Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

Cash flow reconciliation ensures you're buying a business based on actual, usable cash - not inflated numbers. Many small-to-medium businesses (SMBs) rely on unaudited financials, making it easy for metrics like EBITDA to mislead buyers. Without reconciling cash flow, you risk overpaying, missing hidden liabilities, or facing cash shortages post-acquisition.

Here’s why this matters:

- Reported profits don’t always equal real cash. For example, a company with $600,000 EBITDA might only generate $350,000 in operating cash due to slow receivables or other issues.

- Unreconciled cash flow hides risks. These include inflated revenue, uncollectible receivables, or discrepancies between financial statements and bank deposits.

- Thorough reconciliation protects you. It helps verify financial accuracy, ensures fair valuations, and reduces post-close surprises.

To safeguard your investment, use methods like bank-to-book reconciliation, proof-of-cash analysis, and operating cash flow vs. EBITDA validation. These steps help uncover discrepancies, assess true cash flow, and negotiate better deal terms.

Risks of Unreconciled Cash Flows in SMB Acquisitions

How SMB Financial Gaps Create Problems

Many small businesses in the U.S. rely on financial records that are prepared with minimal oversight, often focusing solely on tax purposes. These records are typically created using spreadsheets or manual bookkeeping, which increases the likelihood of errors, timing mismatches, and irregularities.

Things get even murkier when business owners mix personal and business expenses or skip regular reconciliations. This lack of discipline makes it challenging for potential buyers to get a clear picture of actual cash activity. On top of that, weak internal controls - like having one person manage both cash receipts and accounting - can introduce discrepancies, further undermining the reliability of the reported numbers.

These operational shortcomings can lead to significant financial misstatements, creating major risks for buyers.

Financial Risks from Poor Reconciliation

When cash flow reconciliation is neglected, several financial risks emerge. For example:

- Revenue might be recorded without corresponding bank deposits.

- Uncollectible receivables may not be written off.

- Sales could be recognized prematurely.

A proof-of-cash analysis often uncovers periods where reported revenue growth isn't backed by actual bank deposits. These misclassifications can inflate EBITDA and distort the quality of earnings, leading buyers to overvalue the business based on unreliable financial metrics.

Beyond inflated revenue, unreconciled cash flows can hide deeper problems like working capital issues. Buyers may fail to spot slow-paying or uncollectible receivables, understated bad debt reserves, or aging inventory that ties up cash. After the acquisition, these hidden issues can create unexpected cash demands - whether it's funding receivables, covering overdue payables, or restocking inventory levels higher than the financials suggested. These surprises can squeeze liquidity and hurt returns.

Weak internal controls also open the door to fraud, such as skimming cash, creating fake vendors, making duplicate payments, or maintaining off-book accounts. Over time, these practices can obscure the business’s real cash-generating ability.

Ultimately, these discrepancies tend to surface during more detailed financial examinations.

When Cash Flow Issues Surface

Cash flow problems become clear during thorough financial reviews, such as quality of earnings (QoE) analyses or proof-of-cash exercises that check financial statements against bank activity. Warning signs include:

- Large gaps between EBITDA and operating cash flow.

- Unusual growth in receivables or payables compared to sales.

- Inconsistent gross margins.

- Bank statements that don’t match reported cash balances.

These red flags often prompt buyers to dig deeper, requesting additional bank records and reperforming reconciliations across multiple years and accounts.

Post-acquisition, unresolved issues can show up as negative cash variances against budget, sudden borrowing needs, or struggles to meet payroll and vendor obligations - even when EBITDA appears strong. Integration efforts, like migrating to the buyer’s ERP system or standardizing revenue recognition practices, often reveal prior misclassifications, unrecorded expenses, and timing mismatches. These discoveries can significantly lower the actual free cash flow.

All of this underscores the importance of rigorous cash flow reconciliation to ensure accurate valuations and maintain liquidity during and after the acquisition process.

