Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

High customer concentration happens when a few clients contribute most of a business's revenue. This creates risks like revenue instability, reduced valuation, and financial challenges. Losing a key customer can lead to sudden cash flow problems, layoffs, or even business failure. Buyers and lenders often avoid businesses with high concentration, lowering valuations by 30%-40% or requiring contingent payments like earn-outs.

Key Risks:

- Revenue Volatility: Losing a major client can disrupt cash flow and operations.

- Customer Leverage: Big clients may demand discounts or extended payment terms, hurting margins.

- Valuation Impact: High concentration lowers acquisition value and complicates financing.

Solutions:

- Diversify the Customer Base: Add smaller clients, expand to new industries, or upsell existing ones.

- Expand Revenue Streams: Introduce recurring models or cross-sell services.

- Monitor Risks: Regularly review concentration metrics, ensure multiple team members manage key accounts, and consider trade credit insurance.

Tools like Kumo help identify concentration risks early by analyzing business data, making it easier to evaluate acquisition opportunities. Managing concentration proactively can protect revenue and improve business resilience.

Customer Concentration Risk: The Hidden Danger Most Small Businesses Ignore

Risks of High Customer Concentration

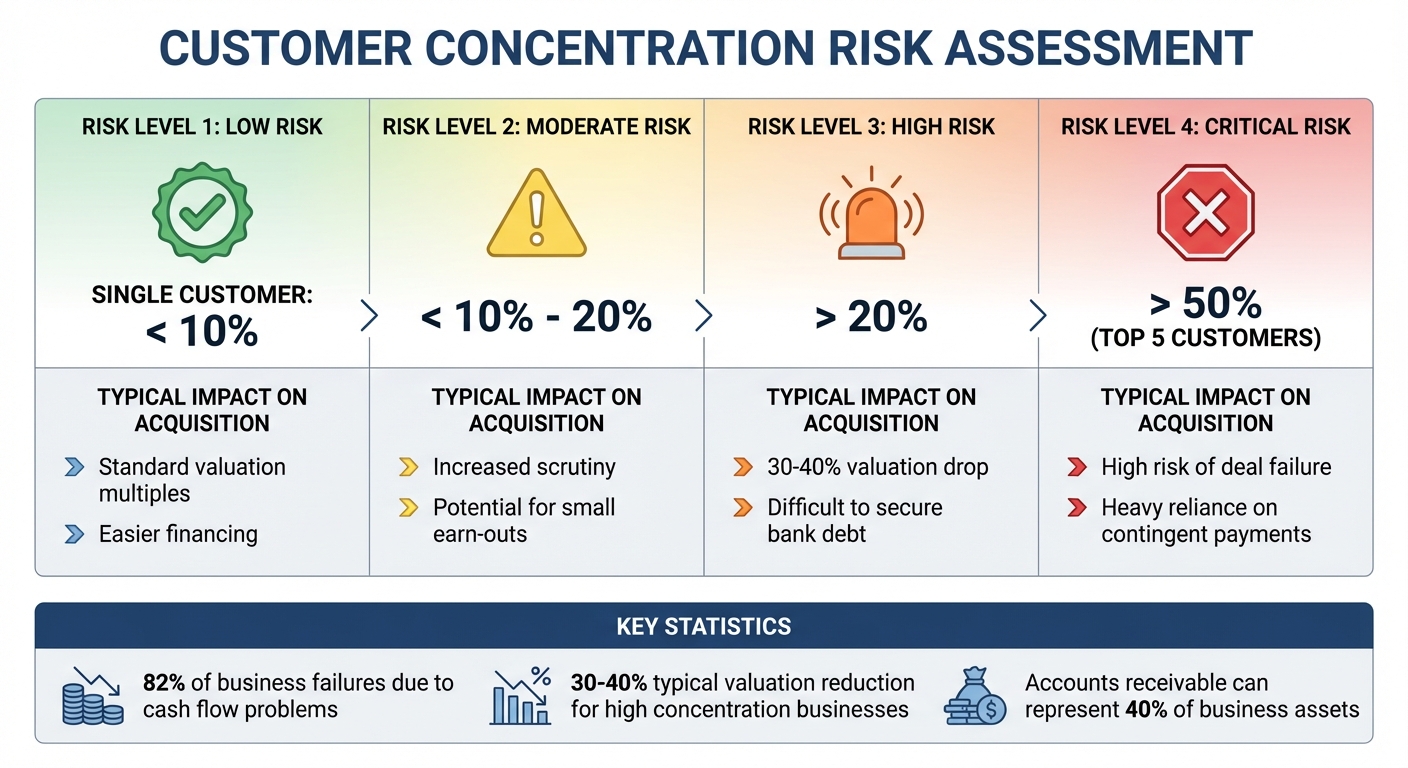

Customer Concentration Risk Levels and Impact on Business Valuation

Understanding the risks tied to high customer concentration is a vital part of due diligence when acquiring small or medium-sized businesses. A heavy reliance on a few clients for the bulk of revenue introduces three major challenges that can derail a deal or jeopardize the long-term health of the business. Let’s break these risks down further.

