Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

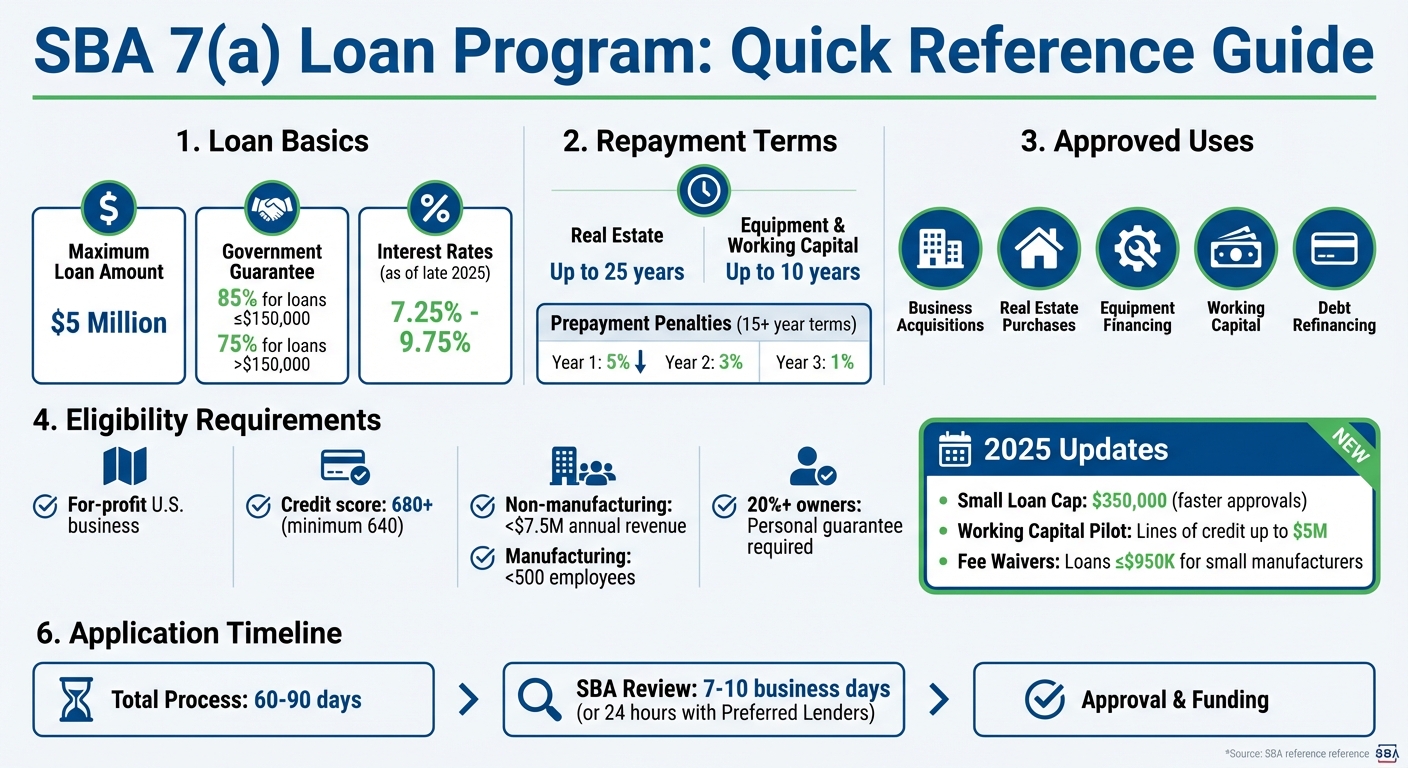

The SBA 7(a) Loan Program is a government-backed financing option designed to help small businesses in the U.S. secure funding. It supports a wide range of needs, including business acquisitions, real estate purchases, equipment financing, working capital, and debt refinancing. Loans can go up to $5 million, with the SBA guaranteeing 75%-85% of the loan amount, reducing lender risk and improving borrower access.

Key Highlights:

- Loan Limits: Up to $5 million.

