Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

When buying a small or medium-sized business (SMB), state and local tax policies can have a huge impact on the deal's cost and long-term profitability. States like Florida and Texas offer tax advantages such as no individual income tax, while California and New York impose higher taxes that can complicate transactions. Here's a quick summary:

- California: High taxes on capital gains and property, plus limits on using Net Operating Losses (NOLs) until 2027. However, programs like the Pass-Through Entity Tax (PTET) provide some federal tax relief.

- Texas: No personal or corporate income tax, but a franchise tax applies to businesses earning over $2.65 million annually. Property taxes are high, but incentives like tax abatements can help.

- New York: One of the least tax-friendly states with high personal income and property taxes. Buyers face additional costs like successor liability for unpaid seller taxes.

- Florida: No state income tax for individuals, low corporate tax rates, and reduced property tax burdens. It also removed the commercial lease tax in late 2025, making it an attractive option for SMB acquisitions.

Each state presents unique tax challenges and opportunities that directly affect deal structure, purchase price, and post-acquisition profitability. Using tools like Kumo can simplify the search for businesses in tax-friendly states by providing real-time insights and filters tailored to your needs.

The Tax Mistakes That Can Destroy a Business Acquisition | 799

1. California

In California, capital gains are taxed as ordinary income with no special rates. This means sellers are subject to the state's highest marginal tax rates on their entire gain, which can heavily influence how they price their businesses. These capital gains rules also introduce additional tax challenges tied to property and operational expenses.

Property taxes in California add another layer of complexity. Thanks to Proposition 13, property taxes can only increase by 2% annually until a property is sold or experiences a "change in control." If you acquire over 50% ownership of a small or medium-sized business (SMB) that owns real estate, the property is reassessed at its current market value, and new liabilities are calculated at 1% of that value. Warren Buffett shed light on this disparity in 2003, pointing out he paid just $2,264 (0.056%) in property taxes on his $4 million California home, compared to $14,410 (2.9%) on a $500,000 home in Nebraska.

Another important factor is California's suspension of Net Operating Loss (NOL) deductions for 2024, 2025, and 2026 under SB 167. If you're acquiring a business with accumulated losses, you won't be able to use those losses to offset future income during this period, which could have a direct effect on the business's valuation.

On top of income and property taxes, federal SALT (State and Local Tax) limitations create added challenges for buyers in California. The federal SALT cap hits buyers in high-tax states like California especially hard. However, the state's Pass-Through Entity Tax (PTET) program offers some relief. Extended through 2031, this program lets pass-through entities pay state taxes at the entity level, making them fully deductible for federal taxes and bypassing the $10,000 individual SALT cap. It's worth noting that starting in 2026, missing the June 15 estimated payment deadline reduces the available PTET credit by 12.5%, though it doesn't disqualify participation.

In terms of sales tax, California generally doesn't tax digital goods or SaaS (Software as a Service) products unless there's a transfer of tangible personal property. As Miles Consulting Group explains, "California in general does not impose taxation on digital goods. There must be a transfer of tangible personal property for a product to be taxable". This policy can make technology-focused SMB acquisitions more appealing from a sales tax perspective.

2. Texas

Texas takes a unique approach to taxation, which directly impacts acquisition costs. The state has no personal income tax or corporate income tax, as both are prohibited by the state constitution. Instead, Texas uses a margin-based franchise tax, applicable only when a business generates more than $2,650,000 in annualized total revenue for the 2026-2027 reporting years. Small and medium businesses (SMBs) earning below this threshold are exempt from state-level entity taxes. This stands in stark contrast to states like California, where layered taxes can significantly increase the cost of acquisitions.

For owner-operators, this structure offers a distinct advantage. On average, Texans pay 7.6% of their income in state and local taxes, which is well below the national average of 10.3% and far less than New York's 14.1%. The result? More cash flow remains in your pocket after an acquisition. Additionally, Texas keeps franchise tax rates relatively low - 0.375% for retail or wholesale businesses and 0.75% for other industries.

