Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

SBA loans are a popular option for buying small businesses due to their low down payment (10%) and favorable terms. However, when using an SBA loan, the purchase agreement must meet specific requirements to avoid delays or denials. Here's what you need to know:

- Equity Injection: Buyers must provide 10% of the purchase price - 5% in cash and 5% through a seller note on "full standby" (no payments allowed during the SBA loan term).

- Seller Financing Rules: Seller notes must comply with SBA guidelines, including standby terms and personal guarantees under certain conditions.

- Business Valuation: The purchase price must align with an independent valuation ordered by the lender.

- Prohibited Terms: Earn-outs and partial ownership transfers are not allowed.

- Documentation: Buyers and sellers must provide detailed financial records, tax returns, and other forms to ensure compliance.

Non-compliance can lead to loan denials or delays, so structuring the purchase agreement correctly is critical. Working with SBA-preferred lenders and advisors can streamline the process and help avoid common pitfalls.

What SBA Lenders want to see in your Purchase & Sale Agreement

SBA Loan Requirements That Affect Purchase Agreements

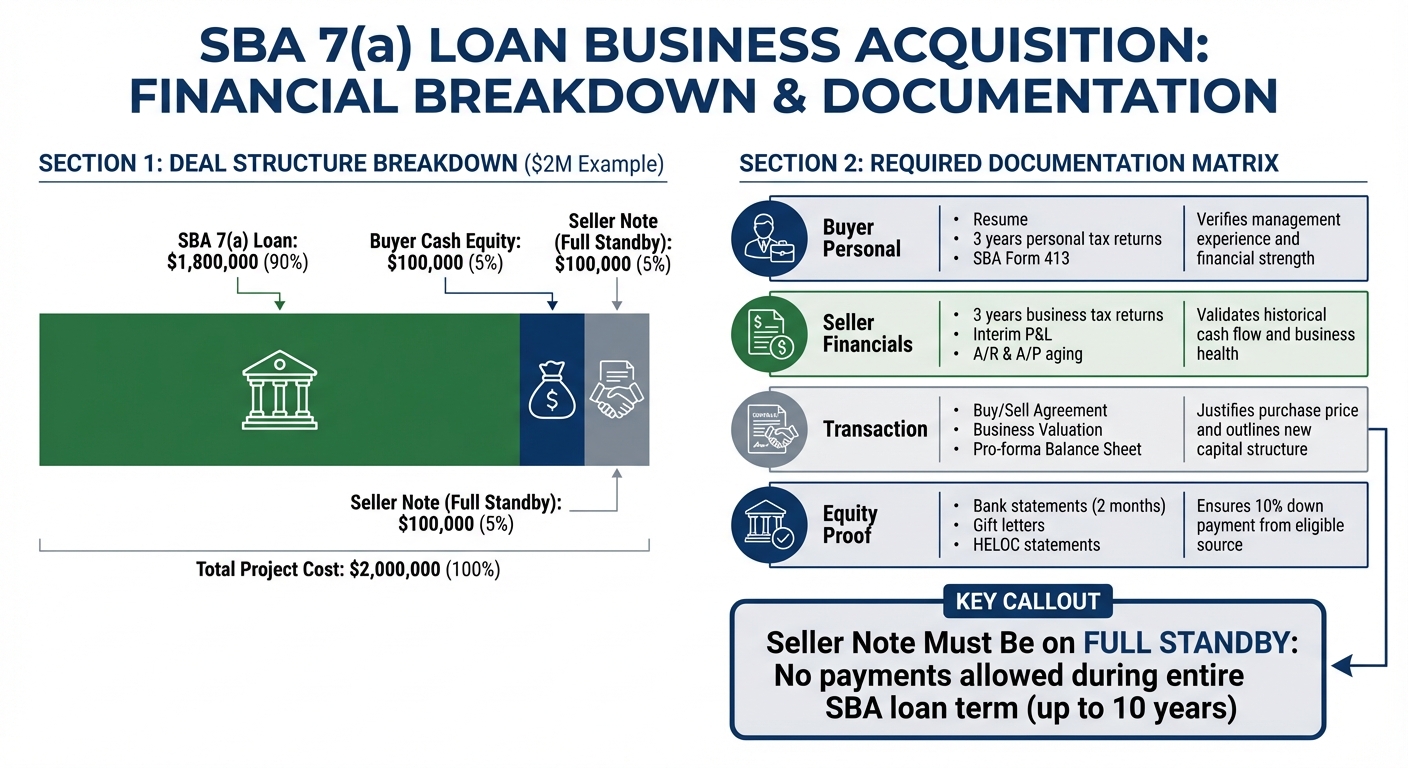

SBA Loan Structure: $2M Business Acquisition Breakdown

Minimum Equity Injection Rules

Under SBA guidelines, buyers are required to provide a 10% equity injection for business acquisitions, which directly influences the structure of purchase agreements. This equity can be broken down into two parts: 5% in cash from the buyer and another 5% through a seller note placed on full standby.

The purchase agreement must clearly outline the sources of equity. For the buyer's 5% cash portion, eligible sources include personal savings, a 401(k) rollover (ROBS), or gifted funds (accompanied by a formal gift letter). Additionally, the seller note must be explicitly noted as being on full standby, meaning no payments can be made during the SBA loan term, which typically spans 10 years.

According to the SBA Standard Operating Procedure: "At a minimum, SBA considers an equity injection of at least 10 percent of the total project costs... to be necessary for such transactions".

Here’s an example of how a $2 million acquisition would be structured under these rules:

| Source | Amount | Percentage |

|---|---|---|

| Buyer Cash Equity | $100,000 | 5% |

| Seller Note (Full Standby) | $100,000 | 5% |

| SBA 7(a) Loan | $1,800,000 | 90% |

| Total Project Cost | $2,000,000 | 100% |

As Ishan Jetley, Owner of GoSBA Loans, stated: "0% down is no longer possible, but the new rules allow for 5% down acquisitions when structured correctly with a seller note on full standby".

This breakdown highlights the importance of clearly defining equity sources, which also plays a key role in structuring seller notes, as discussed below.

Seller Financing and Standby Agreement Rules

