interest and taxes. For business acquisitions, lenders may use Seller's Discretionary Earnings (SDE) instead of NOI, subtracting a reasonable owner's salary, often estimated at $100,000. -

Calculate Total Debt Service

Add up all annual debt payments. This includes payments for the proposed SBA loan as well as any existing obligations, such as credit card balances, business lines of credit, or equipment leases. For example, a $500,000 SBA 7(a) loan at 10% interest over 10 years has an annual payment of about $79,500. If you also have $30,000 in other annual debt payments, your total debt service would be $109,500. -

Perform the DSCR Calculation

Divide your NOI by the total debt service. For instance, if your NOI is $150,000 and your total debt service is $109,500, the DSCR would be approximately 1.37 ($150,000 ÷ $109,500).

This step is critical for determining whether you meet the benchmarks for SBA 7(a) and 504 loans.

How to Interpret DSCR Values

Understanding your DSCR is key to assessing your loan eligibility. For SBA 7(a) loans, the standard benchmark is a DSCR of 1.25x, while SBA 504 loans usually require a minimum of 1.20x. Matthew Elling from FastWay SBA explains:

"A DSCR of 1.2 means your business generates 20% more income than needed to cover your debt."

Here’s a breakdown of DSCR values and what they mean:

| DSCR Value | Interpretation | Approval Likelihood |

|---|---|---|

| < 1.0x | Insufficient coverage; income doesn’t fully cover debt obligations | High Risk |

| 1.15x | Minimum for some SBA 7(a) lenders; may need extra collateral | Borderline |

| 1.20x | Standard minimum for SBA 504 loans | Acceptable for 504 |

| 1.25x | Standard benchmark for SBA 7(a) loans; considered a "sweet spot" | Standard |

| 1.35x - 1.5x+ | Indicates strong financial capacity; may qualify for better terms | Excellent |

A DSCR below 1.0x means your business isn’t generating enough income to cover its debt. For example, a DSCR of 0.90 shows that only 90% of your debt payments are covered. To ensure reliability, lenders might reduce projected revenues by 10–15% to see if the DSCR remains above 1.15x.

DSCR Calculation Examples for SBA 7(a) Loans

Example 1: High DSCR Scenario

This example highlights a business acquisition that met SBA 7(a) requirements with ease. Jeff Baxter Jr. from MidStreet evaluated a deal where the business had Seller's Discretionary Earnings (SDE) of $700,000. After factoring in a reasonable owner's salary of $100,000, the available cash flow was $600,000. The annual debt service - combining the new SBA loan and existing obligations - was set at $400,000.

The math here is straightforward: $600,000 ÷ $400,000 = 1.5. A DSCR of 1.5x not only clears the SBA's 1.25x benchmark but also shows the business generates 50% more income than required to cover its debt. This extra margin allows for flexibility to handle unexpected costs, revenue dips, or even reinvestment in the business. Baxter pointed out that this strong financial position would likely lead to favorable loan terms from lenders.

Let’s now look at a contrasting case where the numbers don’t quite measure up.

Example 2: Low DSCR Scenario

This scenario dives into a business that struggled to meet SBA standards. The business reported an SDE of $400,000. After allocating $80,000 for the owner’s salary, the remaining cash flow was $320,000. Meanwhile, the annual debt service for the proposed loan and existing obligations added up to $280,000.

Here’s the calculation: $320,000 ÷ $280,000 = 1.14. With a DSCR of 1.14x, the business falls short of the SBA’s 1.25x requirement and even the 1.15x threshold that some lenders might accept. Baxter explained that a profit drop of just $40,000 would push the DSCR even lower, making the business ineligible for an SBA loan. To improve the chances of approval, the buyer would need to explore options like negotiating a lower purchase price, increasing the down payment to reduce debt, or finding ways to enhance the business’s cash flow before applying.