AMA: What Every Buyer Should Know About Financial Due Diligence & QofE

Cash Flow Reconciliation Methods

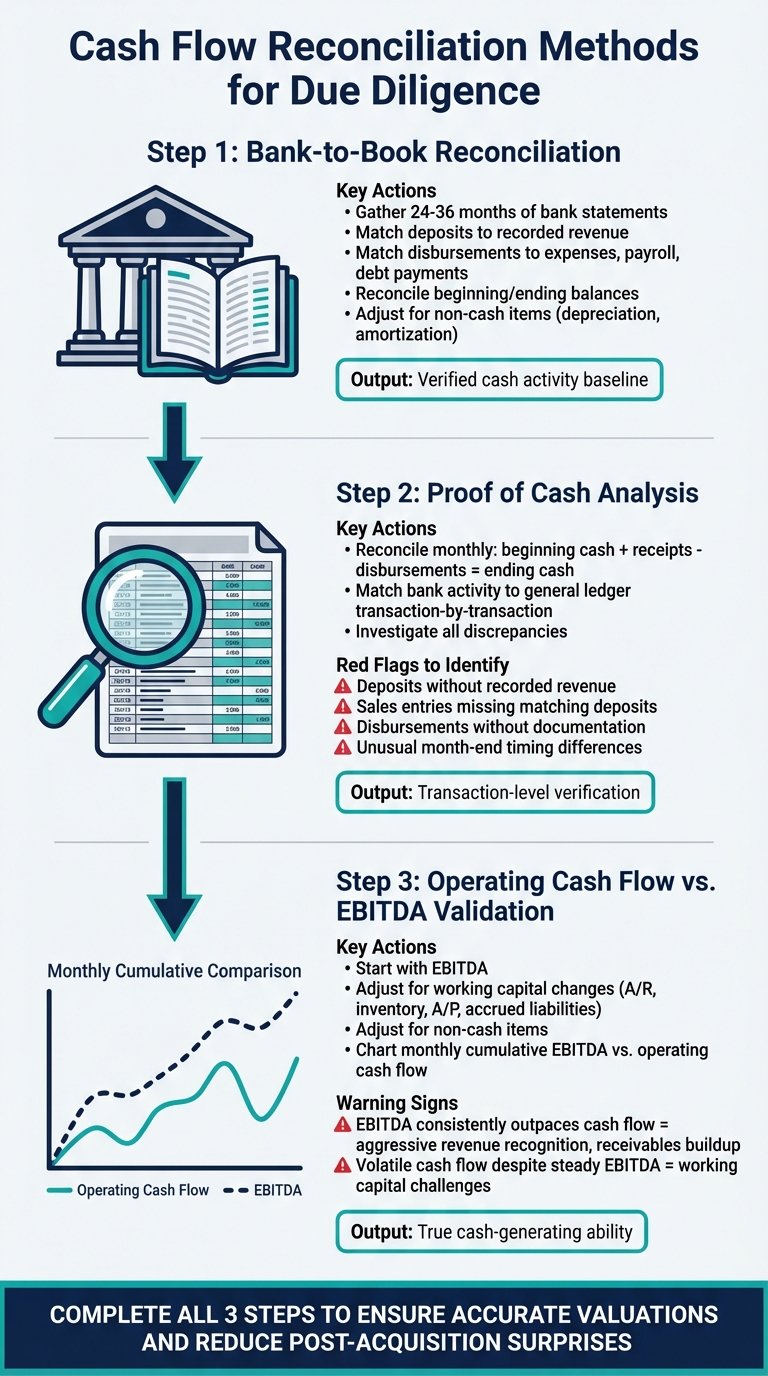

3-Step Cash Flow Reconciliation Process for Due Diligence

Once you grasp the risks of unreconciled cash flows, the next step is to put effective reconciliation methods into action. These methods help you tie financial records directly to bank activity, catching discrepancies early and ensuring a clear picture of your business's cash movements.

Bank-to-Book Reconciliation

Bank-to-book reconciliation involves matching your internal records with bank statements to verify cash activity. Start by gathering all bank statements for every operating and payroll account over the review period - typically spanning 24 to 36 months. Compare total deposits from the bank to recorded cash receipts and revenue. Then, match total disbursements to recorded expenses, payroll, debt payments, owner distributions, and capital expenditures.