When a seller note is used to meet the equity injection requirement, the purchase agreement must include specific standby language. This means the seller note must remain on full standby for the entire SBA loan term, which could stretch up to 10 years. During this period, the seller cannot receive any payments until the SBA loan is fully repaid.

If the seller note is structured as regular financing (not counting toward equity), the business must maintain a Debt Service Coverage Ratio (DSCR) of at least 1.25x when factoring in these payments. The purchase agreement should clearly define the timing and terms of seller payments to ensure compliance with SBA requirements and prevent issues with loan approval.

The policy changes introduced in 2025 added further complexity. Sellers providing financing must now personally guarantee the SBA loan under certain conditions. If the seller note accounts for more than 20% of the deal, the guarantee lasts for the entire loan term. If it’s under 20%, the guarantee is required for two years. These terms must be explicitly addressed in the purchase agreement. Notably, over 50% of business sellers surveyed in 2025 were unaware of these updates.

Another key aspect involves the seller's role post-closing. Sellers are allowed to act as consultants for up to 12 months, but only in a non-managerial capacity with no decision-making authority. The purchase agreement should detail the consulting period, compensation, and scope of duties to ensure compliance with SBA rules.

With these financing rules in place, ensuring the purchase price is accurate and justified becomes a critical next step.

Business Valuation and Price Justification

The SBA mandates that a business valuation be conducted by a "qualified source" to justify the purchase price. This valuation is ordered by the lender, and the purchase agreement must align with its findings. If the agreed-upon price exceeds the valuation, lenders may require a price adjustment or a higher equity injection from the buyer to make up the difference.

This policy is designed to prevent overpayment by ensuring the purchase price reflects the business’s actual value. The purchase agreement should include provisions for price adjustments if the valuation comes in lower than expected. Factors such as the business’s financial performance, industry benchmarks, and current market conditions are all considered during the valuation process, making it essential for the purchase price to be well-supported by these metrics.

Such measures ensure that both the buyer and lender are protected from overpaying for a business, while still meeting the SBA's equity injection requirements.

Required Documentation for SBA Loan Approval

Financial Statements and Tax Returns

When applying for an SBA loan, having the right financial documents in order is crucial. The SBA requires three years of business federal tax returns from the seller, as well as interim financial statements (Profit & Loss and Balance Sheet) that are no older than 90 days. These documents play a key role in determining the business's valuation and underwriting. Lenders carefully compare the seller's financials with IRS records to confirm their accuracy and reliability.

