Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

If you're buying a business with an SBA loan, understanding the tax rules can save you money and prevent mistakes. Here's what you need to know:

- Interest on SBA loans is tax-deductible if the funds are used for business purposes.

- SBA loan proceeds are not taxable income, but how you allocate and report them matters for deductions.

- Principal payments are not tax-deductible, but they affect your asset basis, which impacts depreciation and gains.

- Guaranty fees and origination costs must be deducted over time, not upfront.

- Proper purchase price allocation (using IRS Form 8594) is key to maximizing depreciation and amortization benefits.

- Asset purchases often offer better tax perks than stock purchases due to depreciation advantages.

To stay compliant and maximize benefits, keep detailed records, follow IRS rules, and consult with a CPA. Smart structuring and planning can significantly improve your tax outcomes.

Is The Loan I Took To Buy A Business Deductible?

How SBA Loan Expenses Are Taxed

SBA Loan Tax Deductions Guide: What's Deductible vs Non-Deductible

Understanding how SBA loan expenses are taxed can help reduce costs and ensure compliance with IRS regulations. Not every expense tied to an SBA loan qualifies for deductions, so knowing the rules is key to making the most of your deductions while staying within the law. Here's a breakdown of how different SBA loan expenses are handled for tax purposes.

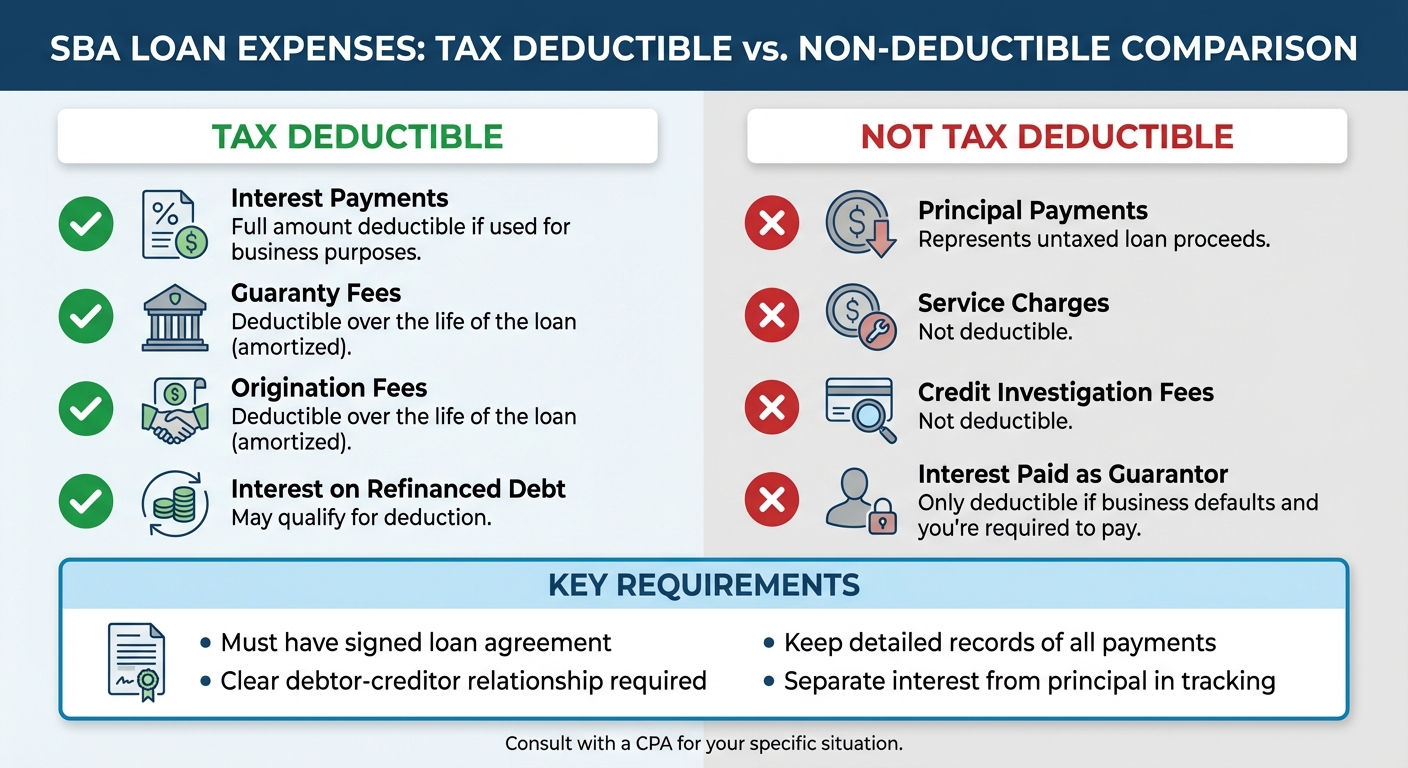

Deducting SBA Loan Interest

If you’re using SBA loan funds exclusively for business purposes, the interest on the loan is tax-deductible. To qualify, you’ll need a signed loan agreement and a clear debtor-creditor relationship. Many small businesses are not subject to interest deduction limits, meaning they can deduct the full amount of interest paid. Additionally, if you’ve used your SBA loan to refinance existing business debt, the interest on the new loan may also qualify for a deduction. To back up your deduction claims, keep detailed records of your loan agreement and interest payments - this documentation is critical for IRS compliance.

How Guaranty Fees and Other Costs Are Treated