Revenue Volatility and Financial Instability

Losing a key customer can wreak havoc on cash flow. Consider a Midwest CPA firm where the seller initially claimed their largest client made up 20% of revenue. However, during the Quality of Earnings (QoE) review, investigators uncovered inter-company transactions that inflated the numbers. After adjusting for these, a single external customer actually accounted for over 60% of the company’s revenue, prompting the buyer to walk away from the deal.

Another case from August 2024 involved a business generating $1.4 million in revenue with a 40% EBITDA margin ($550,000). Despite these seemingly strong metrics, the business depended on just two customers, both of whom could terminate their contracts with only 30 days' notice. This risk made traditional bank financing nearly impossible, and experts recommended structuring the deal around earn-outs or vendor take-back notes tied to customer retention.

"I would be weighting consideration heavily to earn-out or VTB tied to customer retention." - Dustin Owen, Managing Director, Longview Growth Partners

The sudden loss of a major client often forces businesses to lay off staff or scramble to pivot their business model. Since accounts receivable - frequently uninsured - can make up 40% of a business’s assets, a departing client can trigger a cash flow crisis that’s tough to bounce back from.

Customer Leverage and Margin Erosion

When a business relies heavily on a few large clients, those customers gain leverage, which can erode profitability. Big clients know their importance and often demand steep discounts or extended payment terms of 90 to 120 days. This puts pressure on working capital and squeezes margins.

"Large customers are often less profitable than smaller ones, in part due to the negotiating leverage that they often attempt to exercise over their vendors." - Mineola Search Partners

Additionally, serving a "whale" client often requires significant investments in staffing, equipment, or custom solutions. These fixed costs can become a burden if the relationship ends, leaving the business with unused resources that weigh down profitability.

Valuation and Growth Constraints

High customer concentration directly impacts acquisition valuations. Businesses with concentrated revenue streams often see their enterprise value drop by 30% to 40%. Buyers tend to apply lower EBITDA multiples to account for the risk and frequently shift payments from upfront cash to contingent structures like earn-outs or seller notes.

| Concentration Level | Risk Assessment | Typical Impact on Acquisition |

|---|---|---|

| Single Customer < 10% | Low | Standard valuation multiples; easier financing |

| Single Customer 10% - 20% | Moderate | Increased scrutiny; potential for small earn-outs |

| Single Customer > 20% | High | 30-40% valuation drop; difficult to secure bank debt |

| Top 5 Customers > 50% | Critical | High risk of deal failure; heavy reliance on contingent payments |

One example highlights how concentration risks can derail deals. A buyer paused negotiations after discovering that 25% of the seller’s revenue came from a single customer. During the delay, the customer learned about the pending sale, explored other providers, and ultimately switched to a competitor. This move caused the entire acquisition to fall apart.

"The number one deal killer? The owner's perception of risk related to operating their company is almost invariably lower than an outside buyer's perception." - Dan Doran, Founder, Quantive

Beyond valuation concerns, high concentration limits operational flexibility. Businesses focused on providing highly customized services to a single client are often seen more as consultancies than scalable enterprises. This perception can further reduce their valuation and restrict opportunities for growth.

Customer Concentration Benchmarks by Business Stage

Thresholds for Early, Growth, and Mature Stages

Customer concentration shifts significantly as businesses evolve. In the early stages - when annual recurring revenue (ARR) is under $2 million - companies often rely heavily on a few key clients. It’s not unusual for a single customer to account for 20% to 50% of total revenue during this period. This dependence is typical as these businesses work on establishing their sales processes and building a foothold in the market.

As businesses grow and reach the next stage (ARR between $2 million and $20 million), the focus turns to reducing reliance on individual customers. At this point, a single customer’s share of revenue should ideally drop to around 15% to 20%, with the top five customers collectively contributing about 30% to 40% of total revenue.

For mature businesses - those with over $20 million in ARR - expectations become even tighter. Institutional buyers and lenders generally look for no single customer to represent more than 10% of total revenue. Additionally, the top five customers together should account for less than 25% of revenue.

| Business Stage | ARR Range | Single Customer Target | Top 5 Customers Target |

|---|---|---|---|

| Early-Stage | Under $2M | 20% - 50% (common but risky) | Often >50% |

| Growth-Stage | $2M - $20M | 15% - 20% (requires diversification) | 30% - 40% |

| Mature-Stage | Over $20M | <10% (standard for financing) | <25% |

These targets provide a framework for identifying potential issues, which are further explored in the warning signs below.

