Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

Closing an SBA loan can be complex, but a checklist simplifies the process by ensuring all required documents are accounted for. Whether you’re dealing with an SBA 7(a) or 504 loan, the checklist helps avoid delays, protects the SBA guaranty, and ensures compliance with federal regulations.

Key Takeaways:

- SBA 7(a) loans focus on general business needs, requiring forms like SBA Form 1050 (Settlement Sheet) and SBA Form 147 (Note), alongside financial, equity, and legal documents.

- SBA 504 loans target fixed assets like real estate, using SBA Form 2286 (Debenture Checklist) and other forms to qualify for debenture sales.

- Both loan types require tax transcripts, proof of equity injection, and collateral documentation like UCC filings, appraisals, and title verification.

- Missing documents can delay funding or jeopardize the SBA guaranty.

Key Documents:

- Financial: Tax returns (3 years), balance sheets, profit/loss statements.

- Legal: Articles of Incorporation, operating agreements, leases.

- SBA Forms: 1050, 147, 148, 2286 (504 loans), and others.

- Third-Party Reports: Appraisals, lien searches, environmental reports.

Proper preparation, submission, and post-closing compliance are essential to ensure a smooth funding process for SBA loans.

How Long Will it Take to Close an SBA Acquisition Loan?

Pre-Closing Document Preparation

Before closing on an SBA loan, both borrowers and lenders need to gather specific documents that confirm financial status, equity contributions, and legal structure. Proper preparation ensures there are no delays that could jeopardize the SBA guaranty. Below is a breakdown of the necessary financial, equity, and legal documentation.

Required Financial Documents

Lenders are required to secure IRS Tax Transcripts or verifications in line with SBA guidelines. Borrowers must provide three years of business and personal tax returns if they own at least 20% of the business. Additionally, up-to-date financials, including balance sheets and profit and loss statements dated within 60 days of the loan application, are mandatory. A complete debt schedule listing all current business and personal liabilities is also required.

For SBA 7(a) loans, SBA Form 1050 (Settlement Sheet) or similar documentation is essential. This form verifies how the loan proceeds are being used and serves as a critical financial compliance tool.

Proof of Equity Injection

Borrowers must demonstrate they’ve contributed the required equity before receiving the first loan disbursement. This proof typically includes bank statements or wire transfer confirmations showing the cash injection. For startups, documentation of new capital contributions is necessary, while established businesses must provide evidence of prior investments. Again, SBA Form 1050 or an equivalent document is used to confirm the borrower’s financial contribution.

Since the exact requirements may vary depending on the loan size and the lender’s processes, borrowers should work closely with their lender to ensure all necessary documents are prepared and submitted.

Business Entity and Legal Documents

Borrowers must submit official formation documents like Articles of Incorporation or Organization, along with operating agreements, bylaws, or partnership agreements. Owners with at least a 20% stake are required to complete SBA Form 1919 (Borrower Information) and SBA Form 413 (Personal Financial Statement). Photo identification for these owners is also necessary.

If the business operates as a franchise, the franchise agreement must be included. For acquisitions, purchase agreements for the business or any real estate are required. Additionally, lenders need copies of current commercial leases or Letters of Intent for new locations. These leases must align with or exceed the loan term, including any renewal options. Other essential documents include business licenses, permits, and any regulatory compliance paperwork needed for operation.

Required SBA Closing Forms and Certifications

Securing an SBA loan involves completing specific forms and certifications to ensure compliance with federal regulations and confirm the appropriate use of loan funds. These documents must be filled out accurately and retained as outlined by SBA guidelines.

Primary SBA Forms

SBA Form 1050 (Settlement Sheet) is required for all 7(a) loans and their disbursements. This form ensures the proper use of loan proceeds and verifies equity injection. Be sure to use the latest version, updated on December 20, 2023.

SBA Form 147 (Note) acts as the official loan agreement for 7(a) loans, though lenders may use their own note forms instead. SBA Form 148 (Unconditional Guarantee) binds guarantors to repay the loan, though lenders can opt for their own guarantee agreements. Additional forms include:

- SBA Form 159 (Fee Disclosure and Compensation Agreement): Tracks fees paid to third-party representatives.

- SBA Form 155 (Standby Creditor's Agreement): Documents when creditors agree to subordinate their debt.

- SBA Form 601 (Agreement of Compliance): Confirms adherence to federal regulations.

- SBA Form 722 (Equal Employment Opportunity Statement): Provided to borrowers at closing.

Lenders are required to keep Forms 147, 148, and 1050 in their permanent records unless the SBA specifically requests them. All official forms are available for download at sba.gov.