Make sure to reconcile beginning and ending bank balances with your ledger, accounting for timing differences like deposits in transit or outstanding checks. Adjust for non-cash items, such as depreciation, amortization, and changes in accounts payable. For U.S. businesses in cash-heavy industries - like local services or hospitality - it's especially important to verify any unrecorded cash-only sales.

Once you've nailed down the basics, you can take it a step further with a proof of cash analysis, which digs into individual transactions.

Proof of Cash Analysis

Proof of cash analysis goes deeper by reconciling beginning cash, total receipts, disbursements, and ending cash - usually on a monthly basis. This approach directly matches bank activity to your ledger. Start by confirming the beginning and ending cash balances for each account. Then, total all deposits and disbursements from the bank statements and compare these figures to the records in the general ledger. Any differences should be investigated on a transaction-by-transaction basis.

This method acts as a mini-audit for unaudited small and medium-sized businesses (SMBs). It can uncover issues like fictitious revenue, lapping of receivables, unrecorded liabilities, or unauthorized payments. Common red flags include deposits without corresponding recorded revenue, sales entries missing matching deposits, disbursements without proper documentation, and timing differences at month-end. If significant unexplained discrepancies arise, you may need to expand your testing, confirm details with vendors or customers, or even revisit deal terms.

With cash activity reconciled, the next step is to see how reported profitability aligns with actual cash flow through an operating cash flow versus EBITDA analysis.

Operating Cash Flow vs. EBITDA Validation

EBITDA is often highlighted as a key profitability measure, but cash flow paints a more accurate picture of a business's financial health. This step ensures reported figures align with real cash movements, which is essential for accurate valuations. Start with EBITDA and adjust it to reflect operating cash flow. This involves accounting for changes in working capital - like accounts receivable, inventory, accounts payable, accrued liabilities, and prepaid expenses - as well as non-cash items.

Chart monthly cumulative EBITDA alongside operating cash flow to identify any gaps. If EBITDA consistently outpaces operating cash flow, it could signal aggressive revenue recognition, a buildup of receivables, improperly capitalized expenses, under-accrued liabilities, or overly extended customer payment terms. On the flip side, if cash flow is volatile or negative despite steady EBITDA, it might point to working capital challenges - such as seasonal spikes in receivables or inventory consuming more cash than expected. These differences can significantly impact a business's ability to handle debt, especially under current market interest rates. That makes this validation step critical for both valuation and financing decisions.

sbb-itb-97ecd51

Integrating Cash Flow Reconciliation into Due Diligence

Reconciliation within due diligence workflows

Cash flow reconciliation plays a critical role in verifying financial accuracy during due diligence. By comparing historical financial statements to actual bank transactions, this step ensures the numbers align with reality. Typically, reconciliation follows the quality of earnings (QoE) assessment, which identifies one-time items and evaluates the sustainability of earnings. A proof of cash analysis then confirms whether the QoE-adjusted EBITDA reflects genuine banking activity.

This process naturally ties into working capital analysis. For instance, when reviewing accounts receivable aging, inventory levels, and payment behaviors, reconciliation helps determine if the cash conversion cycles align with the reported figures. If a seller reports robust collections but bank deposits don't match the recorded revenue, it raises a major red flag. These findings can directly impact valuation, escrow terms, and purchase agreement warranties. This integrated approach also ensures your data requests to the seller are precise and targeted.

Required data from sellers

To perform effective reconciliation, you'll need a detailed data set from the seller right at the start. This includes 24 to 36 months of bank, payroll, and deposit account statements, along with detailed ledgers, trial balances, and support documents like accounts receivable, accounts payable, and inventory schedules. Full financial statements (income statement, balance sheet, and cash flow statement) spanning at least three years are also non-negotiable.

Additionally, debt schedules, loan agreements, and records of interest payments are essential for reconciling financing activities. If the seller has existing bank reconciliation workpapers, these can provide valuable insights into the rigor of their internal processes and save time in your review. A comprehensive initial data request ensures discrepancies are identified more efficiently.

