Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

When you acquire a business, managing tax compliance is one of the most critical steps to ensure a smooth transition and avoid costly penalties. From updating tax registrations to filing required forms, the process involves multiple layers depending on whether it’s a stock or asset purchase. Here's what you need to know:

- Understand the Deal Structure: Stock purchases retain the target's tax attributes, while asset purchases allow for a stepped-up basis for depreciation benefits.

- Federal Tax Filings: File forms like 8594 for asset allocation or 1122 for consolidated returns. Don’t forget employment taxes and short-period returns if applicable.

- State and Local Taxes: Reassess nexus obligations, update registrations, and address sales tax compliance, including collecting new exemption certificates.

- Legacy Tax Risks: Review prior tax filings, audits, and liabilities to identify potential risks or unresolved issues.

- Internal Controls: Set up clear processes, align tax policies, and maintain accurate records to ensure ongoing compliance.

The first 90 days post-acquisition are critical for meeting tax deadlines, reconciling accounts, and addressing inherited liabilities. A detailed checklist can help you stay organized and avoid surprises during this period.

M&A Tax Structuring 101: Asset vs. Stock Purchases, QSBS, and F-Reorgs Explained with Josh Siegel

Understanding the Acquisition Structure and Tax Implications

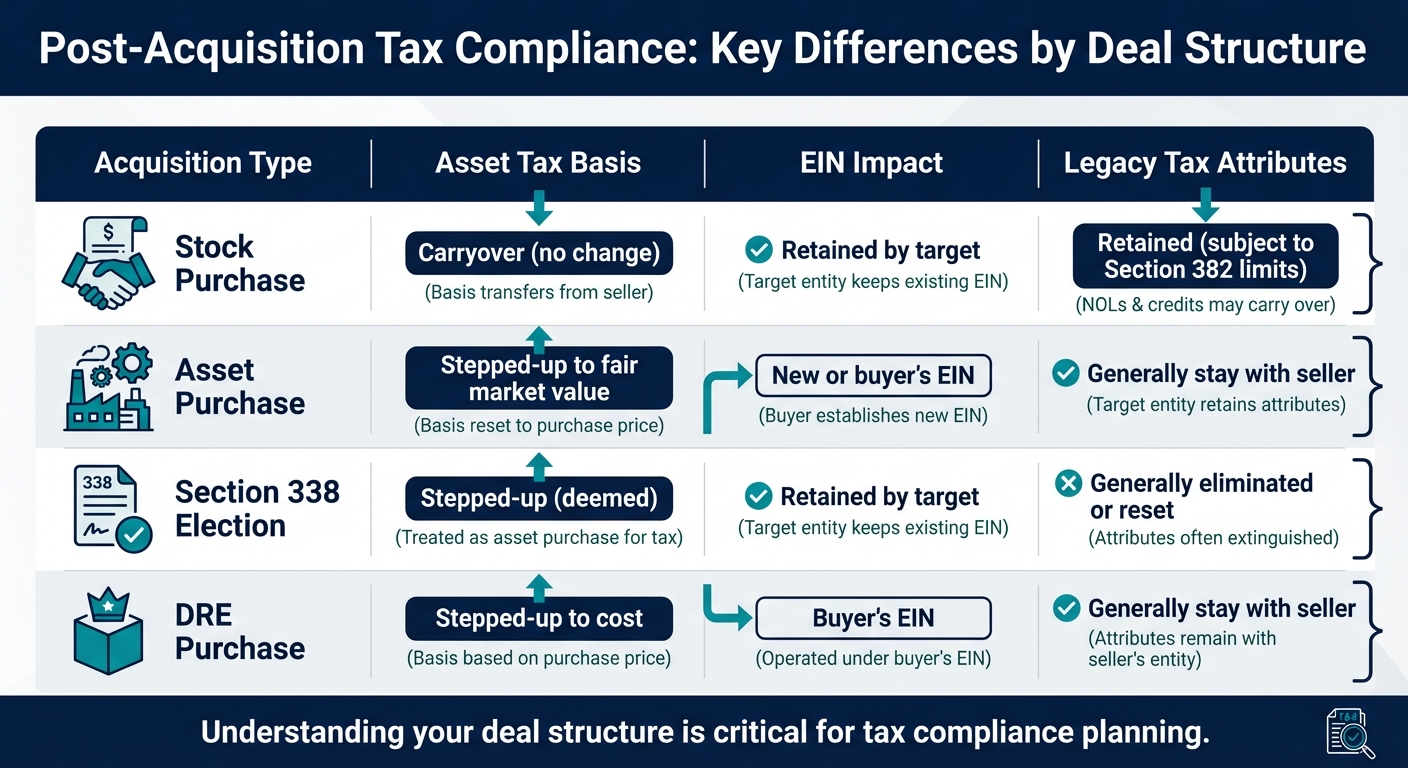

Post-Acquisition Tax Compliance: Key Differences by Deal Structure

Confirming the Acquisition Structure

When navigating post-acquisition tax compliance, the first priority is confirming the acquisition structure. This decision shapes your entire compliance process. For instance, in a taxable stock acquisition, the cost basis of the acquired stock equals the purchase price, while the target corporation's assets and liabilities retain their existing tax basis without adjustment. On the other hand, a taxable asset acquisition allows for a stepped-up cost basis on the assets, matching the purchase price, which can lead to future tax benefits through depreciation or amortization deductions.

