Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

Cash flow is the most reliable indicator of a business's financial health and directly impacts its valuation. Unlike revenue or net income, which can be distorted by accounting methods, cash flow shows the actual movement of money - what’s available to cover expenses, pay debts, and reward investors. A steady, positive cash flow increases a business's value by reducing risk, while erratic cash flow patterns signal instability, even if profits look strong on paper.

Key points:

- Operating Cash Flow (CFO) is the most critical cash flow metric, reflecting money generated from daily business activities.

- Discounted Cash Flow (DCF) models are widely used, with 78.8% of analysts relying on them for valuation.

- Businesses with consistent cash flow enjoy higher valuations due to lower perceived risk and better predictability.

To maximize valuation, businesses should focus on maintaining stable cash flow, managing debt wisely, and addressing common issues like seasonal fluctuations or high client concentration. Tools like Kumo simplify cash flow analysis, helping investors and buyers make informed decisions quickly.

Discounted Cash Flow Model | Quickly Value a Business

sbb-itb-97ecd51

Why Cash Flow Determines Business Value

Cash Flow Metrics and Their Impact on Business Valuation Risk Assessment

Cash flow plays a critical role in determining a business's value because it shows the actual money available to cover expenses, pay off debt, and reward investors. A business might report strong net income, but without enough liquid cash to meet its obligations, its value can take a significant hit. In fact, 78.8% of analysts rely on discounted cash flow (DCF) methods when valuing businesses. This makes understanding the relationship between cash flow and business value essential for accurate valuation and risk assessment.

When a business generates steady, positive cash flow, it proves that its operations are sustainable and capable of turning sales into real cash. This reliability lowers the risk for potential buyers, resulting in a reduced discount rate in valuation models, which ultimately increases the business’s present value. This connection highlights why consistent cash flow is so valuable - and why volatility can be a red flag.

Consistent Cash Flow Increases Business Value

Predictable cash flow patterns significantly boost a business's value. Why? Because they enable accurate forecasts of future earnings. On the flip side, businesses with unpredictable cash flow often face higher discount rates due to the uncertainty, which lowers their overall valuation.

"A company with consistent positive cash flow is generally seen as more stable and valuable." - Bryson Havner, H&H Accounting Services

Stable cash flow also reflects operational efficiency. It shows that the business can run smoothly without constantly relying on outside funding or emergency measures. For buyers, this self-sufficiency is especially appealing because it represents discretionary funds that can be allocated to dividends, debt repayment, or reinvestment. Analysts, for instance, favor Free Cash Flow to the Firm (FCFF) models nearly twice as often as Free Cash Flow to Equity (FCFE) models, emphasizing the importance of cash available for immediate use. While consistent cash flow adds value, any signs of volatility can raise concerns about risk.

Cash Flow as a Risk Indicator

While consistent cash flow is a strength, erratic cash flow can signal financial instability. Lenders and investors closely examine cash flow statements to assess whether a business can handle its debt payments. Perceived risk directly impacts the discount rate applied to future cash flows: the higher the risk, the higher the discount rate, which lowers the business's present value. On the other hand, businesses with strong, stable cash flow enjoy lower discount rates, enhancing their valuation.

This is why maintaining a cash reserve and managing accounts receivable effectively are essential for business owners preparing to sell. These actions demonstrate financial stability and reduce the perceived risk for buyers.