As Katie O'Brien from Starfield & Smith Attorneys at Law notes: "If a loan is underwritten based on certain financial information, it is important for Lender to verify if that financial information is reliable and accurate. Moreover, if an applicant has not filed its required federal tax returns, it is not eligible for SBA financing".

To facilitate this verification, purchase agreements should include a cooperation clause requiring the seller to sign IRS Form 4506-C or Form 8821, allowing lenders to obtain tax transcripts. If the IRS cannot locate the returns or if discrepancies arise between transcripts and submitted financials, the loan process may be delayed or even canceled. Sellers are also expected to provide aging reports for accounts receivable and accounts payable, giving lenders a detailed view of the business's current financial standing.

These financial records form the foundation for structuring the purchase agreement and ensuring compliance with SBA requirements.

Required Purchase Agreement Clauses

The purchase agreement itself must include specific clauses to align with SBA loan standards. It must clearly state that the deal involves the purchase of the entire business, confirming a full transfer of ownership. Additionally, earn-out arrangements - where part of the purchase price depends on future business performance - are not allowed under SBA guidelines.

If the seller plans to stay involved after the sale, their consulting role is limited to a maximum of 12 months. The agreement should also provide a detailed list of all assets being purchased, including intangible assets, to justify the loan amount and confirm that the purchase price aligns with the business's historical performance. Furthermore, any individual owning 20% or more of the business must provide an unlimited personal guarantee, which should also be acknowledged in the agreement.

These clauses ensure that the purchase agreement meets SBA standards while protecting both the buyer and lender.

Buyer and Seller Documentation Responsibilities

Both buyers and sellers have specific documentation responsibilities that are essential for SBA loan approval. Buyers need to submit a resume, three years of personal federal tax returns (including W2s), SBA Form 413 (Personal Financial Statement), a credit report authorization, and a detailed business transition plan. These documents help demonstrate the buyer's ability to manage the business effectively, a key factor in the approval process.

| Category | Specific Requirements | Purpose |

|---|---|---|

| Buyer Personal | Resume, 3 years personal tax returns, SBA Form 413 | Verifies management experience and financial strength |

| Seller Financials | 3 years business tax returns, Interim P&L, A/R & A/P aging | Validates historical cash flow and business health |

| Transaction | Buy/Sell Agreement, Business Valuation, Pro-forma Balance Sheet | Justifies the purchase price and outlines the new capital structure |

| Equity Proof | Bank statements (2 months), Gift letters, HELOC statements | Ensures the 10% down payment is from an eligible source |

Buyers must also provide documentation for any large recent deposits to confirm the legitimacy of their equity injection. Transaction-specific documents include a signed Letter of Intent (LOI) or purchase agreement, a pro-forma balance sheet effective on the transfer date, and an independent business valuation. Working with lenders in the SBA Preferred Lender Program (PLP) can streamline the process by avoiding direct SBA review, speeding up the approval timeline.

sbb-itb-97ecd51

Common Problems and How to Structure SBA-Compliant Purchase Agreements

Frequent Mistakes in SBA Transactions

When structuring SBA purchase agreements, there are a few common pitfalls that can derail the process. One major issue is earn-out arrangements - these are prohibited under SBA 7(a) rules, which require the purchase price to be fixed. Another frequent mistake involves improperly structured seller notes. If a seller note is used to cover part of the 10% equity injection, it must be placed on "full standby." This means no payments - whether principal or interest - can be made until the SBA loan is fully repaid. Failing to meet this condition often causes delays in loan approvals.

Seller involvement in management is another area to watch. SBA rules limit seller participation to 12 months following the sale. Additionally, lease terms must align with the SBA loan's amortization period. In cases of partial buy-outs, sellers often overlook the requirement to personally guarantee the SBA loan for at least two years, even when their ownership stake drops below 20%.

Addressing these common issues early in the process can help both buyers and sellers create a purchase agreement that meets SBA guidelines.