A Section 338 election offers a unique scenario: although the transaction is legally a stock purchase, it is treated as an asset purchase for tax purposes if a corporate buyer acquires at least 80% of the target's stock by vote and value. Similarly, in a disregarded entity (DRE) purchase, acquiring 100% of the DRE is treated as a direct asset purchase for federal tax purposes, even if the legal form is an equity transfer. To ensure accuracy, review the purchase agreement and consult your tax advisor to confirm the structure.

Employer Identification Number (EIN) and Tax Classification

Your EIN obligations hinge on the acquisition structure. In a stock purchase, the target keeps its EIN, along with its tax attributes and historical basis. In an asset purchase, however, income is reported using the buyer's EIN, or a newly established one. To verify an existing EIN, check the original IRS notice, licenses, bank accounts, or past tax filings. If you need to update the responsible party, file Form 8822-B. Keep in mind, the IRS limits EIN applications to one per responsible party per day. While online applications are processed instantly, fax submissions take about four business days. Correct EIN classification is vital for ensuring compliance with federal and state tax filing requirements.

Reviewing Tax Responsibilities in the Purchase Agreement

The purchase agreement serves as your legal guide for dividing tax responsibilities between the buyer and seller. Pay close attention to tax covenants and indemnity clauses, especially for the straddle period, which spans the closing date. According to Weil, Gotshal & Manges:

Under a typical tax indemnity, the seller agrees to indemnify the buyer for certain taxes of the target corporation that arise after closing but are attributable to any pre-closing tax periods.

Additionally, the agreement should outline how the purchase price is allocated across asset categories such as inventory, equipment, and goodwill. This allocation, often determined using the "residual method", establishes the basis for future depreciation and amortization. If the target company has Net Operating Losses (NOLs), review clauses related to Section 382 limitations. These limitations may apply if certain large shareholders increase their ownership by more than 50 percentage points within a three-year testing period. As of August 2024, the published rate for calculating the annual limitation on tax attributes was 3.62%. These details are critical for addressing both federal and local tax compliance requirements.

| Acquisition Type | Asset Tax Basis | EIN Impact | Legacy Tax Attributes |

|---|---|---|---|

| Stock Purchase | Carryover (no change) | Retained by target | Retained (subject to Section 382 limits) |

| Asset Purchase | Stepped-up to fair market value | New or buyer's EIN | Generally stay with seller |

| Section 338 Election | Stepped-up (deemed) | Retained by target | Generally eliminated or reset |

| DRE Purchase | Stepped-up to cost | Buyer's EIN | Generally stay with seller |

Federal Tax Compliance Steps

Federal Income Tax Filing Requirements

After the acquisition closes, you’ll need to determine if a short-period return is required. This applies when the entity operates for less than 12 months or its accounting period changes due to the acquisition. If the acquired business is dissolved or undergoes a major structural change, you must file a final return. Be sure to check the "final return" box on the appropriate tax forms - Forms 1040, 1065, 1120, or 1120-S. For partnerships and S corporations, also mark the "final K-1" box on Schedule K-1 to wrap up tax obligations.

When it comes to allocating the purchase price, use Form 8594 and follow the residual method. Both parties must ensure their filings align to avoid drawing attention from the IRS. If the acquired corporation is liquidated, Form 966 (Corporate Dissolution or Liquidation) must be filed within 30 days of adopting the dissolution plan. Once all returns are filed and taxes are paid, send a letter to the IRS to cancel the entity's EIN and close the business account.

After handling income tax filings, shift your focus to employment and payroll tax compliance.

Employment and Payroll Tax Compliance

For employment taxes, file final Forms 941 or 944 and Form 940 as needed. Mark the "final return" box and include the date the last wages were paid. Specifically for FUTA tax, check box "d" on Form 940. W-2s must be issued to employees by the final filing deadline, and employment tax records should be kept for at least four years.

Make all tax deposits through the Electronic Federal Tax Payment System (EFTPS). If you’re e-filing employment tax returns, you’ll need a 94x On-line Signature PIN, which can take up to 45 days to process. The IRS typically acknowledges e-filed employment tax returns within 24 hours.

Once employment and payroll tax matters are settled, address your information reporting obligations.