That said, the savings on income taxes are partially offset by higher property taxes. Texas ranks 7th highest in the U.S., with an effective property tax rate of 1.36%. If you're acquiring a business that owns real estate, this could become a considerable fixed expense. To mitigate this, Texas offers some relief measures. For example, there’s a "circuit breaker" that caps annual appraisal increases at 20% for commercial properties valued at $5,160,000 or less. The state also provides incentives like Chapter 312 tax abatements, which can exempt part or all of a property's increased value for up to 10 years, and the Freeport exemption, which applies to goods in transit.

Before closing on an acquisition, ensure you obtain a Certificate of No Tax Due. Buyers are responsible for any of the seller's unpaid state taxes (including franchise and sales taxes) up to the purchase price unless Form 86-114 is submitted jointly to the Comptroller. Additionally, you'll need to apply for new sales and use tax permits since these cannot be transferred from the seller. If the business owns tangible personal property used to generate income, you must file an annual rendition statement by April 15. Failing to do so triggers a 10% penalty on the total taxes owed for the year. These steps are non-negotiable.

These tax details play a critical role in assessing the overall benefits and challenges, which will be explored further in the next section.

3. New York

New York presents one of the toughest tax landscapes for small and medium-sized business (SMB) acquisitions. The state ranks 50th overall on the 2026 State Tax Competitiveness Index, making it the least competitive tax jurisdiction in the country. This ranking reflects higher transaction costs and reduced after-tax proceeds, especially when compared to more tax-friendly states like Texas or Florida. These challenges add complexity to doing business in New York.

The state’s individual income tax rates range from 4.00% to 10.90%, and for residents of New York City, an additional local tax of 3.876% pushes the top marginal rate even higher. This combined burden is particularly tough on sellers. Unlike other states with preferential long-term capital gains rates, New York’s tax system places significant pressure on those selling their businesses. Eric Bronnenkant, Head of Tax at Edelman Financial Engines, explains:

"High-income earners could face a combined capital gains tax rate exceeding 14.7% – the next highest in the nation is California at 13.3%".

When you factor in federal taxes and the Net Investment Income Tax, a top-bracket New York City resident selling a business could face a total tax rate nearing 38.6%. This steep tax rate not only increases acquisition costs but also makes structuring deals more intricate.

High taxes also influence acquisition valuations. Sellers often push for higher prices to offset their tax liabilities, which can make deals less appealing to buyers. For instance, in the 2022 tax year, high-income earners reporting over $1 million were responsible for more than 75% of all capital gains in the state. To navigate these challenges, buyers might consider strategies like installment sales to spread out gains over several years, helping sellers avoid the top 10.9% tax bracket. Additionally, filing Form AU-196.10 at least 10 days before closing is crucial to avoid inheriting the seller's unpaid sales taxes.

Despite these hurdles, New York does offer some tax incentives. The state fully conforms to federal Section 1202 (QSBS) rules, allowing a 100% tax exclusion on capital gains from qualified small business stock at both state and city levels. Programs like the Excelsior Jobs Program provide refundable tax credits for businesses in strategic industries, while the START-UP NY Program offers a 10-year tax-free period for approved businesses operating in designated zones. These incentives can significantly reduce long-term tax burdens and improve the viability of acquisitions. Corporate tax rates in the state range from 6.5% to 7.25%.

On top of income taxes, New York’s property tax structure adds another layer of cost. The state has an effective property tax rate of 1.26% on owner-occupied housing, ranking 9th highest in the nation. Additionally, New York uses a Pass-Through Entity Tax (PTET) to help high-income earners work around the federal SALT cap. However, taxpayers claiming PTET credits cannot take advantage of the new New York City income tax elimination credit. Beginning in 2026, corporations will also face a higher minimum estimated tax payment of $5,000, up from $1,000, which could help with short-term cash flow planning.

sbb-itb-97ecd51

4. Florida

Florida stands out as a low-tax haven, offering businesses and individuals significant tax advantages. Ranked 5th overall on the 2026 State Tax Competitiveness Index, it shines particularly in individual income taxation. One of Florida's most attractive features is its lack of a state income tax for individuals. This means pass-through entities - like S-corporations, LLCs, and partnerships - pay $0 in state tax on business income reported on personal returns.

For corporations, Florida imposes a 5.5% tax on profits above $50,000, which can help reduce expenses for smaller businesses. Additionally, as of October 1, 2025, the state eliminated its commercial lease tax, removing a financial burden for companies leasing operational space.