- Government Guarantee: 85% for loans ≤ $150,000; 75% for larger loans.

- Uses: Business acquisitions, real estate, equipment, working capital, debt refinancing.

- Repayment Terms: Up to 25 years for real estate; up to 10 years for equipment and working capital.

- Interest Rates: Negotiated with lenders but capped by SBA guidelines (e.g., 7.25%-9.75% as of late 2025).

- Eligibility: For-profit U.S. businesses meeting size standards; good credit and financial history required.

Recent updates include:

- 2025 Changes: Lowered cap for "7(a) Small Loans" to $350,000 with faster approvals.

- New Pilot Program: Working Capital Pilot (WCP) offering lines of credit up to $5 million.

- Fee Waivers: Loans ≤ $950,000 for small manufacturers in specific sectors now have reduced fees.

This program is a flexible option for entrepreneurs who need financing but may struggle with traditional loans. The SBA also provides tools like Lender Match to connect borrowers with participating lenders.

SBA 7(a) Loan Program Key Features and Requirements

How SBA 7(a) Loans Can Be Used

Financing Business Acquisitions

SBA 7(a) loans can be a powerful tool for financing both full and partial business acquisitions. Whether you're looking to purchase an entire company or buy out a partner's equity, these loans offer the financial support you need. They also extend to franchise purchases, provided the franchise is listed in the SBA Franchise Directory. If the acquisition exceeds $500,000 and involves a full ownership transfer, lenders often require a 10% down payment, helping preserve your personal savings and liquidity. Additionally, any individual owning 20% or more of the business must typically provide a personal guarantee.

One of the loan's standout features is its flexibility. It can cover the acquisition price while also providing funds for working capital and any equipment purchases, all in one package. To apply, you'll need to submit a letter of intent, a company valuation, and financial statements from the past three years. This structure makes SBA 7(a) loans a versatile option for addressing a variety of operational and growth needs.

Other Approved Uses

SBA 7(a) loans aren't just for acquisitions - they're designed to meet a range of business needs. They can fund both short-term and long-term working capital requirements, such as day-to-day operating expenses, inventory purchases, or bridging seasonal cash-flow gaps.

These loans also allow for the purchase and installation of machinery, equipment (including those related to new technologies), furniture, fixtures, and supplies. If you're in need of real estate financing, SBA 7(a) loans can help with purchasing, constructing, or renovating owner-occupied commercial properties. The repayment terms are generous, offering up to 25 years for real estate and up to 10 years (or the useful life of the asset) for equipment.

Another benefit is the ability to refinance existing business debt, provided the new loan improves cash flow or satisfies specific SBA criteria. This refinancing option can complement acquisition strategies by optimizing financial resources. However, there are strict limitations on how funds can be used. For example, you can't use SBA 7(a) loans to pay off other SBA loans, cover delinquent federal or state taxes, or finance owner distributions unless there's a clear business purpose. Speculative or personal uses of the funds are also strictly off-limits.

Loan Amounts, Terms, and Interest Rates

Maximum Loan Amounts and Government Guarantees

SBA 7(a) loans have a maximum limit of $5 million. These loans come with partial government guarantees - 85% for loans of $150,000 or less and 75% for amounts above that threshold. For instance, a $5 million loan would include a government guarantee of $3.75 million, reducing the lender's risk and often leading to better loan terms for borrowers.

Repayment Periods and Interest Rate Structure

Repayment terms and interest rates depend on how the funds are used. Loans for real estate purchases can have repayment periods of up to 25 years, while loans for equipment, inventory, or working capital are usually capped at 10 years. The SBA follows what's known as the "Asset Life Rule", which means the loan term cannot exceed the expected lifespan of the asset being financed.

Interest rates are negotiated between borrowers and lenders but must stay within SBA-set limits. These rates are calculated as a base rate (often the Prime Rate) plus an allowable spread. As of December 30, 2025, interest rates ranged from 7.25% to 9.75%. For loans over $350,000, the spread can go up to 3.0%, while smaller loans - under $50,000 - can have spreads as high as 6.5%.