Information Reporting Obligations

Starting January 1, 2024, businesses filing 10 or more information returns in a calendar year must file electronically. This threshold includes nearly all information return types, such as W-2s and the 1099 series. To avoid backup withholding, use Form W-9 to collect Taxpayer Identification Numbers (TINs) from new vendors and attorneys after the acquisition.

Form 1099-NEC is required for reporting payments of $600 or more to independent contractors, attorney fees, and excess golden parachute payments. The deadline for filing is January 31. Form 1099-MISC, on the other hand, is used for reporting rents ($600+), royalties ($10+), medical payments, and legal settlements. Paper filings for Form 1099-MISC are due by February 28, while electronic filings are due by March 31. If an employee passes away during the acquisition year, report any wages paid to their estate or beneficiary on Form 1099-MISC (Box 3).

For a no-cost option to file 1099 series forms electronically, you can use the IRS Information Returns Intake System (IRIS), which also simplifies the process for filing extensions.

| Form Type | Purpose in Post-Acquisition Compliance | Due Date (to IRS) |

|---|---|---|

| Form 8594 | Asset Acquisition Statement | With income tax return |

| Form 966 | Corporate Dissolution | Within 30 days of plan adoption |

| Form 941/944 | Employment Tax Return (Final) | Quarterly or annually |

| Form 940 | FUTA Tax Return (Final) | January 31 |

| Form 1099-NEC | Nonemployee compensation and attorney fees | January 31 |

| Form 1099-MISC | Rents, royalties, legal settlements, and more | February 28 (Paper) / March 31 (E-file) |

State and Local Tax Compliance

Mapping Nexus and Registration Updates

After an acquisition, it's crucial to reassess state tax obligations. Start with a detailed nexus analysis for both the acquiring and target businesses. This involves examining physical presence factors - like employees, inventory, and property - as well as economic thresholds, such as sales volume or transaction counts. While many states set their economic nexus threshold at $100,000 in sales or 200 transactions, some states, like California, raise the bar to $500,000.

The structure of the acquisition significantly impacts tax compliance. If the target company is merged into your existing legal entity (common in asset deals), you'll need to evaluate the combined footprint of both businesses. On the other hand, if the target remains a separate entity (typical in stock deals), check for any "affiliate nexus." This occurs when shared resources - like facilities, employees, or product lines - create new tax obligations.

"When a business reorganization changes the structure of the business, a new registration is generally required." – Sales Tax Institute

To avoid inheriting the seller’s unpaid tax liabilities, request tax clearance certificates before the deal closes. For example, in Texas, you can file Form 86-114 to obtain a Certificate of No Tax Due. While this certificate is usually issued within 10 business days, it could take up to 90 days if the state opts to audit the seller’s records. This step protects you from being responsible for unpaid taxes, interest, and penalties. Additionally, if the entity is dissolved or merged, file "gap" returns (zero-dollar returns) until the state officially closes the account, avoiding delinquency notices.

Once nexus determinations are updated, align them with state income and franchise tax filing requirements.

State Income and Franchise Tax Filings

Using the updated nexus analysis, adjust your state income and franchise tax filings to reflect the new business structure. For entities operating less than 12 months post-acquisition, file short-period returns. If you’re dissolving the target company, make sure to submit final state income and franchise tax returns. Keep in mind that merging businesses can shift income apportionment across states, especially in areas where you previously had no presence.

Work closely with your legal and payroll teams to prevent overlapping state registrations or duplicate filings. The growing trend of remote work adds complexity here - even a single employee working from home in a different state can trigger new filing requirements.

Once income tax filings are addressed, turn your attention to sales and use tax compliance.

Sales and Use Tax Obligations

Sales tax compliance is another critical area to review. Start by examining the target company’s historical sales tax practices during due diligence. If you find any compliance gaps, consider entering into a Voluntary Disclosure Agreement (VDA). This can limit the look-back period to three or four years and may waive penalties. However, be aware that interest on delinquent sales tax typically averages 12% per year, and penalties can climb as high as 25% of the tax due. The consequences are particularly severe if taxes were collected but not remitted.

Don’t forget to update customer exemption certificates. In asset acquisitions, certificates issued under the previous ownership don’t automatically transfer to the new owner, so it’s essential to collect new ones. Some states, like Florida, even require annual updates to these certificates. Establish clear processes for collecting and remitting sales tax, and ensure your business is registered in every state where the combined entity now has nexus - whether that’s based on physical presence or economic thresholds.

| Nexus Type | Common Triggers | Post-Acquisition Action |

|---|---|---|

| Physical | Employees, inventory, property | Update registrations for new locations |

| Economic | $100,000+ in sales or 200+ transactions | Monitor combined revenue of both entities |

| Affiliate | Related entities promoting in-state | Review ties between buyer and target |

sbb-itb-97ecd51

Tax Accounting and Financial Integration

Aligning Tax Accounting Policies

After ensuring compliance with federal and state tax filing requirements, the next step is to integrate tax accounting processes for accurate financial reporting. From the acquisition date, align the target company's tax accounting policies with your own. According to ASC 805-20-25-6, classify acquired assets and assumed liabilities based on your accounting policies at the acquisition date. This includes adjusting the target’s financials to match your revenue recognition and depreciation methods.