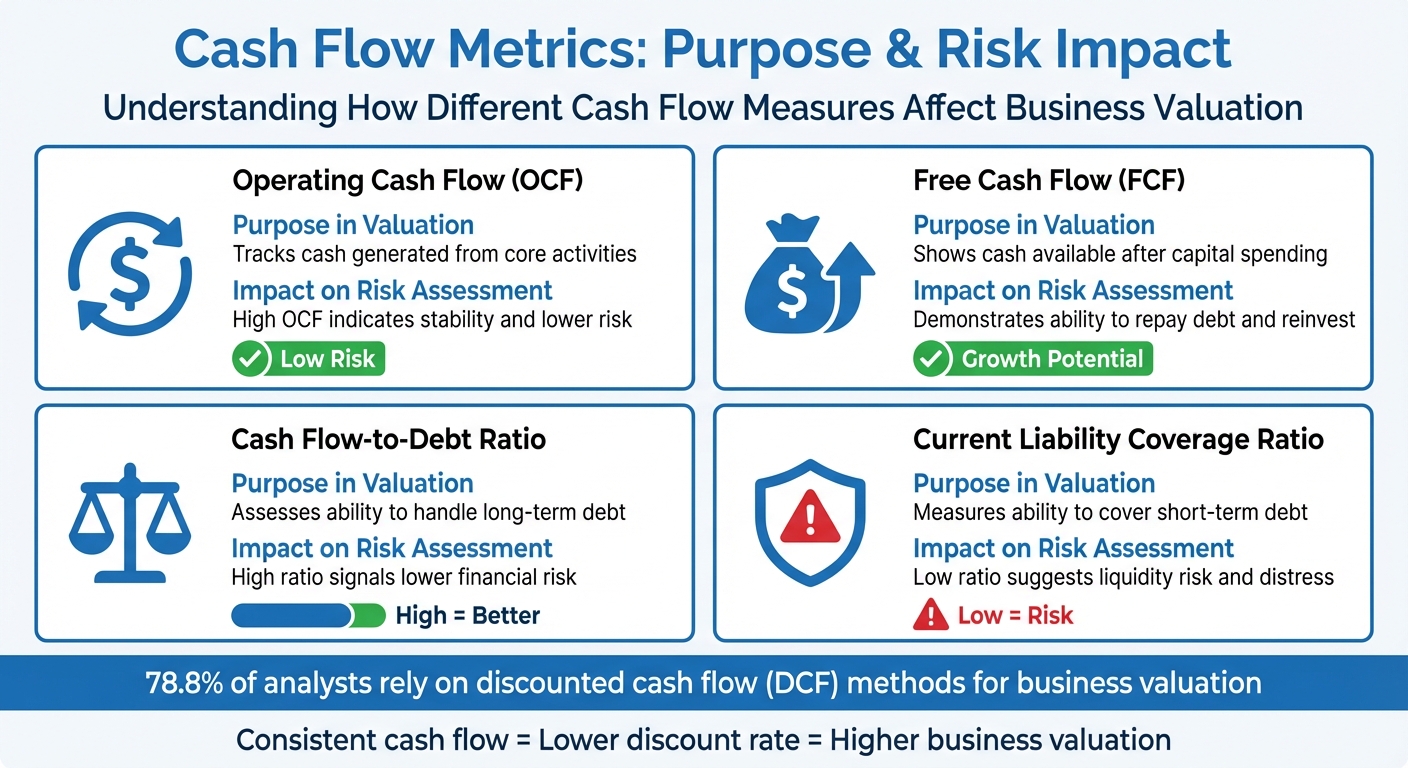

| Metric | Purpose in Valuation | Impact on Risk Assessment |

|---|---|---|

| Operating Cash Flow (OCF) | Tracks cash generated from core activities | High OCF indicates stability and lower risk |

| Free Cash Flow (FCF) | Shows cash available after capital spending | Demonstrates ability to repay debt and reinvest |

| Cash Flow-to-Debt Ratio | Assesses ability to handle long-term debt | High ratio signals lower financial risk |

| Current Liability Coverage Ratio | Measures ability to cover short-term debt | Low ratio suggests liquidity risk and distress |

How Cash Flow is Used in Valuation Models

Cash flow plays a central role in determining a business's value. Valuation models leverage cash flow metrics in different ways, whether through income, market, or asset-based approaches. This is because cash flow is a direct indicator of a company's financial health and its potential for future growth.

The Discounted Cash Flow (DCF) Model

The Discounted Cash Flow (DCF) model is a widely respected method for valuing businesses. It works by projecting a company's future cash flows - typically over a 5–10 year period - and then discounting those cash flows back to their present value. The discount rate accounts for both the time value of money and the risks involved. This method centers on a company's ability to generate cash, avoiding reliance on fleeting market trends or subjective opinions.

