Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

Customer concentration risk happens when a large portion of a business's revenue comes from just a few customers. This creates a major vulnerability: losing one key client could severely harm cash flow, debt repayment, and overall stability. Businesses with high customer concentration often face:

- Lower valuations: Buyers apply reduced multiples due to perceived risks.

- Financing challenges: Lenders may deny loans or impose stricter terms.

- Deal complexities: Buyers may demand earn-outs, seller financing, or escrow holdbacks.

Key Risk Indicators:

- A single customer contributing over 40% of revenue is critical risk.

- The top 5 customers generating more than 50% of revenue signals high risk.

- Diversification is ideal when the top 5 customers account for less than 25% of revenue.

How to Assess:

- Analyze revenue data for the past 2–3 years, focusing on top customers.

- Review contracts for terms like "change-of-control" clauses.

- Stress-test financials to model the impact of losing major clients.

To mitigate risk, ensure diversified revenue streams, negotiate deal safeguards, and strengthen customer relationships through formal contracts. Tools like Kumo can help identify risks early and prioritize safer investments.

Why Customer Concentration Risk Matters in SMB Acquisitions

Revenue Volatility and Financial Stability

Relying heavily on one or two customers makes cash flow incredibly fragile. Losing a major client can send a business into financial turmoil, quickly draining working capital and driving down the Debt Service Coverage Ratio (DSCR). The DSCR, which evaluates a company's ability to manage its debt, can plummet when revenue streams shrink unexpectedly.

Lenders are acutely aware of this risk. Banks and SBA lenders often flag high customer concentration as a significant underwriting concern. For instance, if a single customer accounts for 30–40% of a company's revenue, losing that client could jeopardize the ability to service debt. Avery Hastings, CPA, puts it bluntly:

If one email from a client can nuke your deal, you don't own the business. They do.

This "trapdoor" effect underscores why customer concentration risk needs to be carefully evaluated during acquisitions.

Impact on Business Valuation

Customer concentration doesn't just create operational challenges - it also drags down business valuation. Buyers tend to apply lower EBITDA multiples to offset the uncertainty tied to revenue volatility. For example, a diversified company might secure a 4.5× EBITDA multiple, while a similar business with two customers making up 50% of sales might only achieve a 3.5× multiple.

The risk becomes even more critical when customer contributions cross certain thresholds. According to Euler Hermes, any single customer representing 20% or more of revenue signals high concentration. Forbes takes an even stricter stance, suggesting no one customer should account for more than 10% of total revenue.

M&A Transaction Complications

High customer concentration doesn't just impact valuation - it can also create major hurdles in mergers and acquisitions (M&A). Deals often require structural adjustments to mitigate risk, turning straightforward cash-at-closing agreements into more complex arrangements. Buyers might insist on contingencies like earn-outs, seller notes, or escrow holdbacks tied to customer retention over 12–24 months. While these measures protect buyers, they can delay full payment for sellers.

Lenders may also respond by tightening credit terms, making financing more difficult. On top of that, buyers face the challenge of relationship dependency. Key customers may have stronger loyalty to the seller than to the business itself. If contracts include "change-of-control" or "termination for convenience" clauses, major clients could walk away right after the acquisition. This creates a precarious situation where the business's future hinges on retaining a few critical customers.

Customer Concentration Risk Will Kill Your Fundraise or Exit | SaaS Metrics School | SaaS Risks

Collecting Data for Customer Concentration Analysis

To assess the risks tied to customer concentration, you'll need to gather detailed data on how much revenue each customer contributes.

Revenue Breakdown by Customer

Start by collecting sales data from the past 2–3 years, focusing on how much revenue each customer generates. Pay special attention to your top 1, 5, and 10 clients to calculate concentration ratios. This historical data provides valuable insights into patterns like customer churn, retention rates, and changes in the performance of major accounts over time.

Be cautious about inter-company transactions. For instance, during one acquisition, a seller claimed their largest customer contributed only 20% of total revenue. However, a quality of earnings review revealed that two linked entities, owned by the seller, were transacting internally. These internal dealings artificially inflated revenue figures. When these were excluded, the top external customer's share jumped to over 60%, prompting the buyer to cancel the deal. Always ensure revenue figures exclude such internal transactions to avoid misleading conclusions.