Florida's property tax rate is modest, with an effective rate of 0.74% on owner-occupied housing. However, businesses should be aware of the Tangible Personal Property (TPP) Tax, which applies to business assets, with returns due by April 1 each year. New employers also benefit from a reemployment tax rate of 2.7% on the first $7,000 of each employee’s wages during their first 10 quarters.

The state offers several targeted incentives to attract businesses. These include the Rural Job Tax Credit, which provides $1,000 to $1,500 per employee (capped at $500,000), and the Experiential Learning Tax Credit, offering $2,000 per intern, up to $10,000 annually. Manufacturers and R&D-focused businesses can also apply for sales tax exemptions on machinery and equipment, helping to reduce upfront costs. Furthermore, the absence of estate or inheritance taxes makes Florida an appealing choice for long-term business succession planning.

When conducting due diligence in Florida, buyers should ensure the target business has filed its TPP return on time and obtained the necessary local business tax receipts, as requirements differ by county and municipality.

Pros and Cons

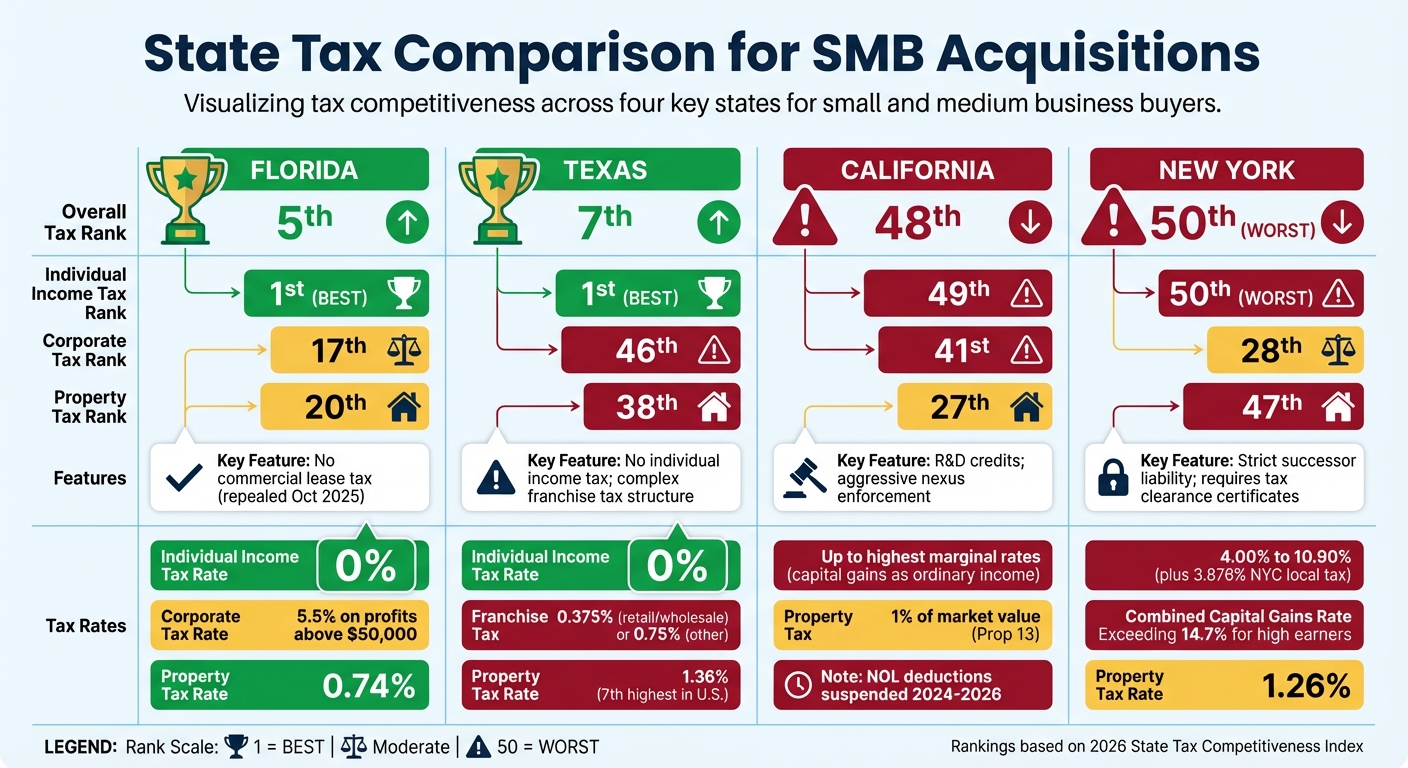

State Tax Comparison for SMB Acquisitions: Florida, Texas, California, and New York