"DCF analysis is the best way to arrive at an educated estimate, whether you're assessing the cost of a specific project, purchasing shares of a publicly traded company, or investing in a private business." - Katie O'Leary & Carlos Cervantes, PitchBook

The DCF model operates in two parts. First is the explicit forecast period, where cash flows are estimated based on historical data and growth projections. Second is the terminal value, which represents the business's worth beyond the forecast period. The terminal value often makes up more than half of the total valuation, highlighting the importance of discounting future cash flows.

FCFF vs. FCFE in DCF Calculations

When creating a DCF model, analysts can choose between Free Cash Flow to the Firm (FCFF) and Free Cash Flow to Equity (FCFE).

- FCFF represents the cash available to all capital providers - both debt and equity.

- FCFE focuses on the cash available specifically to equity investors after covering operating expenses, taxes, reinvestments, and debt payments.

FCFF is the preferred choice for companies with complex capital structures because the Weighted Average Cost of Capital (WACC) tends to remain more stable than the cost of equity. In fact, analysts use FCFF about twice as often as FCFE.

| Feature | Free Cash Flow to Firm (FCFF) | Free Cash Flow to Equity (FCFE) |

|---|---|---|

| Definition | Cash available to all investors | Cash available to equity investors |

| Starting Point | Often starts with EBIT or EBITDA | Often starts with Net Income |

| Discount Rate | Weighted Average Cost of Capital (WACC) | Required rate of return on equity |

| Formula (Simplified) | NI + Non-cash Charges + Interest (1–Tax) – CapEx – Working Capital | NI + Non-cash Charges – CapEx – Working Capital + Net Borrowing |

| Primary Use | Valuing the entire enterprise | Valuing the equity stake |

To calculate equity value using FCFF, analysts first determine the total firm value and then subtract the market value of debt. With FCFE, the equity value is calculated directly. FCFF is better suited for businesses with intricate capital structures, while FCFE works well for companies with steady debt levels or when analyzing from a minority shareholder's perspective.

Cash Flow in Market and Asset-Based Valuations

Cash flow also plays a key role in market-based and asset-based valuation methods. While DCF provides an intrinsic valuation based on a company's internal performance, market-based valuation focuses on relative value by comparing similar businesses. Metrics like EV/EBITDA multiples allow investors to benchmark a company's performance against industry standards. For example, nearly 92.8% of professional analysts use market multiples when valuing individual equities.

If a DCF-derived intrinsic value differs significantly from market comparables, it may indicate the need to revisit assumptions about growth and risk. Additionally, industry-specific factors affect multiples - software companies with higher profit margins often command higher multiples than manufacturing firms with lower margins.

Asset-based valuation incorporates cash flow by estimating the market value of a company's assets at the end of the forecast period. This approach is particularly useful for asset-heavy or distressed businesses. For smaller private companies, discounts of 20% to 50% are often applied compared to public company valuations to account for liquidity and risk differences. These valuation techniques set the stage for addressing common cash flow challenges that can impact a business's overall value.

Common Cash Flow Problems That Hurt Valuation

Cash flow problems can take a serious toll on business valuation, signaling instability and operational risks to potential buyers or investors. Research shows that 82% of business failures cite cash flow issues as a primary cause.

One major issue is inventory management. When too much cash is tied up in slow-moving inventory, liquidity takes a hit. Interestingly, 80% of sales typically come from just 20% of inventory. Businesses often fall into the trap of over-diversifying their product offerings, adding items that don’t significantly boost sales. This dilutes profit margins and puts unnecessary strain on working capital. Another red flag is client concentration - relying on a single customer for more than 30% of revenue. This creates a precarious situation where one delayed payment or lost contract can trigger a cash crisis, immediately lowering valuation. These operational risks are major concerns for investors.

"One of the biggest mistakes a company can make is flying blind with their finances. This almost always leads to overspending, under-charging, delinquent accounts, and fatal cash flow issues." - Troy Skabelund, CFO and Systems Expert, Preferred CFO

High fixed costs are another culprit. They drain cash reserves, especially when businesses are forced to offer interest-free credit due to late payments, further tightening liquidity.

Managing Seasonal Cash Flow Changes

Seasonal revenue swings can complicate valuation by making it harder to assess a business’s consistent cash flow. Take a ski resort that earns most of its revenue during the winter or a retail store that thrives during the holidays. Without careful planning, these businesses may appear unstable, even if their models are fundamentally sound.