Customer Contracts and Payment Terms

Review contracts with top customers to understand their terms, including duration, renewal conditions, notice requirements, and termination clauses. Pay particular attention to "change-of-control" provisions, as these might allow a key client to terminate their agreement after an acquisition. It's also crucial to verify that significant accounts are backed by formal contracts rather than informal deals, as the latter offer little legal security and are often frowned upon by lenders.

Additionally, examine payment histories and credit data for major customers. This can help you identify risks like chronic payment delays or financial instability - especially concerning if a customer accounts for a large portion of your revenue.

Transaction History Analysis

Building on your contract reviews, dive into transaction histories to distinguish between stable, recurring revenue and one-off projects that might not continue after an acquisition. Compare the duration of customer relationships with their revenue contributions. Long-standing clients generally pose less risk than newer, high-revenue customers. This analysis also reveals whether growth stems from a healthy, diverse market or relies too heavily on a single expanding client. Overdependence on one client can amplify customer concentration risks.

These steps provide a solid foundation for calculating risk metrics in later stages of the analysis.

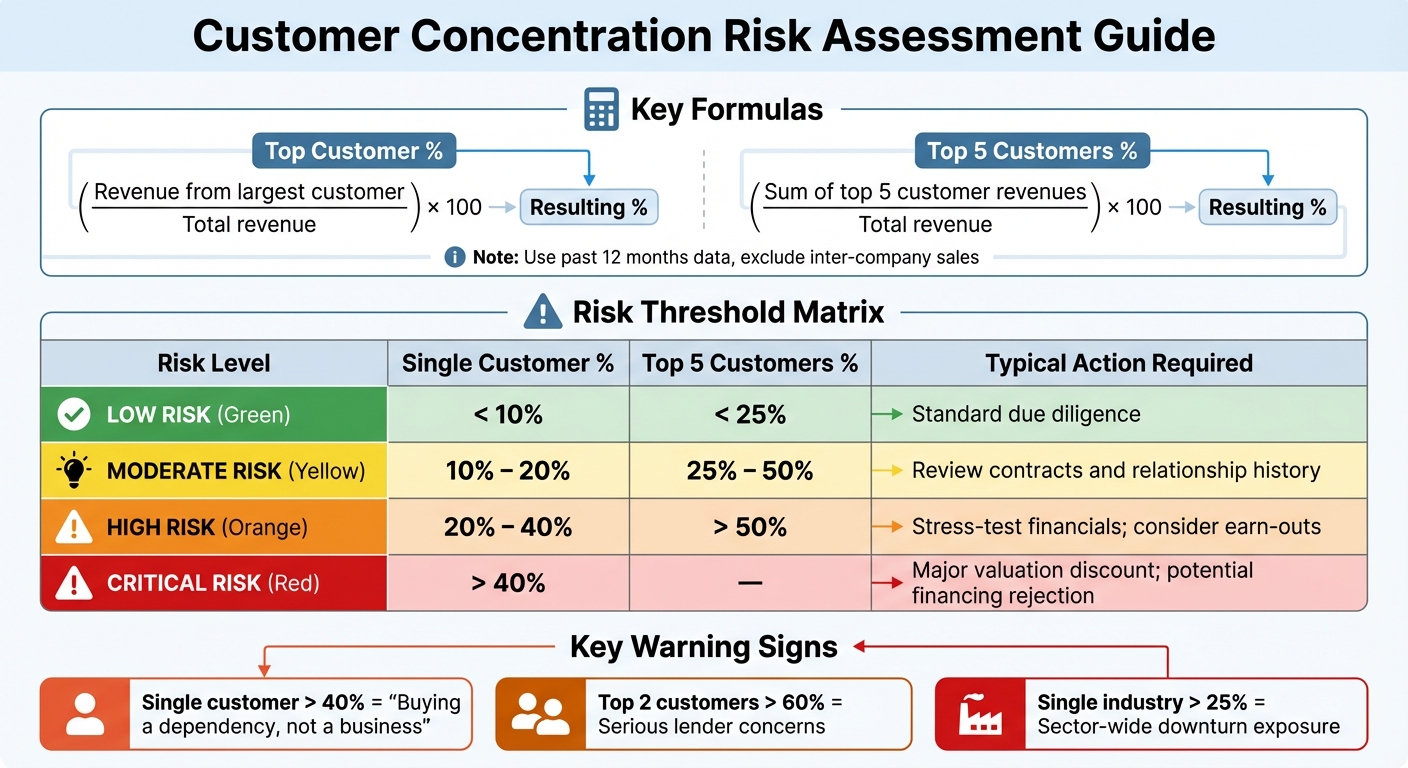

Key Metrics and Formulas for Risk Assessment

Customer Concentration Risk Assessment Thresholds and Actions

To gauge customer concentration risk, focus on revenue percentages. Two key formulas come into play here:

- Top Customer %: This is calculated as (Revenue from largest customer / Total revenue) × 100.

- Top 5 Customers %: This is determined by (Sum of the top 5 customer revenues / Total revenue) × 100.

When applying these formulas, use revenue data from the past 12 months or the most recent calendar year. Be sure to exclude inter-company and internal sales from your calculations. Begin by analyzing each major customer in descending order of their revenue contribution. Stop once individual contributions drop below 8% of the total revenue. Once these figures are ready, compare them against industry-defined risk thresholds to assess the level of concentration risk.

Risk Thresholds and Benchmarks

Industry benchmarks provide a clear framework for interpreting these metrics. For a single customer, the following thresholds apply:

- Less than 10%: Low risk

- 10% to 20%: Moderate risk

- 20% to 40%: High risk

- Over 40%: Critical risk

As Avery Hastings, CPA at Acquidex, explains:

"If 40%+ of revenue comes from one customer, you're not buying a business - you're buying a dependency".

For the top 5 customers combined, less than 25% signals low concentration risk, while 25% to 50% indicates moderate risk. Anything over 50% is a red flag for high risk. Additionally, if the top two customers alone account for more than 60% of revenue, lenders may respond with serious reservations. Beyond customer-specific risks, reliance on a single industry for more than 25% of revenue exposes the business to sector-wide downturns.

| Risk Level | Single Customer % | Top 5 Customers % | Typical Action Required |

|---|---|---|---|

| Low Risk | < 10% | < 25% | Standard due diligence |

| Moderate Risk | 10% – 20% | 25% – 50% | Review contracts and relationship history |

| High Risk | 20% – 40% | > 50% | Stress-test financials; consider earn-outs |

| Critical Risk | > 40% | – | Major valuation discount; potential financing rejection |

sbb-itb-97ecd51

Step-by-Step Customer Concentration Assessment

Once you've gathered the necessary data and identified risk benchmarks, it's time to evaluate customer concentration risk during due diligence. Here's how to approach it.

Calculate Key Metrics

Start by requesting a ranked list of customers. If the seller hesitates or refuses, consider it a warning sign. Using data from the most recent 12 months or the last full calendar year, calculate the following:

- Top Customer Percentage: (Revenue from a customer ÷ Total Revenue) × 100

- Combined Share of Top Five Customers: Add up the revenue from the top five customers.

Make sure to exclude inter-company sales from these calculations. A case study from 2024 involving a Midwest CPA firm, led by Chris Barrett, highlights why. In this instance, a seller claimed their largest customer made up only 20% of revenue. However, after removing inter-company sales that inflated total revenue, the true figure exceeded 60%. This revelation led the buyer to back out of the deal.

To gain deeper insights, create a table showing the revenue shares of the top five customers over the past 2–3 years. This will help identify whether these key accounts are growing, stable, or declining. Once you've established these metrics, shift your focus to the stability of customer relationships.

Review Contracts and Renewal Risks

Take a close look at the agreements underpinning each major customer relationship. Formal contracts should always take precedence over informal arrangements, as handshake deals provide no legal security - a major concern for lenders. Pay special attention to clauses like change-of-control provisions or termination terms that might allow customers to exit if the business is sold.