When it comes to SMB acquisitions, each state's tax structure brings its own set of trade-offs. States like Florida and Texas stand out for one major advantage: no individual income tax. For owners of pass-through entities, this means no state tax on business income reported on personal returns, which can be a game-changer during exit planning. The divide between low-tax states, such as Florida and Texas, and high-tax states, like California and New York, is stark and often pivotal for decision-makers.

However, there are complexities to consider. Texas, for instance, leans heavily on property taxes (ranking 38th) and enforces a complicated franchise tax on gross receipts, which drags its corporate tax competitiveness down to 46th place. On the other hand, California and New York impose high individual income tax rates, which are further amplified by the SALT cap. California ranks 49th and New York 50th for individual income tax competitiveness, making them some of the least favorable states in this category.

These tax structures introduce both challenges and opportunities, as highlighted by tax expert David A. Hughes:

"Any taxable gain will likely be treated as 'business income' for state income tax purposes and will be subject to tax wherever the company/target is taxable, which will flow through to the owners of a pass-through entity."

Adding to the complexity, buyers in New York face the risk of inheriting unpaid sales tax debts through successor liability in asset deals if proper bulk sale notifications aren't made. Maria Keating, CPA at Clark Nuber, underscores the importance of due diligence:

"A purchaser should always perform due diligence around state and local tax items to identify risk prior to the acquisition, where this risk and potential liability may transfer to the purchaser."

The table below provides a snapshot of these tax trade-offs across key states:

| State | Overall Tax Rank | Individual Income Tax Rank | Corporate Tax Rank | Property Tax Rank | Key Buyer Incentive |

|---|---|---|---|---|---|

| Florida | 5 | 1 | 17 | 20 | No commercial lease tax (repealed Oct 2025) |

| Texas | 7 | 1 | 46 | 38 | No individual income tax; complex franchise tax structure |

| California | 48 | 49 | 41 | 27 | R&D credits; aggressive nexus enforcement complicates compliance |

| New York | 50 | 50 | 28 | 47 | Strict successor liability; requires tax clearance certificates |

Note: A rank of 1 represents the best, while 50 is the worst.

Using Platforms to Navigate Tax-Driven Acquisition Opportunities

Navigating the tax complexities of acquiring an SMB can feel like a daunting task. In the past, finding the right opportunity in a tax-friendly state meant spending weeks - or even months - trawling through broker websites, marketplaces, and endless listings. But platforms like Kumo have changed the game. By consolidating over 120,000 deals from thousands of brokers and major marketplaces into one searchable database, Kumo simplifies the process. It currently monitors more than $26 billion in business listings, making it a powerful tool for buyers looking to streamline their search.

Buyers can easily zero in on tax-friendly states using geographic filters. Plus, with daily email alerts for new matching listings, they can act fast when the right business in a favorable tax environment becomes available. With over 700 fresh deals added every day, this feature ensures buyers stay ahead of the curve.

Kumo doesn’t just stop at location filters. Its AI-powered analytics offer a deeper layer of insight by connecting regional tax burdens with business performance data. This is key, as tax competitiveness isn't just about statutory tax rates. As the Tax Foundation explains, "Statutory tax rates only tell part of the story... Tax incentives, apportionment, throwback rules, and other factors can have a dramatic impact on effective tax burdens". For instance, Louisiana's tax reforms in 2026 boosted its tax competitiveness ranking, making it a more attractive option for buyers. Kumo’s analytics break down these intricate tax details, turning them into clear, actionable insights.