To navigate these challenges, businesses should build cash reserves during peak seasons to cover slower months. Experts recommend maintaining reserves that can cover at least 3 to 6 months of operating expenses. Rolling 12-month cash flow forecasts can also help identify potential shortfalls early, giving businesses time to adjust spending or ramp up sales. Negotiating extended payment terms with suppliers during off-peak periods can further ease cash flow pressure.

Another strategy is diversifying product lines to smooth out seasonal fluctuations. For example, a landscaping business could add snow removal services in the winter, or a pool maintenance company might offer holiday lighting installation. This approach spreads revenue across the year, reducing dependence on a single season. Additionally, adjusting operational costs - like inventory, staffing, and marketing - based on seasonal trends ensures expenses stay aligned with revenue. These strategies help maintain cash flow stability, which is a key factor in attracting investors.

Debt and Growth Management

Beyond operational cash flow, managing growth and debt is equally critical. Many businesses fall into the "success trap", where rapid expansion requires significant upfront investment. This is why 38% of startups run out of cash during growth phases. High debt levels only add to the problem, as cash gets funneled into interest payments instead of reinvestment, increasing risk and dragging down valuation.

A great example of balanced cash flow management comes from Hannah's Bananas in March 2024. The company generated $35,000 from operating activities, allocating $20,000 to new equipment (growth) and $5,000 to loan repayment, while still achieving a net cash increase of $22,000 for the period. This shows how disciplined planning can support growth without overextending resources.

"Revenue alone doesn't indicate profitability. A business with high revenue but poor cash flow may struggle with expenses or debt." - Bryson Havner, H&H Accounting Services

To avoid overextension, businesses should create detailed capital forecasts for different growth scenarios. Calculating incremental working capital needs - often as a percentage of revenue growth - can highlight how much cash expansion will consume. Flexible staffing models, such as outsourcing or hiring part-time workers, can keep fixed costs low during early growth stages. Focusing on high-return activities that preserve liquidity makes the business more appealing to buyers. Additionally, implementing clear payment terms and requiring deposits for large projects ensures faster cash inflows, keeping funds available for both operations and debt obligations.

| Cash Flow Problem | Impact on Valuation | Identification Sign |

|---|---|---|

| High Debt Levels | Increases risk; limits reinvestment options | High debt-to-equity ratio; significant financing cash outflows |

| Seasonal Fluctuations | Makes forecasting difficult; suggests instability | Erratic month-to-month operating cash flow |

| Rapid Growth | Can lead to overextension and inefficiency | Negative operating cash flow despite revenue growth |

| Inventory Creep | Ties up cash; raises storage costs | High inventory with low turnover rates |

| Client Concentration | Creates dependency risk; threatens stability | Over 30% of revenue from one client |

Using Kumo for Cash Flow Analysis in Business Acquisitions

Accurate cash flow analysis is essential when assessing business acquisitions. It can often be the deciding factor between a successful investment and a costly mistake. Kumo simplifies this process by bringing together business listings from various sources and equipping investors with tools to evaluate financial health before making a commitment. By doing so, it establishes a solid foundation for insights powered by advanced AI.

AI-Powered Cash Flow Insights

Kumo uses advanced algorithms to turn financial data into practical insights, tackling common cash flow challenges head-on. Its Financeability Framework evaluates more than 50 key factors, with a strong emphasis on cash flow modeling and borrower profiles. This framework automatically highlights crucial valuation elements, such as delivery and merchant risk, while keeping loan-to-value (LTV) ratios under 75% to minimize exposure.

"Our indices cover critical aspects such as the cost curve of various carbon credit types, delivery risk, and detailed cash flow analyses, giving investors the insights they need to make informed decisions." - Kumo FAQ

Kumo also automates data aggregation, organizing financial documents into secure, standardized data rooms. This ensures that project-level information is readily accessible and simplifies the due diligence process.

Finding Businesses with Strong Cash Flow Using Kumo

Kumo’s custom search filters and deal alerts make it easier for investors to pinpoint businesses with steady cash flow. Its Project Comparison Tool allows users to benchmark opportunities against industry norms and pre-screened projects, helping identify businesses with reliable financial patterns. After acquisition, Kumo’s Portfolio Management System offers round-the-clock automated monitoring to track financial performance and flag potential issues early on.