Additionally, determine whether these relationships are tied to the business itself or to the seller personally. Connections based on social or religious ties often dissolve when the seller steps away. As Todd Kutcher and John Milnes from Reliant Business Valuation explain:

Whenever a single customer makes up 15% or more of a company's business, it is important to examine the relationship and the subsequent risks related to this customer.

If any critical customer relationships are based on informal agreements, insist on converting them into formal contracts before moving forward with the deal.

With risks quantified and contracts reviewed, it's time to simulate potential challenges.

Stress-Test Revenue Impact

Run worst-case scenarios to gauge how the business would fare under pressure. For example, model a situation where the largest customer is lost and revenue drops by 70%. Check whether the Debt Service Coverage Ratio (DSCR) would still support financing under these circumstances. If the DSCR becomes unsustainable, the deal could be in jeopardy.

You should also calculate the remaining EBITDA if the largest customer leaves immediately after closing. This helps determine your effective entry multiple. For instance, if you're acquiring a business for $1,000,000 at a 5.0× multiple with $200,000 in EBITDA, but losing a key customer reduces EBITDA by 30% to $140,000, your effective multiple spikes to 7.1×. As Avery Hastings aptly notes:

A healthy business isn't just profitable - it's resilient. If one customer sneezing can trigger a cash flow coma, it's not resilient.

How to Reduce High Customer Concentration Risk

Addressing high customer concentration requires a combination of smart deal structuring, strategic diversification, and effective use of data tools. Here's how you can tackle this challenge.

Negotiating Earn-Outs and Price Adjustments

One way to handle customer concentration risk is by structuring deals that shift some of the risk back to the seller. For example, if a single customer contributes 40% of the company's revenue, you could set up part of the purchase as a seller note. This note could convert if that customer leaves within 12–24 months.

Another strategy is tying earn-outs to customer retention. Dustin Owen highlights the importance of aligning risk through earn-out terms:

I would be weighting consideration heavily to earn-out or VTB [Vendor Take Back] tied to customer retention.

Additionally, you might hold back 10–15% of the purchase price in escrow for 18 months. Releasing these funds could depend on key customers staying engaged. It's also wise to require the seller to confirm in writing that major customers haven't signaled plans to leave or requested price cuts.

Beyond these deal terms, expanding your revenue base can further reduce risk.

Diversification Plans and Customer Growth

A solid diversification plan after acquisition is critical. Instead of relying on one major client, aim to work with multiple smaller accounts to spread your risk. Automating the onboarding process can help you quickly bring in new customers.

You can also strengthen relationships with existing clients through regular account reviews. These reviews can uncover opportunities for upselling or cross-selling, which are often more cost-efficient than acquiring new customers. Expanding into new products, services, or industries is another way to balance revenue streams. For instance, if a top customer in manufacturing dominates your revenue, consider branching out into sectors like healthcare or retail to shield yourself from industry-specific downturns.

Another key step is to institutionalize relationships with major clients. Transitioning these relationships to a capable management team or key employees before closing the deal ensures continuity. As Jacob Orosz, President of Morgan & Westfield, explains:

The more indispensable you are to your business, the more difficult your business will be to sell - and the less your business is worth.

Using Kumo for Risk Assessment

Early identification of concentration risk is just as important as addressing it. Tools like Kumo can help by aggregating business listings and providing analytics to flag risks early. When using Kumo, pay close attention to indicators of revenue stability. For instance, if a seller highlights long-term contracts with key clients but lists only a handful of customers, that could be a warning sign.

Kumo’s AI-powered features, such as custom search filters and deal alerts, allow you to track changes over time. This helps you focus on opportunities with lower concentration risks, making it easier to prioritize safer investments.

Conclusion and Key Takeaways

Evaluating customer concentration risk is crucial for safeguarding your investment. The stakes are high: when a single customer accounts for more than 40% of revenue, businesses often face valuation cuts ranging from 20% to 40%. Additionally, lenders commonly flag these situations as too risky to fund.