Borrower Certifications

Borrowers must certify that all provided information is accurate and that they comply with the terms of the SBA loan. These certifications must be completed using the appropriate SBA forms.

While lenders can use alternative documentation that captures the same certifications for use-of-proceeds and equity injection, most prefer to stick with official SBA forms to avoid compliance risks. After certifications, lenders must also verify financial details through IRS documentation.

IRS and Tax Documentation

Accurate tax documentation is a key step in verifying financial information. IRS tax transcripts are essential for confirming financial accuracy and ensuring tax compliance. Lenders must match these transcripts against the borrower’s financial statements, with requirements depending on the loan type and amount. For 7(a) loans of $500,000 or less, lenders must verify business size eligibility through transcripts or business tax returns.

To obtain these transcripts, borrowers must sign IRS Form 4506-C (or Form 8821), authorizing the IRS to release their tax records. Typically, three years of business tax returns are required under the NAICS size standard, while two years are sufficient under the alternative size standard. Additionally, personal tax returns for the past three years are required for any individual owning 20% or more of the business.

"SBA requires that SBA lenders verify financial information in order to (i) confirm that the applicant filed business tax returns and (ii) verify that the applicant's financial statements that were provided to Lender match the tax returns that were filed with the IRS." - Katie O'Brien, Attorney, Starfield & Smith

If the IRS does not respond within 10 business days, lenders should re-submit the request, marking it as a "Second Request". Failure to properly verify tax information can result in the denial of the SBA loan guaranty, particularly in cases of early defaults. Borrowers are encouraged to review their tax transcripts alongside their profit and loss statements before closing to identify and address any discrepancies.

Third-Party Reports and Collateral Documentation

Collateral documentation plays a crucial role in verifying the security of a loan. Third-party reports help confirm the value and legal status of the collateral, and lenders are required to submit these documents to the SBA in compliance with current SOP guidelines. Below, we’ll break down key aspects like lien searches, title verifications, and other essential collateral documentation.

Lien Searches and UCC Filings

UCC searches ensure there are no conflicting liens on business assets. To secure their priority on personal property, lenders file UCC-1 financing statements.

For real estate, title searches are conducted to confirm ownership and identify any liens, easements, or encumbrances. Lenders must provide title insurance and complete title search documentation to prove a clear title. When working with a Certified Development Company (CDC) on a 504 loan, the escrow agent typically handles these title verification documents.

Additionally, lenders should prepare a Lien Instrument of Project Property and a Security Agreement to safeguard the SBA's interest in the collateral.

Title Reports and Property Appraisals

Real estate and equipment appraisals conducted by third parties help determine their market value, which influences loan amounts and terms. Environmental investigation reports are also necessary to identify potential risks or liabilities. Addressing environmental concerns early in the process is critical, as unresolved issues can delay or even derail loan approval.

If your business operates on leased property, you’ll need to provide a copy of the lease or a letter from the landlord detailing proposed lease terms.

Insurance and Compliance Documents

A CAIVRS (Credit Alert Verification Reporting System) report is mandatory to verify that the borrower has no delinquent federal debt, which could affect their eligibility for an SBA-guaranteed loan. This report must show no issues before the loan can proceed to closing.

Beyond appraisals and environmental reports, lenders must submit additional documents to ensure financial and compliance requirements are met. Here’s a quick overview:

| Document Type | Purpose | Submission Requirement |

|---|---|---|

| UCC Lien Search | Verifies no conflicting claims on business assets | Required for collateral security |

| Real Estate Appraisal | Establishes the value of property collateral | Submit copy to SBA |

| Equipment Appraisal | Determines the value of machinery/equipment | Submit copy to SBA |

| Environmental Investigation Report | Identifies potential environmental risks/liabilities | Submit copy to SBA |

| CAIVRS Report | Checks for delinquent federal debt | Required for eligibility |

| Title Insurance | Protects against title defects | Provided to Escrow/CDC |

Each of these documents plays a specific role in verifying collateral, ensuring compliance, and facilitating a smooth loan approval process. Proper preparation and submission of these materials are key to avoiding delays.

sbb-itb-97ecd51

Final Funding and Closing Logistics

Once all third-party reports and collateral documents are finalized, the closing process begins. This involves delivering the necessary documents, disbursing funds, and securely storing records. The goal? To ensure every step taken leads to a compliant and seamless closing.

Document Delivery and Verification

Start by verifying all required documents. Use SBA Form 1050 to confirm that disbursements align perfectly with the approved SBA Loan Authorization.

