Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

Finalizing an SBA loan doesn’t end your responsibilities - it’s just the beginning. Both borrowers and lenders must handle specific post-closing documentation to comply with SBA rules and protect the loan guarantee. Here’s what you need to know:

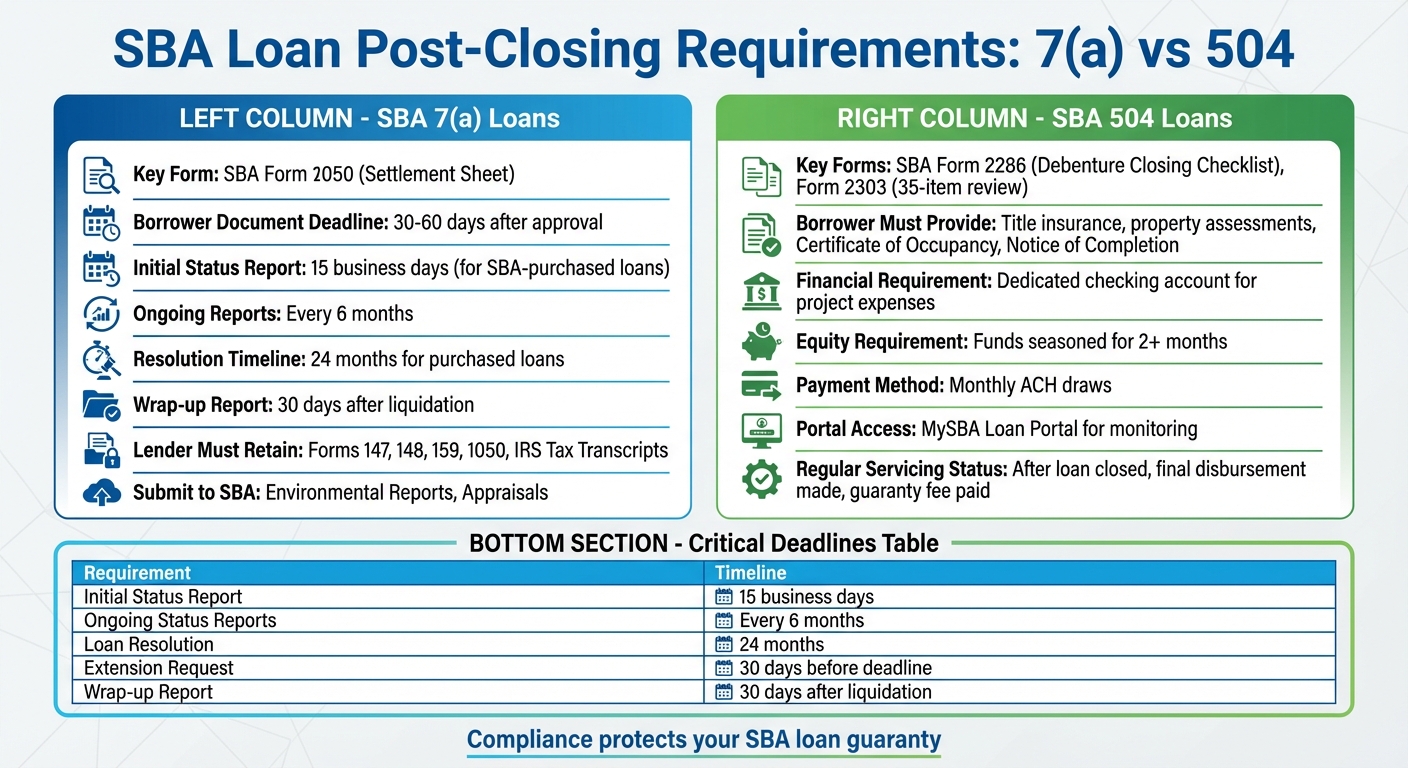

- SBA 7(a) Loans: Lenders must retain key forms like SBA Form 1050, monitor borrower compliance, and meet strict reporting deadlines. Borrowers must ensure funds are used as approved and submit required documents promptly.

- SBA 504 Loans: Certified Development Companies (CDCs) and borrowers must complete debenture closing requirements, including SBA Form 2286, and provide evidence of proper fund use, such as title insurance and project completion documents.