Assessment Process Summary

Start by verifying bank deposits against 24 months of revenue. Review the key revenue percentages already identified - any single customer contributing over 10% of revenue is a warning sign, while concentrations above 50% signal extreme risk.

Next, simulate the impact of losing the top two customers. If the business struggles to meet debt obligations at 70% of projected revenue, the deal may be too unstable. Carefully examine contracts for details like duration, renewal terms, and assignability. To further mitigate risks, consider mechanisms like earn-outs, escrow holds (typically 5–15% of the purchase price), or seller notes tied to retaining key accounts.

This method ensures a more secure foundation for future acquisitions.

Next Steps for Future Acquisitions

Building on these insights, incorporate customer calls and verified revenue data into your due diligence process. Make customer concentration analysis a routine step. Confirm top-customer revenue percentages using bank statements, and for businesses where a single customer contributes 20–35% of revenue, conduct direct customer calls to evaluate the strength of those relationships.

Leverage tools like Kumo to identify concentration risks early. These tools track revenue stability across multiple listings, helping you prioritize opportunities with more balanced customer bases. By following these steps, you strengthen your risk management efforts and set the stage for smarter, safer acquisitions.

FAQs

What are effective ways to reduce customer concentration risk?

Reducing customer concentration risk means spreading out your revenue sources so you're not overly dependent on a single client. To get started, focus on broadening your customer base. This could mean targeting new market segments or bringing in smaller clients to ensure no single customer accounts for more than 20% of your total revenue. Another approach is to expand your offerings by introducing new products or services that appeal to different buyer groups. You might also consider exploring new distribution channels, like online sales or strategic partnerships, to tap into markets you haven’t reached yet.

At the same time, nurturing relationships with your existing customers is key. By offering value-added solutions and building loyalty, you can maintain steady sales while working toward diversification. Keep a close eye on key metrics, such as the percentage of revenue tied to your top customers, so you can spot potential risks early. Having a financial safety net, like solid cash reserves, can also provide a buffer if you lose a major client unexpectedly.

If you're exploring SMB acquisitions, tools like Kumo can help by analyzing customer concentration metrics across listings. This can reveal diversification opportunities before you close the deal. Combining these strategies can help you build a more balanced and stable revenue stream.

What happens financially if a business loses a key customer?

Losing a major customer can hit a business where it hurts the most - its bottom line. A sudden revenue drop can put a strain on cash flow, making it tougher to manage day-to-day expenses or fund future growth plans. This kind of financial pressure can quickly chip away at profitability and even affect the company's ability to stay liquid.

But the ripple effects don’t stop there. When a business depends heavily on a few key customers, losing one can make it seem less stable in the eyes of investors or potential buyers. This perception of higher risk often translates to a lower valuation, which can hurt opportunities for funding or acquisition.

To avoid these pitfalls, it’s crucial to broaden your customer base. By reducing reliance on a handful of clients, you can better safeguard your business’s financial health and long-term stability.

How does customer concentration affect the valuation of a business during an acquisition?

Customer concentration is a key factor in determining business valuation because it directly affects the perceived risk for potential buyers. When a single customer - or a small group of customers - accounts for a significant chunk of revenue, typically 30%–40% or more, it raises red flags about the business's stability. Buyers often worry, “What if one or two major customers stop working with the company?” If losing those customers would seriously disrupt cash flow or make it difficult to manage debt, buyers may lower their offer price or reduce the EBITDA multiple to reflect the added risk.

This concern is particularly relevant in industries with recurring revenue models, such as SaaS. In these cases, high customer concentration can push valuation multiples down. A common way to measure this risk is by calculating the ratio of revenue from the largest customer to total revenue. If this ratio exceeds industry norms - say, more than 10% for enterprise-focused companies - buyers may respond by negotiating price reductions, adding protective clauses, or structuring deals with contingent payments.

Tools like Kumo can be incredibly useful in this process. They provide analytics to identify customer concentration risks early, helping both buyers and sellers approach negotiations with a clearer understanding of the potential challenges.