Warning Signs to Watch For

During due diligence, certain red flags can highlight customer concentration risks. One major concern is upcoming contract renewals. If a key customer’s agreement is nearing expiration - especially during or shortly after an acquisition - buyers may hesitate until they can evaluate the likelihood of renewal.

Another issue arises when customer relationships are overly dependent on the business owner. When the founder is the sole contact for major accounts, there’s a greater chance that these customers might leave once the business changes hands.

Hidden concentration is another area to consider. Even if a company has multiple clients, serving a single industry or sector can create what’s known as "end-use concentration" risk. This type of reliance can leave the business vulnerable to downturns in that particular industry.

"Ideally, no single customer should represent more than 15–20% of total revenue." - Chris Barrett, Midwest CPA

Additionally, contract terms can signal potential risks. Provisions like short termination notices or "change of control" clauses - allowing customers to exit if the business is sold - can complicate financing and acquisition deals.

sbb-itb-97ecd51

Solutions to Reduce High Customer Concentration

Addressing high customer concentration requires a proactive approach. Here are several strategies that can help mitigate this risk effectively.

Diversifying the Customer Base

The simplest way to reduce reliance on a few dominant clients is to broaden your customer base. Instead of focusing on just a handful of large accounts, aim to secure a greater number of smaller clients. This approach spreads out the risk, so losing one customer has less impact on your overall revenue.

Expanding into new industries and geographic regions also reduces dependence on a single sector or area. For instance, a manufacturing company that supplies only the automotive industry could face challenges if that sector experiences a downturn. By branching into other markets like healthcare or construction, you create a safety net against sector-specific slowdowns.

Streamlining your onboarding process is another way to make diversification more manageable. When onboarding is efficient and standardized, you can add new clients without dramatically increasing costs. This allows you to serve smaller accounts profitably, even if they contribute less revenue individually.

You can also upsell to smaller existing clients to shift revenue dependency gradually. Offering additional services or products to these clients is often less expensive than acquiring brand-new ones. Over time, this strategy can reduce the dominance of your largest customers without requiring a significant increase in marketing expenses.

Diversifying your customer base is crucial, but reducing risk also means rethinking how you generate revenue.

Expanding Revenue Streams

Adding complementary revenue streams is another way to reduce dependency on major clients. For example, adopting recurring revenue models like subscriptions or maintenance contracts can provide a steady cash flow.

If you've invested in infrastructure to serve a large client, explore ways to use those resources for other customers. However, be cautious about making significant investments solely for one client unless they agree to share the costs.

When pursuing new revenue opportunities, focus on profitability rather than sheer volume. A large client might account for 15% of your revenue but only contribute 5% to your gross profit due to the costs of specialized services. Prioritize scalable offerings that fit into your existing operations over highly customized work that increases reliance on individual clients.

"Measuring the profitability of a relationship, the real value created for your business, is essential. The risk you take by catering to a significant customer should be rewarded by greater profitability." - Robert S. Olszewski, CPA, AMSF Director, Kreischer Miller

Monitoring and Formal Policies

Establishing clear policies and regularly monitoring customer concentration is essential. Experts suggest that no single customer should account for more than 10% to 20% of your annual revenue. Making this a formal guideline helps your sales team prioritize diversification and avoid over-reliance on any one client.

Regular customer segmentation reviews should be part of your routine operations. Don’t just track which clients account for the highest revenue; also analyze concentration by industry, region, and contract terms. This broader analysis can reveal hidden risks, such as overexposure to a single vulnerable sector.

To further protect against dependency, implement relationship diversification policies. If only one person manages a key client, you risk losing that account if the employee leaves. Assign multiple team members to manage major accounts to reduce this vulnerability.

Another tool to consider is Trade Credit Insurance (TCI). Since accounts receivable can make up as much as 40% of a business's assets, TCI offers protection against customer defaults. It can also improve lender confidence, potentially increasing your access to credit. Adjusting sales incentives to reward diversification can also help. For example, cap commissions for existing large accounts and offer bonuses for bringing in clients from new sectors.

How Data Analytics Platforms Help Reduce Risk

Spotting customer concentration risks early can save you from making expensive mistakes, especially when evaluating potential acquisitions. Deal sourcing platforms simplify this process by centralizing data, helping you identify these risks right from the start. Tools like Kumo excel in this area.