- Key Deadlines: Lenders must submit reports within 15 business days for SBA-purchased loans and resolve issues in 24 months. Borrowers must sign and return closing documents within 30–60 days to avoid approval voidance.

- Document Retention: Both parties must keep critical documents like invoices, receipts, and tax transcripts for audits or reviews.

Staying organized and meeting deadlines is crucial to maintaining compliance and safeguarding the SBA guaranty. Let’s break down the details.

SBA 7(a) vs 504 Loan Post-Closing Requirements Comparison

SBA EIDL Requirements | POST-CLOSING

SBA 7(a) Loan Post-Closing Requirements

Once an SBA 7(a) loan is finalized, both lenders and borrowers must adhere to specific ongoing documentation requirements outlined in SOP 50 57 4, which takes effect on November 1, 2025. These requirements differ significantly from those associated with SBA 504 loans.

Required Forms and Deadlines

The SBA Form 1050 (Settlement Sheet) is a critical piece of post-closing documentation for 7(a) loans. Lenders are responsible for completing this form for every disbursement to confirm that loan proceeds were used as approved and that the borrower's equity injection was made before funds were released.

Borrowers must sign and return their closing documents within 30–60 days of loan approval. Missing this timeframe can result in the loan approval being voided. For loans purchased by the SBA from the secondary market, lenders face even stricter timelines. They must submit an initial written status report within 15 business days of receiving the purchase notice and then provide status updates every 6 months until the loan is resolved. If a loan enters liquidation, lenders have 30 calendar days after completing the liquidation process to submit a final wrap-up report to the Commercial Loan Service Center (CLSC).

While borrowers have specific responsibilities, lenders carry additional obligations to ensure full compliance.

What Lenders Must Do for 7(a) Loans

Lenders are required to permanently retain essential documents such as SBA Forms 147, 148, 159, and IRS Tax Transcripts. Although most records remain in the lender's files, certain documents - like Environmental Investigation Reports and Appraisals - must be submitted directly to the SBA.

Monitoring borrower compliance and collateral is another key responsibility for lenders. Mike Owen, Chief Credit Officer at CDC Small Business Finance, highlights the importance of accurate fee disclosures:

"The latest revamp of the SBA 159 form is unique because now it directly ties proper disclosure and identifies responsible parties to filling out the form to follow regulations and SOP for the agency".

For agent fees exceeding $2,500, lenders must provide detailed accounting.

Ethan Smith, Managing Partner at Starfield & Smith, warns against cutting corners:

"Anyone looking to skirt around the rule and not comply and only get a slap of wrist are kidding themselves".

Failing to comply with these requirements can have serious consequences, including the SBA refusing to honor its loan guaranty, which undermines the entire purpose of obtaining an SBA-backed loan.

SBA 504 Loan Post-Closing Requirements

SBA 504 loans act as takeout financing, with the debenture closing taking place after the project is completed and the interim loan is paid off. Because of this structure, both Certified Development Companies (CDCs) and borrowers must meet specific documentation requirements.

Debenture Closing Documentation

The cornerstone of the debenture closing process is SBA Form 2286 (504 Debenture Closing Checklist). This form is used by CDCs and the SBA to determine if the debenture is ready to be sold, which is essential for funding the loan.

If additional review is needed, CDCs must submit SBA Form 2303, a detailed checklist that includes up to 35 items. The first 13 items are mandatory, and the initial eight are typically prepared by an assigned attorney.

A 504 loan officially enters "regular servicing" status only after three key steps are completed: the loan is closed in accordance with its authorization, the final disbursement is made, and the SBA guaranty fee is paid. Until these milestones are achieved, the loan remains in an approval stage.

| Document/Form Number | Purpose | Responsible Party |

|---|---|---|

| SBA Form 2286 | 504 Debenture Closing Checklist | CDC and SBA |

| SBA Form 2303 | Complete File Review Checklist | Designated Attorney / CDC |

| SBA Form 1505 | Note Assignment to SBA | CDC (Authorized Officer) |

| SBA Form 1528 | Borrower's Agreement | CDC / Borrower |

Borrowers also have specific responsibilities to complete the 504 loan closing process.

What Borrowers Must Do for 504 Loans

Borrowers need to provide title insurance and property assessments as part of their closing package. For construction projects, they must also secure a Certificate of Occupancy and a Notice of Completion to confirm the project's completion.