Loans with terms of 15 years or longer include prepayment penalties: 5% in the first year, 3% in the second, and 1% in the third. Additionally, as of October 1, 2023, loans of $1 million or less come with no upfront guarantee fees, while larger loans have fees ranging from 1.45% to 3.75%.

Eligibility Requirements for Borrowers

Business Requirements

To qualify for an SBA 7(a) loan, your business must meet specific criteria. First, it must be a for-profit entity actively operating within the United States or its territories. Non-profits and charitable organizations aren’t eligible.

The SBA also enforces size standards that vary by industry. For non-manufacturing businesses, the cap is $7.5 million in average annual revenue. Manufacturing and mining businesses, on the other hand, must have fewer than 500 employees. Alternatively, some businesses may qualify under a different size standard: a tangible net worth below $15 million and an average net income of less than $5 million (after federal income taxes, excluding carry-over losses) over the previous two fiscal years.

Certain types of businesses are automatically disqualified, including real estate investment firms, gambling establishments, lending institutions, speculative ventures, and passive landlords. If you’re purchasing a franchise, check the SBA Franchise Directory to ensure your franchise is pre-approved. Additionally, you’ll need to pass the "credit elsewhere" test, which requires proof that you cannot secure financing on reasonable terms without SBA assistance.

Beyond business qualifications, personal financial and character requirements also play a role in determining eligibility.

Personal Requirements

Lenders typically prefer a personal credit score of at least 680, though some may accept scores as low as 640. For 7(a) Small loans, the SBA requires a minimum FICO Small Business Scoring Service (SBSS) score of 165.

Your financial history is just as important. You must not have recent bankruptcies, foreclosures, or tax liens, and all federal obligations - such as taxes and student loans - must be current. The SBA also evaluates your "good character", which includes your ability to responsibly manage resources and business affairs.

If you own 20% or more of the business, you’ll need to provide an unlimited personal guarantee and undergo a full credit and background check. Additionally, all direct and indirect owners must be U.S. citizens, U.S. nationals, or lawful permanent residents (Green Card holders). Business owners on parole are not eligible.

sbb-itb-97ecd51

How to Apply for an SBA 7(a) Loan

Application Steps

You can't apply for an SBA 7(a) loan directly through the SBA. Instead, you'll need to go through a private lender, such as a bank or credit union. A helpful starting point is the SBA Lender Match tool, which connects you with lenders in your area that specialize in SBA loans.

Once you've chosen a lender, it's time to gather your paperwork. You'll need to fill out SBA Form 1919, along with Forms 912 and 413 (the latter is required if you own 20% or more of the business). Additional documentation includes:

- Three years of personal and business tax returns

- Current profit and loss statements

- Balance sheets

- A one-year cash flow projection

- Resumes for owners with at least 20% ownership

- Key operational documents like your business license, articles of incorporation, and lease agreements.

Your lender will review your application first. If they approve it, they'll forward it to the SBA for a loan guarantee. If you work with a Preferred Lender, the process can move faster since these lenders have the authority to approve loans without waiting for the SBA's separate review. In some cases, this can cut the approval time to as little as 24 hours, compared to the typical 7-10 business days.

Once both the lender and the SBA have approved your application, you'll move to the closing phase. This involves securing collateral and disbursing the funds. The entire process usually takes about 60 to 90 days from start to finish. During fiscal year 2025, the SBA backed more than $37 billion in 7(a) loans.

Keep in mind that there are some important updates to the 7(a) program that were introduced in 2025.

2025 Program Changes

In 2025, the SBA made several updates to the 7(a) loan program. One major change was lowering the cap for the 7(a) Small Loan category to $350,000. This category now benefits from a faster SBA review process, taking just two to 10 business days to approve smaller loans.

The fee structure has also been revised to support under-served business owners. Starting in fiscal year 2026 (beginning October 1, 2025), the SBA will waive guarantee fees for loans of $950,000 or less issued to small manufacturers in NAICS sectors 31 to 33. However, lenders can still charge a flat fee of up to $2,500 per loan. For other borrowers, guarantee fees generally range from 0.25% to 3.75%, depending on the loan size.