Upfront costs, such as guaranty fees, are handled differently than ongoing interest payments. These fees, often referred to as "points", must be deducted gradually over the life of the loan. Similarly, origination fees and financing charges are also spread out across the loan term for tax purposes. However, some fees, like service charges and credit investigation fees, are not deductible at all. If you personally guarantee the loan, keep in mind that you can’t deduct interest payments as a guarantor unless the business defaults and you’re required to cover those payments.

Principal Payments and Basis Adjustments

Principal payments on an SBA loan aren’t deductible. Since the principal represents untaxed loan proceeds, repaying it doesn’t reduce your taxable income. It’s important to track your payments carefully to separate deductible interest from non-deductible principal. These principal payments also impact your basis, which is used for calculating depreciation and gains or losses on your assets.

Asset Purchases and How to Allocate Purchase Price

Why SBA Loans Often Fund Asset Purchases

SBA loans are frequently used to finance asset purchases because they allow businesses to benefit from depreciation deductions. When you buy assets like machinery, equipment, buildings, vehicles, or furniture, you can claim depreciation deductions, which help spread the cost of these items over several years. This, in turn, reduces your taxable income over time.

These loans are structured to align with depreciation schedules, making them an attractive option for buyers. While sales agreements can be structured as either asset or stock purchases, the depreciation advantage typically makes asset purchases more appealing for those aiming to maximize tax benefits.

For an asset to qualify for depreciation, it must meet specific criteria: your business must own the property, use it for business or income-generating purposes, have a determinable useful life, and expect it to last more than one year. However, land itself isn’t depreciable, though buildings and certain improvements to land are. If the property was placed into service after 1986, depreciation calculations are done using the Modified Accelerated Cost Recovery System (MACRS). Understanding these criteria is crucial because they directly impact how the purchase price is allocated and reported on IRS Form 8594. This step is key to maximizing the tax benefits of your purchase.