Conclusion

DSCR as a Key Metric for Financial Health

As discussed earlier, the Debt Service Coverage Ratio (DSCR) plays a central role in loan approvals and shaping financial strategies. It's especially critical in SBA loan underwriting. Pioneer Capital Advisory explains it best: "DSCR is at the heart of SBA loan underwriting. It tells lenders whether your business generates enough cash to repay the loan, and it tells buyers how much flexibility their deal structure allows". A DSCR below 1.0x indicates your business isn't generating enough cash to cover its debt obligations. On the other hand, a DSCR of 1.25x or higher boosts your chances of approval and allows for better financing terms.

But DSCR isn't just about securing loans. It also provides insight into how much financial buffer your business has to handle unexpected challenges. For example, a DSCR of 1.35x means you're producing 35% more cash than needed to cover your debt. This extra cushion can be used to reinvest in the business, manage revenue shortfalls, or even increase owner compensation.

"The higher the DSCR, the greater security a business has should it incur any major losses, and the more money the owner has to re-invest into the business" - Jeff Baxter Jr., MidStreet

Steps to Calculate DSCR Accurately

Accurate DSCR calculation hinges on precise inputs for both income and debt. Start with your Net Operating Income (NOI) or EBITDA, but make adjustments. Subtract a reasonable owner's salary (commonly $100,000) and exclude non-cash expenses like depreciation. If you're evaluating a business acquisition, use Seller's Discretionary Earnings (SDE) instead.

On the debt side, account for all obligations. This includes the proposed SBA loan, any existing business loans, equipment leases, lines of credit, and business credit card balances. Add up all annual principal and interest payments to calculate your total debt service. Then, use the formula: divide your adjusted cash flow by the total annual debt service. To ensure the accuracy of your calculation, review both historical and projected financial figures, as noted earlier.

FAQs

What affects the DSCR calculation for an SBA loan?

Several elements can affect your Debt Service Coverage Ratio (DSCR) when you're applying for an SBA loan. The most important factor is your business’s cash flow - specifically net operating income (NOI) or operating cash flow. This figure shows whether your income is sufficient to cover debt payments. Adjustments to cash flow, like adding back one-time expenses or owner compensation, can also shift the DSCR.

Other considerations include the precision of your financial records and the specific criteria used by the lender. For example, some lenders may account for capital expenditures or tax distributions when calculating DSCR. Additionally, lenders often examine your business’s historical financial performance to gauge the consistency of your cash flow. A solid track record can bolster your DSCR and make your loan application more appealing.

To improve your chances, focus on maintaining accurate financial statements and understanding how lenders might adjust your cash flow calculations. These steps can help ensure your DSCR aligns with SBA loan requirements.

How can I improve my DSCR to qualify for better terms on an SBA loan?

Improving your Debt Service Coverage Ratio (DSCR) can open the door to better SBA loan terms. To achieve this, focus on two key areas: increasing your business's net operating income (NOI) and reducing debt obligations.

Boosting your NOI can involve strategies like driving up sales, expanding your customer base, or adjusting your pricing to maximize revenue. Cutting unnecessary operating expenses and streamlining processes for greater efficiency can also make a noticeable difference. On the debt side, refinancing existing loans to secure lower interest rates or extending repayment terms can help reduce your monthly debt payments, directly improving your DSCR.

Make it a habit to monitor your DSCR regularly and keep detailed, accurate financial records. This practice not only helps you spot areas for improvement but also strengthens your case for loan approval. A higher DSCR can lead to better loan terms, such as reduced interest rates or the ability to borrow more.

Why is having a higher DSCR important when applying for an SBA loan?

A higher Debt Service Coverage Ratio (DSCR) indicates that your business produces sufficient cash flow to easily meet its debt obligations. This gives lenders confidence in your ability to repay, which can improve your chances of securing a loan.

Moreover, a solid DSCR can lead to better loan terms. You might qualify for lower interest rates or even larger loan amounts, offering your business greater flexibility and a stronger financial footing.