To ensure proper financial tracking, borrowers should maintain a dedicated checking account specifically for project-related expenses. This helps separate eligible 504 costs from routine business operations and avoids complications during audits. Using personal credit cards for project expenses should be avoided, as it makes the audit trail harder to follow. Borrowers must also keep all invoices, receipts, and proof of payment to demonstrate that the interim loan was used solely for approved project expenses.

Additionally, any owner-equity funds must be seasoned, meaning they should have been in a verifiable account for at least two months before closing. This ensures transparency and prevents last-minute equity contributions that cannot be properly documented. Borrowers should also retain both physical and electronic copies of all legal-entity documents, such as state filings, sales-tax certificates, and DUNS numbers.

sbb-itb-97ecd51

Compliance Obligations After Closing

After the loan closes, both lenders and borrowers have ongoing responsibilities to ensure the loan is managed properly, the SBA guaranty is protected, and transparency is upheld.

Lender Compliance Requirements

Lenders managing 7(a) loans take on servicing duties once a loan moves into either "regular servicing" or "liquidation" status, as outlined in SOP 50 57 4 (effective November 1, 2025). For loans purchased by the SBA, lenders must meet specific reporting deadlines, which require close attention.

- Initial Status Report: Within 15 business days of receiving notice that the SBA has purchased its guaranty from the secondary market, lenders must submit an initial status report to the Commercial Loan Service Center (CLSC).

- Ongoing Reports: Every six months, lenders must provide written updates to the SBA, covering key details about the borrower and collateral.

Lenders are required to resolve SBA-purchased loans within 24 months of purchase through one of the following methods:

- Returning the loan to regular servicing with documented payment terms.

- Confirming the loan is paid in full and verifying this in E-Tran.

- Submitting an SBA-approved wrap-up report after completing liquidation.

If circumstances like bankruptcy or judicial foreclosure delay progress, lenders must request an extension in writing from the CLSC at least 30 calendar days before the deadline. Once liquidation is finalized, lenders have 30 calendar days to electronically submit the wrap-up report.

| Requirement | Timeline |

|---|---|

| Initial Status Report (Secondary Market Purchase) | Within 15 business days of notice |

| Ongoing Status Reports (Purchased Loans) | Every 6 months |

| Resolution of SBA-Purchased Loan | Within 24 months of purchase |

| Extension Request Submission | 30 days before deadline |

| Wrap-up Report Submission | 30 days after liquidation complete |

While lenders handle these tasks, borrowers also have their own set of obligations to ensure compliance.

Borrower Compliance Requirements

Borrowers must meet specific documentation and reporting standards to stay in compliance with their loan agreements and SBA rules. This includes submitting SBA Form 770 (Financial Statement of Debtor) or standard business financial statements, especially during loan servicing actions or when seeking an Offer in Compromise. Borrowers must also certify the correct use of loan proceeds using SBA Form 1050 (Settlement Sheet) or equivalent documentation, and adhere to the terms outlined in SBA Form 601 (Agreement of Compliance) provided at loan closing.

For 504 loans, payments are typically processed through monthly ACH draws, though other payment methods are available. Borrowers whose 504 debentures have been purchased by the SBA should set up an account in the MySBA Loan Portal to monitor loan activity and manage payments online. To address questions about account balances, due dates, or loan terms, borrowers are encouraged to maintain regular contact with their Certified Development Company (CDC).

Document Retention and Submission

How Long to Keep Documents

Lenders are required to retain key closing documents, including SBA Form 147 (Note), SBA Form 148 (Unconditional Guarantee), SBA Form 1050 (Settlement Sheet), and SBA Form 159 (Fee Disclosure), in their internal files instead of submitting them immediately to the SBA. These records must remain accessible for potential SBA audits or guaranty purchase reviews.

To verify proper use of loan funds, lenders should also maintain supporting documents such as invoices, receipts, and canceled checks. As Jennifer E. Borra, Attorney at Starfield & Smith, explains:

"SBA cites failure to use loan proceeds as required by the SBA loan authorization as one of the most common lender deficiencies noted in PLP audits and guaranty purchase reviews".

When lenders take independent servicing actions, it’s essential to document the business rationale and justification thoroughly. These records should be stored in the loan file for future SBA reviews.