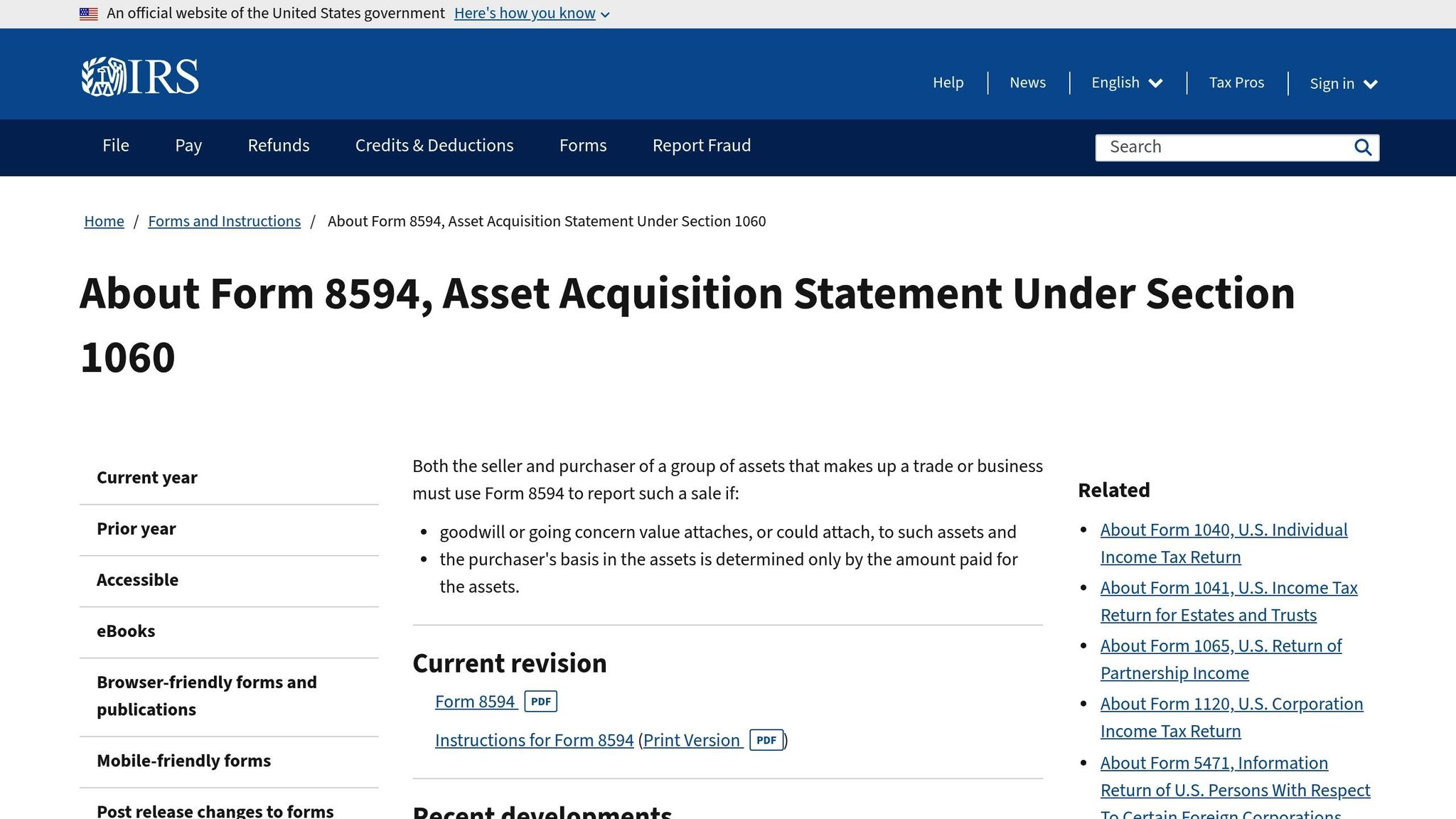

Allocating Purchase Price and IRS Form 8594

Allocating the purchase price correctly is essential for optimizing depreciation benefits. The way you divide the purchase price among various assets can significantly affect your tax situation. Both the buyer and the seller are required to use the IRS-approved "residual method" to allocate the purchase price. This allocation determines the tax basis for depreciation and amortization.

This process is documented on IRS Form 8594 (Asset Acquisition Statement Under Section 1060). Both the buyer and seller must file this form when the transaction involves a trade or business, particularly if goodwill or going concern value is part of the deal. The form requires a detailed breakdown of how the purchase price is distributed across asset categories. To ensure accuracy, refer to the IRS Instructions for Form 8594, which provide step-by-step guidance.

Depreciation and Amortization Rules

Once the purchase price is allocated, you can start claiming deductions through depreciation and amortization. Tangible assets like equipment and vehicles are depreciated over their useful lives using MACRS, while intangible assets - such as goodwill, intellectual property, or customer lists - are amortized over time.

There are also ways to accelerate these deductions. Section 179 depreciation allows you to deduct the full cost of qualifying assets in the year they are placed in service, rather than spreading the deductions over several years. Similarly, bonus depreciation enables you to front-load deductions, offering immediate tax relief that can significantly reduce your taxable income in the year of acquisition. These tools provide flexibility, allowing you to align your deductions with your business’s financial strategy.

sbb-itb-97ecd51

Compliance and Reporting Requirements

Ensuring proper compliance and accurate tax reporting is crucial when working with SBA-financed deals. These steps not only help you meet legal obligations but also maximize the benefits of your loan.

Federal and SBA Program Requirements

To qualify for SBA loan funds, your business must be a U.S.-based, for-profit entity that adheres to SBA size standards and avoids restricted industries. Additionally, any individual owning 20% or more of the business may need to provide an unlimited personal guarantee for the loan.

Once you receive the funds, strict rules govern how they can be used. SBA loans are designated for specific business purposes, such as purchasing assets (both tangible and intangible), supporting working capital, or refinancing existing debt. However, these funds cannot be used for passive investments, speculative ventures, or non-essential purchases. Your lender will also require regular financial reports and adherence to loan covenants. This means your tax strategy must align with these requirements to avoid breaching loan terms. Proper tax reporting plays a critical role in maintaining compliance.