Another major benefit? Kumo eliminates duplicate listings, ensuring every opportunity is unique. Alex Goldberg, an SMB operator and investor, praises the platform for its openness:

"What really stands out is its transparency - you can literally see which brokers they're scraping and which ones they plan to add next. No other platform I've tested offers that level of openness".

For buyers navigating the maze of state tax policies, tools like Kumo turn what was once a time-consuming process into a strategic, data-driven approach. Whether you're focusing on tax-friendly states like Florida or keeping an eye on shifts in policies - such as Louisiana’s new 3% flat individual income tax - Kumo provides the insights you need to make informed, tax-savvy acquisition decisions.

Conclusion

As we've explored, local tax policies can have a major impact on acquisition costs. The differences between tax-friendly states and those with higher tax burdens translate directly into financial consequences. For example, navigating California's 1.5% S-corp tax or Texas's franchise tax on gross receipts requires a clear understanding of regional tax structures before finalizing any deal. This makes thorough due diligence a critical part of the process.

Smart buyers dig deeper into tax risks, carefully examining successor liabilities and state-specific tax elections. Nexus studies are a common tool to uncover hidden obligations. As Corey L. Rosenthal, JD, explains:

"Understanding the tax profile of the buying and selling entities, the jurisdictions in which each business has operations, and the long-term goals of the parties is key to providing prudent advice".

This highlights the importance of involving state and local tax (SALT) experts early in the process - ideally during the letter of intent stage, rather than waiting until after the deal is finalized.

More buyers are also focusing on acquisitions in states with tax-friendly policies. States like Wyoming, South Dakota, and Florida consistently rank among the top five for tax competitiveness in 2026. Tools like Kumo provide timely updates on favorable tax environments, allowing buyers to turn tax advantages into a strategic edge rather than an afterthought.

FAQs

How do local tax policies influence the valuation of small businesses during acquisitions?

Local tax policies can significantly affect how small businesses are valued, shaping both the buyer's expected cash flow and the total transaction costs. For example, states with high real estate transfer taxes or taxes on asset transfers can drive up the effective purchase price. On the other hand, states offering tax credits or lower corporate income tax rates can boost the potential for future earnings.

The structure of the transaction also plays a big role. Whether it's an asset sale or a stock sale, the tax implications can differ greatly. In an asset sale, the buyer might benefit from tax perks like a stepped-up basis for depreciation, but the seller could face immediate income tax liabilities. Gaining a clear understanding of these tax details early on can help buyers negotiate key terms - like tax indemnities - or decide how to handle transfer tax responsibilities.

Since tax rules can vary widely depending on the location, tools like Kumo are invaluable. They allow buyers to evaluate these factors across multiple listings, making it easier to plan deals and make informed valuation decisions.

What tax benefits are available when acquiring a small business in Florida or Texas?

Acquiring a small business in Florida comes with some appealing tax perks that can make the process more affordable. For starters, Florida doesn’t have a state personal income tax. This means profits from the sale or income earned through pass-through entities won’t be hit with state income tax. On top of that, businesses may benefit from corporate tax incentives like Research & Development (R&D) credits, which can help offset corporate tax obligations for eligible companies. Florida also offers specific tax credits for activities such as job creation or capital investments, potentially reducing your tax load even further after the acquisition.

In Texas, while the state doesn’t offer as many direct tax benefits tied to small business acquisitions, it does share one big advantage with Florida: no personal income tax. This can be a significant financial boost for business owners. Additionally, some small entities may qualify for an exemption from the state’s franchise tax. Programs like the Texas Enterprise Fund also provide financial incentives to businesses that meet certain criteria. To get the most accurate and up-to-date information, it’s a good idea to check state resources or consult the Texas Comptroller’s office.

What steps can buyers take to reduce tax risks when acquiring a business in high-tax states like California or New York?

When dealing with high-tax states like California or New York, it's crucial for buyers to conduct detailed state tax due diligence. This process should uncover any possible liabilities tied to income tax, sales tax, or nexus issues that could arise.

Opting for an asset purchase is one way to help reduce successor liability. Additionally, buyers can negotiate tax indemnities, establish escrow accounts, or strategically allocate the purchase price to mitigate potential tax risks. Seeking advice from a qualified tax professional is a wise move to ensure compliance and minimize exposure to unforeseen tax challenges.