Another addition to the program is the 7(a) Working Capital Pilot (WCP), launched in late 2024. This pilot offers monitored lines of credit up to $5 million and features a simpler application process compared to traditional CAPLines. Additionally, borrowers now have more flexibility when purchasing a business. SBA loans can now be used to finance partial acquisitions instead of requiring a complete change of ownership.

Conclusion

Main Points to Remember

The SBA 7(a) Loan Program provides small businesses with flexible, government-backed financing options. Loans can go up to $5,000,000, with the government guaranteeing 75%-85% of the amount. These loans are incredibly versatile, allowing funds to be used for acquisitions, real estate purchases, equipment, working capital, or even debt refinancing.

Borrowers also benefit from favorable repayment terms - up to 25 years for real estate loans and up to 10 years for equipment financing - along with competitive interest rates and fee structures. Recent updates, like the Working Capital Pilot Program, which offers lines of credit up to $5,000,000, and support for partial acquisitions, have made the program even more accessible and practical for a variety of business needs. These features equip you with the tools to make confident acquisition decisions.

How Kumo Helps with Business Acquisitions

Securing the right loan is only part of the equation - finding the right business is equally important. This is where Kumo steps in. By using AI-powered tools, Kumo simplifies the process of identifying opportunities that align with SBA 7(a) loan criteria. Aggregated business listings, custom search filters, and real-time data ensure you can quickly spot the best opportunities.

Kumo also provides data analysis tools to evaluate a target business's cash flow, helping you ensure long-term financial stability. Whether you're pursuing a full acquisition or a partner buyout, Kumo’s global coverage of business listings enables you to act swiftly. This is especially advantageous when working with Preferred Lenders, who offer faster, in-house approvals.

Meet the NEW SBA 7(a) loan program (effective June 1, 2025)

FAQs

What do I need to qualify for an SBA 7(a) loan?

To qualify for an SBA 7(a) loan, your business needs to meet a set of specific requirements:

- For-profit operation: Your business must be actively generating revenue. Nonprofits are not eligible.

- U.S.-based operations: The business must operate within the United States or its territories.

- Small business classification: Your company must fall within the SBA’s size guidelines, which vary by industry and are determined by employee count or revenue.

- Eligible industry: Businesses in certain sectors, like gambling or lending, are not eligible for SBA loans.

- Lack of other financing options: You’ll need to prove that traditional financing isn’t accessible or would be too costly without SBA support.

- Strong credit and repayment ability: A good credit history and sufficient cash flow to cover loan payments are crucial.

If you're considering buying a business through platforms like Kumo, make sure the target business also meets these criteria to improve your chances of securing SBA 7(a) funding.

How are SBA 7(a) loans used for buying a business?

SBA 7(a) loans are a well-known choice for financing the purchase of a business. They can cover the entire purchase or just a portion, helping with expenses like real estate, equipment, inventory, and working capital.

These loans aim to make owning a business more attainable by providing appealing terms. Features such as lower down payments and extended repayment periods can significantly reduce the financial strain that often comes with buying a business.

What updates were made to the SBA 7(a) loan program in 2025?

In 2025, the SBA rolled out updates to the 7(a) loan program through a revised SOP 50-10-8, which officially took effect on June 1, 2025. These updates brought tighter eligibility rules, more rigorous underwriting standards, and greater responsibilities for lenders to encourage responsible lending practices.

Another key change was the reinstatement of lender fees for the program, beginning October 1, 2025. These modifications were designed to maintain the program's long-term stability and tackle issues tied to how it had been managed in the past.

Related Blog Posts

- SBA 7(a) Loan Basics for Business Buyers

- SBA Loan Terms: What Buyers Need to Know

- Top things to know about the June 1, 2025, the U.S. Small Business Administration (SBA) has implemented significant changes to its Standard Operating Procedure (SOP) 50 10 8, which governs the 7(a) and 504 loan programs

- SBA's SOP and the 7(a) loan program maxmimum loan amount. When will this be increased?