For SBA 504 loans, lenders rely on SBA Form 2286 (504 Debenture Closing Checklist) to determine readiness for funding. If SBA counsel requests a Complete File Review, borrowers must submit all items listed (1–35) on Form 2303.

Key original documents - like stock certificates, vehicle titles, and executed notes - must be delivered to the appropriate parties. Additionally, lenders are responsible for providing borrowers with SBA Form 722 (Equal Employment Opportunity Statement) during the closing stage.

Once all documents are verified and delivered, attention shifts to tracking the disbursement of funds.

Tracking Loan Disbursements

Each disbursement must strictly follow the approved SBA Loan Authorization. For 7(a) loans that aren’t fully disbursed, lenders use SBA Form 2237 (7(a) Loan Post Approval Action Checklist) to document and monitor any changes.

If the loan involves real estate construction or renovation, specific documents - such as the Certificate of Occupancy and Notice of Completion - must be submitted to the CDC or escrow agent to trigger the final funding. Comparing the settlement statement with actual expenses ensures every dollar is accounted for according to the Use of Proceeds agreement.

After all funds are disbursed and documented, the focus moves to securely storing the finalized paperwork.

Post-Closing Document Storage

Once the closing is complete, securely store the finalized documents. Permanent retention is required for key documents, including the Note (Form 147), Unconditional Guarantee (Form 148), and Settlement Sheet (Form 1050). However, reports like the Environmental Investigation Report and Property Appraisals must be submitted to the SBA instead of simply being retained.

Digitize and archive essential closing documents to prepare for future audits. After the loan is fully disbursed, it transitions into regular servicing under SOP 50 57, effective November 1, 2025.