Practical Tips for Buyers and Sellers

To stay on track with SBA requirements, the first step is to ensure the Letter of Intent (LOI) aligns with SBA rules. The LOI should clearly state that the transaction involves 100% ownership transfer and include acknowledgment of personal guarantee obligations for any owner with a 20% or greater stake. It's also smart to address standby terms upfront during negotiations, as waiting until loan underwriting can lead to unnecessary complications.

Working with lenders in the SBA Preferred Lender Program (PLP) can help speed up the process. These lenders can underwrite and close loans without waiting for direct SBA approval, which can save valuable time. Buyers should also include working capital in their deal structure, either through a line of credit or reserves, to ease financial pressures during the transition period. Lastly, confirm that all buyer group members meet eligibility requirements, such as being U.S. citizens or lawful permanent residents, as this is non-negotiable.

Using Tools to Simplify the Transaction Process

Modern tools can make navigating SBA transactions much more manageable. For example, platforms like Kumo (https://withkumo.com) simplify the search for SBA-compliant acquisition opportunities. By aggregating business listings from marketplaces, brokerages, and proprietary sources, Kumo helps buyers identify suitable targets quickly. Its AI-driven search and real-time alerts keep buyers updated on potential deals, while built-in analytics evaluate whether a business's financials meet SBA valuation standards before time is spent on due diligence.

Once a target business is identified, keep everything - financial statements, tax returns, and purchase agreement drafts - organized in one central location. This reduces back-and-forth communication, which can otherwise stretch the approval process from weeks to months. Staying organized and leveraging the right tools can make a big difference in closing SBA-compliant deals efficiently.

Conclusion

Grasping SBA loan requirements is a key part of ensuring a successful approval process. At the heart of it all lies the purchase agreement, which allocates risk and ensures terms that align with SBA guidelines between the buyer and seller. When these terms stray from SBA Standard Operating Procedures, the deal risks stalling - or even falling apart - despite months of negotiation.

These guidelines exist to protect everyone involved: the buyer, the seller, the lender, and the government agency backing the loan. They create a framework that supports a smooth transaction and safeguards the interests of all parties.

Preparation plays a huge role in avoiding complications. As the Faison Law Group explains:

"The three essential functions of an SBA acquisition lawyer are borrower advocate, compliance specialist, and transaction facilitator".

Collaborating with professionals familiar with SBA Standard Operating Procedures can help tackle critical topics early in the process, such as standby seller notes, personal guarantees, and the 12-month consulting limit for sellers.

Buyers who engage experienced advisors early, work with Preferred Lender Program (PLP) lenders, and address SBA-related terms directly in the Letter of Intent stand a better chance of navigating the process successfully. For sellers, understanding standby requirements and ownership transfer rules ensures they can negotiate terms that safeguard their interests. When the purchase agreement is structured properly from the outset, both parties benefit - fewer delays, reduced legal expenses, and an increased likelihood of closing. Aligning every detail of the purchase agreement with SBA requirements not only ensures compliance with federal rules but also helps manage risks for everyone involved.

FAQs

What should I do if the business valuation is less than the purchase price?

If the business valuation is lower than the agreed-upon purchase price, the SBA loan amount could be adjusted down. In such cases, the buyer might have to fill the gap by contributing more personal funds or working out a seller financing arrangement.

To avoid surprises during the loan process, it’s crucial to ensure that the purchase price is closely aligned with the business valuation.

Why does a seller note need to be on full standby during the SBA loan term?

When an SBA loan is involved, a seller note must remain on full standby throughout the loan term. This means no principal or interest payments can be made on the seller note until the SBA loan is fully repaid. Why? It ensures the seller note stays in a subordinate position to the SBA loan, which helps safeguard the lender by minimizing financial risks.

This arrangement also benefits the borrower. By prioritizing repayment of the SBA loan, the borrower can show their ability to meet repayment obligations, all while keeping the deal aligned with SBA financing rules.

What documents are required for SBA loan approval when buying a business?

To get an SBA loan for buying a business, you'll need to gather some essential documents. These typically include proof of equity injection (usually 10% of the purchase price), any seller financing agreements, and a comprehensive purchase and transition plan. On top of that, you'll need to provide business financial statements, federal tax returns, bank statements, and personal financial statements.

Depending on the specifics of the deal, the SBA might ask for additional paperwork, like ownership records or extra financial details. Being well-prepared with all required documents can help make the approval process much smoother.