Tax Reporting and Payment Obligations

Tax reporting begins with the asset allocation agreed upon in IRS Form 8594. Mistakes in this allocation can lead to audits and penalties. Depending on your business structure - whether it's a sole proprietorship, LLC, S corporation, or C corporation - you'll need to file the appropriate entity-level tax returns.

If you anticipate owing $1,000 or more in taxes, you must make estimated quarterly tax payments. Missing these deadlines - April 15, June 15, September 15, and January 15 - can result in penalties. Additionally, interest payments on SBA loans are typically deductible as business expenses, so it's essential to track and report them accurately. Keep thorough records, including loan agreements, payment receipts, and other supporting documents, to ensure compliance and defend deductions in case of an audit.

Common Tax Mistakes to Avoid

One common mistake is misclassifying workers as independent contractors instead of employees, which can result in hefty penalties. Another frequent error is mixing personal and business expenses. To avoid this, maintain separate accounts and only claim deductions that your business legitimately qualifies for. Inconsistent asset allocations between buyer and seller on Form 8594 can also catch the IRS's attention.

Poor documentation is another major issue. Without proper records - like payment receipts, loan agreements, and invoices - you may struggle to justify deductions during an audit. Even small oversights, like forgetting to sign your tax return, can lead to unnecessary delays. A CPA from the Midwest emphasizes:

"Proactive coordination between your CPA and lender is key to staying in full compliance".

Collaborating with experienced tax professionals can help you sidestep these challenges and set up your deals for optimal tax outcomes from the beginning.

Tax Planning Strategies for SBA-Financed Deals

Tax planning isn’t something to leave for later - it starts before you even sign the purchase agreement. The way you structure your deal can have a lasting impact on your tax responsibilities.

Structuring Deals for Better Tax Results

Asset purchases often come with better tax perks than stock purchases. Why? Because when you buy assets instead of equity, you can "step up" the tax basis of those assets. This means you can claim higher depreciation and amortization deductions over time, which reduces your future tax bill.

One of the smartest moves you can make is negotiating the purchase price allocation. Work with the seller to structure the deal in a way that maximizes your immediate tax deductions. For instance, tangible assets like equipment or vehicles might qualify for accelerated depreciation, giving you upfront tax savings. On the other hand, intangible assets like goodwill or customer lists are amortized over 15 years, spreading out the deductions. As a CPA from the Midwest puts it:

"The deal structure has a direct impact on your tax situation for years to come."

Interestingly, SBA lenders usually favor asset purchase structures, which aligns well with these tax advantages. If the seller insists on a stock sale, be aware that you could miss out on these benefits.

This initial deal structure also lays the groundwork for selecting the right business entity and planning your tax strategy post-acquisition.

Choosing the Right Entity and Post-Acquisition Planning

The type of business entity you choose affects your taxes, how you operate, and even your exit strategy. If you plan to actively manage the business, an S corporation might be a smart choice. Why? Gains from an S corporation sale aren’t subject to the 3.8% Medicare tax on net investment income, unlike those from a C corporation.

Here’s a quick breakdown of some common entity types:

- Sole proprietorships and single-member LLCs: Simple to set up, but you’ll face higher self-employment taxes.

- Multi-member LLCs and partnerships: Offer flexible profit-sharing options but come with more complex reporting requirements.

- S corporations: Help active owners avoid the 3.8% Medicare tax on sale proceeds but come with stricter ownership rules.

- C corporations: Easier to raise capital with, but you’ll face double taxation and a heavier overall tax burden.

It’s crucial to finalize your entity choice before closing the deal. Switching structures down the road can lead to unexpected tax issues. Work closely with your CPA and SBA lender to ensure your choice aligns with the loan’s requirements and your long-term goals.

Using Deal Sourcing Tools to Find SBA-Eligible Businesses

Once your deal structure and entity choice are clear, the next step is finding an SBA-eligible business that fits your criteria. Kumo simplifies this process by consolidating listings from various marketplaces, brokerages, and proprietary sources into one platform.

Kumo’s custom filters let you zero in on businesses that qualify for SBA financing while meeting your specific needs. Thanks to its AI-powered tools and data analytics, you can quickly evaluate whether a target business has the right financial profile. You can even set up alerts for new opportunities, track listing changes over time, and export data for deeper analysis.