Using deal sourcing platforms to streamline due diligence

Once internal data verification is underway, external deal-sourcing platforms can further refine the process. Tools like Kumo aggregate over 100,000 business listings and use AI-powered filters to help you focus on high-potential opportunities. By integrating structured data into your financial modeling tools, these platforms streamline the early stages of due diligence.

This approach prevents wasted effort on unqualified leads. Instead, you can dedicate your reconciliation efforts to the most promising targets. For example, Kumo allows you to export structured data as CSV files, which can then be integrated into CRMs and financial models. By the time you decide to pursue a specific target, you'll already have an organized foundation of structured data. This makes it easier to cross-check the seller's bank statements and ledgers, helping you identify inconsistencies more effectively.

Conclusion

The importance of thorough cash flow reconciliation in successful SMB transactions cannot be overstated. Here’s why it matters:

More accurate valuations and pricing

Cash flow reconciliation ensures you're paying for actual, sustainable cash flows rather than inflated earnings. By conducting a proof-of-cash analysis - comparing financial statements with bank records - you can uncover the true recurring free cash flow that supports valuations, especially critical for unaudited SMBs where internal controls might be lacking. This process may reveal hidden liabilities or overly aggressive revenue recognition practices, leading to purchase price adjustments as high as 10–20%. Without proper reconciliation, buyers could face valuation errors of up to 30% due to unsustainable earnings.

Better deal terms and reduced risk

Identifying cash flow discrepancies allows for better-structured deal terms, such as earnouts linked to verified post-close cash performance, escrows (typically 10–15% of the deal value) to cover hidden liabilities, and working capital adjustments based on normalized historical levels. This level of diligence can lead to fewer post-close disputes - up to 25% fewer disagreements over working capital adjustments. These structured terms not only strengthen initial negotiations but also help maintain financial stability after the deal closes.

Post-close financial stability

Accurate reconciliations give banks confidence in the business's cash flow history and internal controls, making credit facility transfers smoother and ensuring compliance with financial covenants. Verified cash flow data minimizes early liquidity risks, such as delayed receivables, and supports better financing terms post-acquisition. This data also aids in creating reliable cash flow forecasts, reducing the likelihood of mismatches in capital expenditures or liquidity issues. Strong reconciliations enable precise working capital planning and help establish solid banking relationships from the start.

FAQs

Why is cash flow reconciliation important for valuing a business during an acquisition?

Cash flow reconciliation plays a key role in accurately assessing a business's value. It provides a clear view of the company's actual cash inflows and outflows, ensuring a better understanding of its financial health. This process can reveal the true profitability of the business while also identifying potential risks, such as discrepancies or irregularities in financial records.

By offering a dependable financial snapshot, cash flow reconciliation minimizes the risk of overestimating or underestimating the business's worth. This clarity makes it easier to negotiate a fair purchase price and supports smarter, more informed acquisition decisions.

How can you effectively perform cash flow reconciliation during due diligence?

To ensure accurate cash flow reconciliation during due diligence, start by comparing cash inflows and outflows with the accounting records. Cross-check bank statements against ledger entries, and carefully examine any timing differences that might arise. These steps are key to verifying the reliability of financial data.

Leveraging automated tools can make the process faster and more precise by pinpointing discrepancies with ease. Consistent reconciliation is essential for identifying potential risks and ensuring accurate business valuations.

Why is operating cash flow different from EBITDA, and why is it important?

Operating cash flow and EBITDA often tell different stories because they measure distinct aspects of a company's financial health. Operating cash flow accounts for actual cash movements, including shifts in working capital, capital expenditures, and other cash-related activities that EBITDA doesn't factor in. On the flip side, EBITDA zeroes in on earnings before interest, taxes, depreciation, and amortization, which can gloss over important cash flow nuances.

Why does this difference matter? Operating cash flow gives a more accurate view of a company's liquidity and its ability to produce cash. When conducting due diligence, understanding these differences is crucial for evaluating risks, ensuring accurate valuations, and making well-informed decisions.