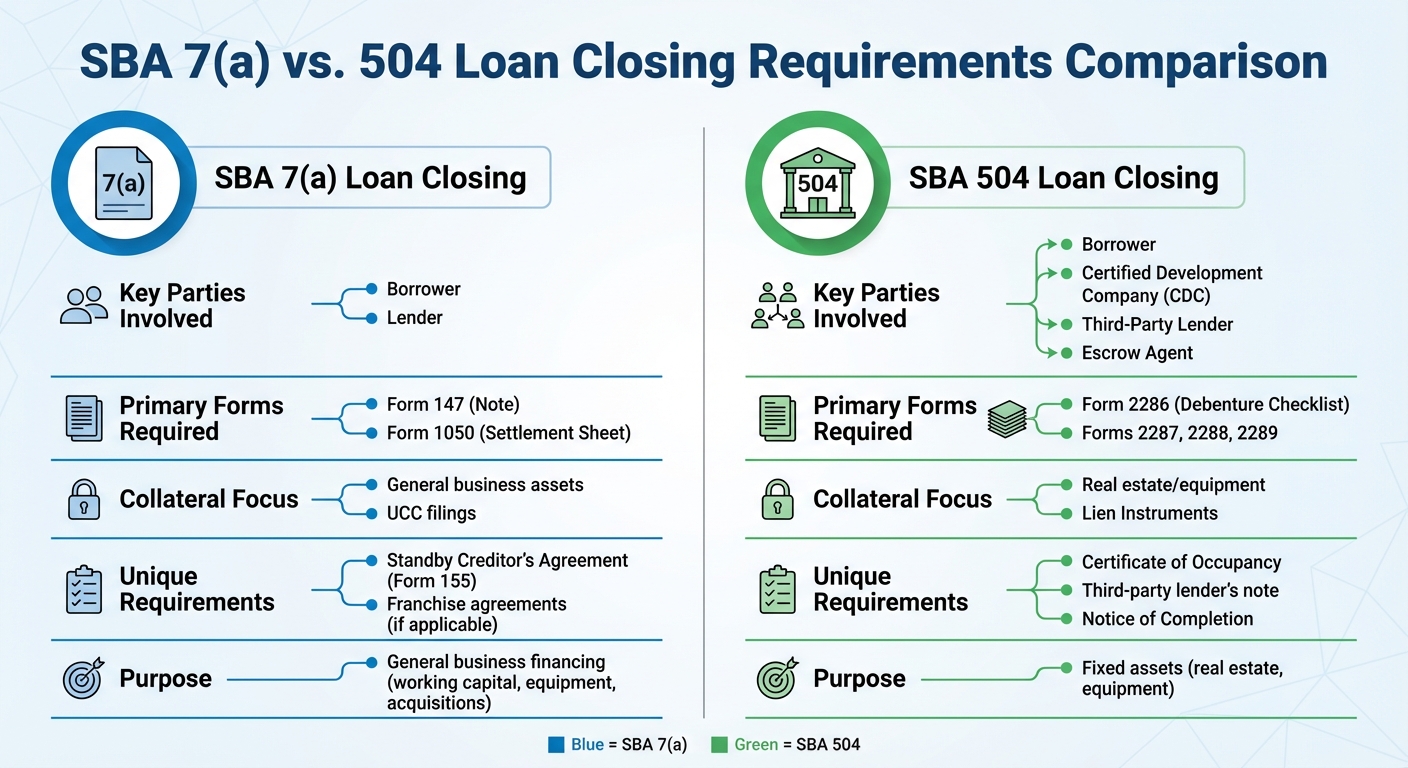

SBA 7(a) vs. 504 Loan Closing Requirements

SBA 7(a) vs 504 Loan Closing Requirements Comparison

The closing process for SBA 7(a) loans and SBA 504 loans is quite different. A 7(a) loan closing primarily involves the borrower and the lender, while a 504 loan requires coordination among multiple parties: the borrower, a Certified Development Company (CDC), a third-party lender, and an escrow agent. These differences not only affect the required documentation but also influence how the final funding is handled.

SBA 7(a) Loan Requirements

The closing process for an SBA 7(a) loan is centered around general business financing needs, such as working capital, equipment purchases, or business acquisitions. Key documents include SBA Form 1050, which certifies the use of loan proceeds, and Form 147, the SBA Note. If the loan involves a franchise, a franchise agreement must be included. For leased spaces, a final lease agreement or a signed Letter of Intent (LOI) is required.

If the loan involves subordinating existing debt to the SBA loan, a Standby Creditor's Agreement (SBA Form 155) must be submitted. This ensures other creditors defer their payments until the SBA loan is repaid. Additionally, all cost-related documents - such as purchase agreements for acquisitions or quotes for furniture, fixtures, and equipment (FF&E) - must be finalized to align with the Settlement Sheet before closing.

SBA 504 Loan Requirements

SBA 504 loans are specifically designed for purchasing fixed assets, such as real estate or equipment. The closing process for 504 loans is more complex due to the involvement of multiple parties. The CDC uses Form 2286 to confirm readiness for funding, while Form 2303 is used for a Complete File Review, which is necessary for the debenture sale.

For projects involving construction or renovation, a Certificate of Occupancy and a Notice of Completion must be submitted to the CDC or escrow agent to trigger final funding. The third-party lender provides their own note and lien instrument, which must be coordinated with the CDC's documentation. Small businesses can refinance up to 90% of the current appraised property value under the 504 debt refinancing program, making property appraisals a critical component. To ensure a smooth process, you’ll need to collaborate closely with your CDC to complete all "Project Property" documentation, including environmental reports and appraisals, in compliance with SBA counsel guidelines for the debenture sale.

| Feature | SBA 7(a) Closing | SBA 504 Closing |

|---|---|---|

| Key Parties | Borrower and Lender | Borrower, CDC, Third-Party Lender, Escrow Agent |

| Primary Forms | Form 147 (Note), Form 1050 (Settlement Sheet) | Form 2286 (Debenture Checklist), Forms 2287, 2288, 2289 |

| Collateral Focus | General business assets, UCC filings | Real estate/equipment via Lien Instruments |

| Unique Requirements | Standby Creditor's Agreement (Form 155), franchise agreements | Certificate of Occupancy, third-party lender's note |

Post-Closing Compliance and Document Submission

Post-closing compliance is essential to keep the SBA guaranty in place. Both borrowers and lenders have specific tasks to complete after closing to ensure compliance. Skipping any step can put the guaranty at risk and may delay final funding, especially for 504 loans that depend on debenture sales.

Recording and Shipping Documents

Start by recording all collateral documents with the appropriate authorities to secure the lender’s position. This includes filing lien instruments and UCC-1 financing statements with the correct county or state offices immediately after closing. For 504 loans, this process involves recording the Lien Instrument of Project Property and the third-party lender's note and lien. If these documents aren’t properly recorded, the collateral may not be enforceable under the law.

For 7(a) loans, specific documents like the Environmental Investigation Report and Property Appraisal must be submitted to the SBA. Additionally, lenders should retain key originals, such as Form 147, Form 148, Form 1050, and Form 159. For 504 loans, Certified Development Companies (CDCs) are responsible for preparing and submitting the full debenture closing package, which includes Forms 1528, 1505, and 1504. This step is critical, as the debenture sale funds the loan itself.

Once the documents are recorded, take time to review the entire funding package to ensure everything aligns.