Here’s a quick reference for document retention and submission requirements:

| Document Type | Retention/Submission Requirements |

|---|---|

| SBA Form 147 (Note) | Retain in lender's internal file |

| SBA Form 148 (Unconditional Guarantee) | Retain in lender's internal file |

| SBA Form 1050 (Settlement Sheet) | Retain in lender's internal file |

| SBA Form 159 (Fee Disclosure) | Retain in lender's internal file |

| IRS Tax Transcripts | Retain in lender's internal file |

| Environmental Investigation Report | Submit copy to SBA |

| Appraisal | Submit copy to SBA |

Electronic Submission Methods

After retaining the necessary documents, the SBA provides several electronic submission options to streamline the process. For 7(a) loan modification requests, lenders can email 7aLoanmod@sba.gov. Post-servicing actions for the Fresno Commercial Loan Service Center (CLSC) can be sent to FSC.PostServicing@sba.gov or uploaded to designated Box.com folders.

Routine updates, such as address changes or maturity date extensions, can be managed through E-Tran, with no additional notification required.

For borrowers with 504 debentures, loan details and payments can be handled through the MySBA Loan Portal at lending.sba.gov, which is compatible with modern web browsers.

Conclusion

What Borrowers and Lenders Need to Remember

For both borrowers and lenders, staying organized and disciplined after the loan closing is critical. When it comes to post-closing documentation for SBA loans, accuracy and timeliness are non-negotiable. Lenders must keep all key closing documents on file to maintain the SBA guarantee during audits or liquidation processes. On the other hand, borrowers should ensure their financial records are accurate, especially when submitting an Offer in Compromise using SBA Form 1150.

Meeting deadlines is equally important. Lenders are required to submit regular status reports and resolve issues within 24 months to retain the SBA guarantee. The process is made easier through digital tools like E-Tran and designated email channels, which simplify routine updates and modification requests .

Both parties benefit from proactive documentation management. For lenders, requesting deadline extensions at least 30 days in advance can help address unexpected delays. Borrowers, meanwhile, should double-check certifications and tax transcript authorizations to avoid any hold-ups in disbursement. These practices not only protect the loan relationship but also ensure the SBA guarantee remains intact.

FAQs

What documents are required after closing an SBA 7(a) loan?

After finalizing an SBA 7(a) loan, lenders are required to keep several important documents on file. These include the loan note (Form 147), unconditional guarantee (Form 148), and the settlement sheet or use-of-proceeds certification (Form 1050). Other essential forms to retain are the fee-disclosure agreement (Form 159), borrower certifications, standby-creditor agreement (Form 155), compliance agreement (Form 601), and the borrower’s IRS tax transcript. Additionally, lenders should maintain the environmental investigation report and appraisal that were submitted during the loan process.

Borrowers, on the other hand, will receive necessary SBA forms, such as Form 722, as part of the post-closing process. Properly completing and storing these documents is critical to meeting SBA compliance requirements.

What steps should borrowers take to meet SBA 504 loan closing requirements?

To finalize an SBA 504 loan, borrowers need to submit all the documents outlined in the SBA 504 closing checklist. These usually include items like the CDC board resolution, debenture, title insurance, UCC filings, construction and occupancy certificates, lien and security agreements, borrower certifications, tax transcripts, and any conditional documents, such as environmental reports or franchise-related paperwork.

Timely responses to requests from your lender or the SBA for additional information or documents are crucial. Staying organized and keeping open lines of communication with your lender can make the closing process much smoother.

What happens if I miss documentation deadlines for my SBA loan?

Missing post-closing documentation deadlines for an SBA loan can have serious repercussions. For borrowers, this could mean delays in receiving funds, outright denial of the loan, or even default. In the worst-case scenario, defaulting might lead to personal liability under the loan guarantee. On the lender’s side, they might pause disbursements or refuse to finalize the loan until all necessary forms - like SBA Forms 147, 148, 1050, and borrower certifications - are properly submitted and verified.

If these documentation problems persist, the loan might move into liquidation. This could fast-track repayment demands, lead to asset seizures, or even result in the loss of the SBA guarantee. Delays in submitting critical items such as environmental reports, appraisals, or financial statements can also drive up costs and throw project timelines off course.

To steer clear of these challenges, make sure all post-closing paperwork is completed accurately and submitted on time. This not only safeguards your loan eligibility but also ensures the process remains smooth for both you and your lender.