This upfront research ensures that when you sit down with your CPA to plan tax strategies, you already have a clear understanding of the business’s assets, revenue structure, and potential allocation opportunities. It’s a time-saver that sets you up for smarter decisions down the line.

Conclusion

Understanding SBA loan tax rules is a critical step in ensuring a successful business acquisition. These loans are not considered taxable income since they must be repaid, but the real advantage lies in the potential tax benefits. These include deductible interest payments, depreciation on tangible assets, and the amortization of intangible assets like goodwill and customer lists over 15 years.

How you structure your deal also plays a major role in your tax outcomes. Asset purchases often provide better opportunities for depreciation and amortization compared to stock purchases, making them a preferred choice for many buyers. It’s also important to note recent rule changes, effective June 1, 2025, that introduce stricter requirements. These include tighter citizenship rules for owners, mandatory collateral for most loans exceeding $50,000, and a minimum 10% equity injection for new businesses. These updates underscore the importance of careful deal structuring from the start.

Compliance is another cornerstone of effective tax planning. Maintaining detailed records of your loan agreement and interest payments is essential. Collaborate closely with your CPA and SBA lender to ensure your tax strategy aligns with loan covenants. This approach can help you avoid common pitfalls such as errors in purchase price allocation or incomplete documentation.

Smart deal sourcing can also strengthen your tax strategy. Platforms like Kumo bring together listings from various sources, allowing you to filter for SBA-eligible businesses. Its AI-driven analytics let you quickly evaluate financial profiles, while deal alerts notify you of new opportunities that match your criteria. With this level of preparation, you can approach your tax advisor with a clear understanding of the business’s asset structure and revenue, saving time and enabling more informed tax planning.

FAQs

What are the best ways to maximize tax benefits when using an SBA loan to buy a business?

To make the most of tax benefits with an SBA loan, it’s important to know that loan proceeds are not considered taxable income. This means you don’t report the funds as revenue. Instead, your focus should be on deductible expenses, such as the interest paid on the loan, which is typically fully deductible for small business acquisitions. Most small businesses remain under the $2.5 million adjusted taxable income threshold, so interest deduction limits are rarely an issue.

When acquiring a business, you can allocate the purchase price between tangible assets (like equipment or real estate) and intangible assets (such as goodwill or patents). Tangible assets often qualify for depreciation or can be expensed under Section 179 or bonus depreciation, providing tax savings over time. Additionally, fees associated with the loan - like origination or appraisal costs - need to be capitalized and amortized over the loan’s term. However, the annual amortization expense is also deductible.

For added efficiency, tools like Kumo can help identify acquisition opportunities that align with SBA criteria and include well-defined assets. Businesses with a significant amount of depreciable assets offer a double tax advantage: reducing taxable income now with interest deductions and in the years ahead through depreciation. To fully benefit, careful planning and accurate record-keeping are essential.

What are the main tax differences between buying a business through an asset purchase versus a stock purchase?

When purchasing a business through an asset purchase, the buyer gains a tax advantage known as a step-up in the tax basis for the acquired assets. This allows the buyer to depreciate or amortize the assets based on their purchase price, which can lead to larger tax deductions and reduce taxable income over time. Another benefit is the flexibility to choose specific assets and liabilities to acquire, helping the buyer sidestep any unwanted legacy liabilities that could pose future tax risks.

On the other hand, a stock purchase involves buying the entire business entity, including all its assets and liabilities. In this case, the tax basis of the assets stays the same as it was for the seller, meaning there’s no step-up and no immediate boost in depreciation or amortization deductions. While this structure is useful for preserving existing contracts, licenses, and goodwill, it also means the buyer inherits any hidden or contingent tax liabilities tied to the business.

How can I ensure my business complies with SBA loan tax rules?

To ensure you’re following SBA loan tax rules, it’s important to know that the loan proceeds themselves aren’t considered taxable income. They’re classified as a financing transaction. However, the interest you pay on the loan might qualify as a deductible business expense - so long as it meets IRS requirements and is properly documented.

Make sure to keep thorough records, including your loan agreement, payment statements, and details on how you’ve used the funds for your business. When it’s time to file your taxes, report any interest deductions on the appropriate tax form for your business type (like Schedule C for sole proprietors or Form 1120 for corporations). Also, review IRS guidelines for any limits on interest deductions and double-check that your filings are accurate and complete. Staying organized and detailed in your reporting will help you stay on the right side of tax regulations.