Reviewing the Funding Package

Carefully examine the complete loan file to confirm it meets SBA guidelines. As 7aSavvy explains, “The lender doesn’t analyze the closing documents to evaluate the business. Instead, they analyze them simply to make sure they’re complete and satisfactory to SBA guidelines and the loan terms and conditions.” Cross-check every document against the loan approval letter to confirm all conditions are met.

For 504 loans, the SBA requires CDCs to use a specific checklist for debenture closings. This checklist outlines all the documents needed for the SBA to approve the debenture sale. Missing documents, such as SBA Form 2286 or Form 2303, can delay or even block the debenture sale, which means the loan won’t be funded. Always refer back to the checklist to avoid these issues.

Maintaining Your SBA Guaranty

After reviewing the documents, ongoing compliance is key to protecting the SBA guaranty. To keep the guaranty valid, lenders must follow the servicing standards outlined in SOP 50 57, which takes effect on November 1, 2025. This involves ensuring the loan remains in "regular servicing" status and adhering to all post-closing conditions. If any loan terms change after closing, lenders must submit modification requests to 7aLoanmod@sba.gov, following the guidelines in SOP 50 10 7.1.

Lenders are also required to provide borrowers with SBA Form 722 (Equal Employment Opportunity Statement) after closing. Keep detailed records of all document submissions, recording confirmations, and communications with the SBA. Staying organized is crucial for maintaining the guaranty and avoiding servicing problems later on.

Conclusion

Closing an SBA loan involves careful attention to detail at every stage. From organizing financial records and proof of equity injection to filing UCC-1 financing statements and submitting third-party reports, each step is essential. These actions not only protect the SBA guaranty but also help ensure timely funding. Missing even one document can lead to delays or jeopardize the guaranty.

The process differs significantly between 7(a) and 504 loans. For 504 loans, coordination with a Certified Development Company (CDC) and an escrow agent is necessary, as the SBA checklist ensures eligibility for the debenture sale. On the other hand, 7(a) loans require critical documentation, including specific reports like appraisals and environmental investigations, which must be submitted directly to the SBA. These distinctions highlight the importance of adhering to the respective checklists to avoid complications and ensure smooth post-closing compliance.

"Most lenders spend up to 70% more time on SBA loans than other loan types. That wasted time can mean frustrated borrowers, missed opportunities, and even risk to the SBA guaranty." – GoDocs

Whether you're closing a 7(a) or 504 loan, using standardized checklists - such as SBA Form 2286 for 504 loans - ensures that all required documents are accounted for before finalizing the process. Conducting a mini-checklist verification during the post-approval phase can help minimize delays and avoid last-minute surprises. After closing, promptly recording collateral documents and adhering to post-closing compliance procedures is equally critical.

FAQs

What are the main differences between the SBA 7(a) and 504 loan closing processes?

The SBA 504 loan closing process requires SBA Forms 2286 and 2303 and includes a thorough review of fixed-asset collateral by a Certified Development Company (CDC). Depending on the project, additional paperwork - like environmental reports, construction plans, or franchise agreements - might also be necessary.

On the other hand, the SBA 7(a) loan closing process relies on standard loan paperwork and skips the need for these specific forms. It’s designed to be more flexible, supporting a variety of purposes such as working capital, acquisitions, or refinancing. This often makes the 7(a) loan process quicker and easier to navigate.

What happens if documents are missing during the SBA loan closing process?

Missing documents can throw a wrench into the SBA loan closing process, often causing delays or even halting the transaction entirely. If critical paperwork isn’t submitted - like financial statements, purchase agreements, or business licenses - the lender might have to pause the process, ask for resubmissions, or, in some cases, stop the deal altogether.

To sidestep these setbacks, make sure you’ve gathered and submitted every required document on time. Keeping everything organized with a detailed checklist can go a long way in ensuring the process runs smoothly and stays on schedule.

What are the key steps to stay compliant after closing an SBA loan?

To keep up with post-closing compliance for an SBA 7(a) or 504 loan, start by carefully reviewing all loan documents. Make sure everything - like the loan note, unconditional guarantee, and borrower certifications - is fully completed, signed, and properly filed.

Once the loan is disbursed, the focus shifts to ongoing compliance. This means keeping an up-to-date loan file with all original documents and any amendments. Regularly monitor financial and collateral requirements, and ensure timely submission of reports, such as the annual compliance agreement and use-of-proceeds certification. It’s also crucial to periodically review the business’s operations to confirm it still meets SBA eligibility standards. Any significant changes, like ownership transitions or major acquisitions, should be promptly reported.

Staying organized and ahead of these requirements helps borrowers maintain good standing with the SBA and steer clear of potential complications.