Conclusion

Cash flow is a clear indicator of a business's financial health and serves as a cornerstone for accurate valuation. Unlike revenue or profit, which can be shaped by accounting methods, cash flow reveals the actual movement of money within a company - money that’s available to cover expenses, invest in growth, and meet obligations. As Lemuel J. Lim from Genesis Law Firm explains, "DCF valuation is about making predictions concerning how much future free cash the business will generate, and then 'discounting' the future cash flow back into today's money". This underscores the importance of reliable cash flow projections in any valuation model.

For buyers and investors, understanding cash flow patterns is non-negotiable. Even companies that appear profitable on paper can face sustainability issues if their cash flow is inconsistent. In fact, research highlights that 86.9% of professional analysts rely on discounted free cash flow models when valuing equities. This statistic underscores the trust placed in cash flow analysis as a vital tool for assessing a business's worth.

However, diving into detailed cash flow data can be a complex and time-consuming task. This is where advanced tools like Kumo come into play. By automating data collection, providing AI-driven insights, and offering thorough analytics, Kumo simplifies the process. It also enables users to benchmark opportunities against industry standards, making it easier to pinpoint high-value prospects. With such technology, investors can evaluate cash flow's role in business valuation more efficiently, equipping them to make smarter, quicker decisions.

Whether you're analyzing your first acquisition or managing an extensive portfolio, focusing on cash flow analysis is key to better decision-making. Understanding the difference between accounting profits and actual liquidity, spotting businesses with sustainable cash generation, and assessing risks with precision all hinge on a strong grasp of cash flow. Armed with the right tools and a thoughtful approach, you can confidently navigate the complexities of valuation and uncover opportunities that promise lasting rewards.

FAQs

What is the difference between cash flow and net income in business valuation?

Cash flow and net income are two separate financial metrics, each serving a unique purpose in understanding a business's financial health. Cash flow tracks the actual movement of money in and out of a business, covering operations, investments, and financing activities. On the other hand, net income is an accounting figure that subtracts expenses from revenues, often factoring in non-cash items like depreciation and amortization.

Because net income is shaped by accounting policies and timing differences, it doesn’t always represent the cash readily available for reinvestment, paying off debt, or distributing to owners. This is why valuation methods like discounted cash flow (DCF) rely on cash-based metrics - they offer a more accurate measure of a company’s ability to generate returns. If you're considering acquisitions on platforms like Kumo, focusing on operating cash flow can give you a clearer understanding of a company's real value than simply looking at net income.

Why do analysts often use the Discounted Cash Flow (DCF) model for business valuation?

The Discounted Cash Flow (DCF) model is a go-to tool for analysts because it zeroes in on a company's core value by estimating future cash flows and bringing them back to their present value. This method takes the time value of money into account, ensuring future earnings are adjusted to reflect their worth today.

What sets the DCF model apart is its focus on a company's fundamentals rather than short-term market fluctuations. By prioritizing projected cash flow performance, it offers a solid framework for assessing long-term value and provides a clearer understanding of a business's true financial health.

How can businesses effectively manage cash flow during seasonal fluctuations?

Managing seasonal cash flow begins with forecasting. Take a close look at past sales trends to anticipate periods of high and low revenue. This insight helps you plan your cash inflows and outflows more effectively. For instance, you can set aside extra cash during peak months to cover expenses during slower times. It also allows you to schedule larger expenses to coincide with stronger revenue periods.

Another smart move is considering flexible financing options. Tools like revolving lines of credit or short-term loans can provide a safety net for temporary cash shortfalls, helping you avoid more expensive solutions. You might also look into renegotiating payment terms. For example, you could extend payment timelines with suppliers or offer discounts to customers for early payments - both strategies can help stabilize cash flow.

Operational tweaks can make a big difference too. During slower seasons, you might reduce inventory, cut back on discretionary spending, or rely more on part-time or contract workers. On the flip side, during peak periods, consider running promotions or launching new products to stretch your revenue beyond the seasonal spike. These approaches can help create a more balanced cash flow throughout the year.