Using Kumo for Segmentation Analysis

Kumo aggregates data from over 120,000 business listings, pulling information from hundreds of brokers and all major marketplaces. This gives users access to more than $26 billion in total listings. On top of that, the platform adds around 700 new deals every day.

What makes Kumo stand out is its AI-powered matching technology, which identifies duplicate listings across different sources. Instead of wasting time sifting through the same listings from multiple brokers, you can focus on unique opportunities. Custom filters let you zero in on businesses that align with your risk tolerance. For instance, you can target industries like retail or diversified services, which typically have lower customer concentration risks.

Kumo also offers a daily alert system that notifies you when new listings match your criteria. This feature allows you to evaluate customer concentration risks right away. As Kumo highlights:

Sharp financial analysis separates serious buyers from the rest... They can also spot warning signs, such as declining customer concentration, irregular expenses, or cash flow discrepancies.

Comparing Metrics Across SMBs

After narrowing down potential targets through segmentation, advanced analytics take risk assessment to the next level. Comparing customer concentration metrics across multiple businesses helps you quickly identify which opportunities are within acceptable risk levels and which might need closer scrutiny. For example, pay attention if a single customer accounts for more than 10–15% of revenue or if the top five customers contribute over 25% - these could be red flags requiring further investigation.

Additionally, advanced analytics shed light on cash flow trends, margin stability, and industry benchmarks. This type of analysis is especially important since cash flow issues are a leading cause of business failure. In fact, 82% of businesses that fail do so because of cash flow problems, often triggered by losing a major customer with concentrated revenue.

Conclusion: Managing Risk and Building Resilience

High customer concentration poses a major risk in SMB acquisitions. When a single customer contributes 20% or more of revenue, losing that customer can disrupt cash flow significantly - an issue associated with around 82% of business failures.

Addressing this risk starts with early detection and thorough due diligence. For instance, a due diligence review once revealed hidden customer concentration, prompting a buyer to walk away from a deal. This highlights the importance of using detailed data analysis during the acquisition process.

Tools like Kumo simplify evaluations by consolidating business data. These platforms can pinpoint businesses with balanced revenue streams and flag potential warning signs, such as declining customer metrics.

Beyond detection, managing risk requires strategic actions post-acquisition. Diversifying into new industries or geographic regions, establishing formal policies to monitor customer concentration, and securing key customers with long-term contracts - without change-of-control termination clauses - are all effective measures.

FAQs

What risks are associated with high customer concentration?

High customer concentration can be a serious challenge for businesses. When a major client decides to leave, it can take a heavy toll on your revenue and cash flow, potentially throwing your finances into disarray. Beyond the immediate financial hit, depending too much on one or a handful of clients puts you at a disadvantage during negotiations - they might push for lower prices or demand terms that favor them more than you.

This kind of reliance can also skew how you allocate your resources. You may find yourself dedicating too much time and effort to keeping that client happy, leaving other parts of your business overlooked. On top of that, it can hurt your company's valuation and make securing financing more difficult. Investors and lenders often see high customer concentration as a warning sign, signaling higher risks for your business.

What are the best strategies for reducing customer concentration risk?

Reducing customer concentration risk is essential for keeping your revenue steady and boosting your business's overall value. When a single customer contributes 20% or more of your income, it creates a weak spot - losing that customer could disrupt your cash flow and limit your pricing flexibility.

To address this, start by reviewing your current customer base to spot industries, regions, or product lines that might be underrepresented. From there, consider exploring new markets through targeted marketing campaigns or expanding into different regions to tap into fresh economic opportunities. Offering add-on products or services can also be a smart way to increase sales with smaller clients and grow their accounts over time. Another approach? Build strategic partnerships or enter joint ventures to access entirely new customer networks without requiring a large upfront investment.

Leverage data-driven prospecting tools to streamline your efforts. Platforms like Kumo make it easier to identify potential customers with a more balanced mix, helping small and medium-sized business owners diversify their client base efficiently - whether they're aiming for growth or preparing for a sale.

How can data analytics platforms help identify and manage customer concentration risks?

Data analytics platforms are crucial for spotting and managing customer concentration risks. By processing raw revenue data, these tools deliver actionable insights. For example, they can analyze sales figures to determine what percentage of total revenue each customer contributes. Accounts that surpass a specific threshold - say, 25% of total revenue - are flagged, allowing businesses to quickly pinpoint over-dependence on certain clients.

When it comes to SMB acquisitions, platforms like Kumo simplify this process further. Kumo combines deal sourcing with advanced analytics, enabling users to evaluate a potential acquisition’s customer base early on. It runs concentration analyses to help buyers focus on targets with diversified revenue streams or negotiate safeguards. This approach minimizes the risk of revenue instability post-acquisition.