If tax effects are central to deal negotiations, record them on Day 1. Otherwise, address them on Day 2. For example, if the acquisition involves a shift from S-Corp to C-Corp status, you must recognize deferred tax assets and liabilities for all temporary differences existing on the acquisition date. Similarly, if the combined entity files a consolidated tax return, deferred taxes should be measured using enacted tax rates. This becomes especially relevant when expanding your state tax footprint. For instance, acquiring a business in California while headquartered in Nevada may introduce new state deferred tax requirements. These changes should be recorded as income tax expense rather than being included in acquisition accounting.

"At the acquisition date, the acquirer shall classify or designate the identifiable assets acquired and liabilities assumed as necessary to subsequently apply other GAAP. The acquirer shall make those classifications or designations on the basis of the contractual terms, economic conditions, its operating or accounting policies, and other pertinent conditions as they exist at the acquisition date." – ASC 805-20-25-6

Once tax accounting policies are aligned, the focus shifts to reconciling tax accounts after the deal closes.

Reconciling Tax Accounts Post-Close

Start by creating an opening balance sheet using purchase accounting, and take advantage of the one-year measurement period to make retrospective adjustments as new information comes to light.

Pay close attention to swing accounts, such as bad debt reserves or unpaid compensation, which may not meet the tax all-events test. In stock acquisitions, while the target’s balance sheet is adjusted to fair value for GAAP purposes, the tax basis remains on a carryover basis. This creates a permanent difference in "inside basis", particularly for fixed assets and intangible assets, which must be carefully tracked. Use financial systems to monitor the gap between fair value (GAAP) and the historical tax basis.

Review the target’s financial statements for any "blackout" periods - times when income or balance sheet activity leading up to the close may be excluded. These periods could include events relevant to transaction tax filings. Reconcile and settle all inter-company accounts, then consolidate them into a unified cash management platform to simplify ongoing operations.

Once tax accounts are reconciled, the next priority is to establish strong internal controls to ensure future compliance.

Establishing Internal Controls and Documentation

On Day 1, set up clear reporting lines and an escalation process to maintain accurate financial data flow. Develop a roles and responsibilities matrix for the newly combined finance team to address redundancies and assign tax-related tasks effectively.

Work with your IT team to create a one-year Sarbanes-Oxley (SOX) integration plan for finance and tax functions. This plan should include interim process controls and align the accounting close process and calendar between the two companies to ensure timely tax filings. Maintain a centralized calendar to track all federal, state, and local tax deadlines. Document Phase 1 reporting activities, organizational changes, and new processes in your corporate archives.

Centralize all documentation related to pending tax matters, such as active audits, extensions, and waivers of statutes of limitations. Confirm that all legacy taxes - including payroll, withholding, sales, use, franchise, and real/personal property taxes - are fully paid through the closing date. Prepare detailed schedules for financial statement footnotes, particularly for goodwill adjustments, to create a clear audit trail. This will help your team address inquiries from tax authorities and maintain compliance in the years ahead.

Monitoring Legacy Tax Liabilities and Risks

Identifying and Managing Legacy Liabilities

After completing an acquisition, it’s crucial to assess any tax risks you’ve inherited. Start by requesting copies of all federal, state, local, and foreign tax returns for at least the past five years. These documents can help you spot compliance patterns - or uncover potential non-compliance issues. Did you know that 47% of M&A deals fail because of problems discovered during due diligence? A significant portion of these failures stems from undetected tax liabilities.

Take a close look at past audit reports, examination notices, settlements, and correspondence with the IRS or state tax authorities. These records may highlight unresolved disputes or recurring issues that could become your responsibility. Pay special attention to uncertain tax positions listed on the target company’s balance sheet. These reserves are often set aside for liabilities that could come back to haunt you after the deal closes.

"Analyzing government audits uncovers compliance issues and future liabilities." - Jack Nicholaisen, Founder, Businessinitiative.org

If your deal involves equity, be prepared for the possibility that all tax risks transfer to you. Even in asset purchases, certain liabilities - like unpaid payroll taxes or sales/use taxes - can follow the business. To protect yourself, cross-check these liabilities with the indemnification rights and tax responsibility clauses in your purchase agreement. This step will clarify your financial recourse and help you prepare for any surprises.

Ongoing Tax Compliance Monitoring

Once you’ve identified legacy liabilities, the next step is to stay on top of them. Implement a system to track these risks and ensure compliance moving forward. A simple but critical task: file IRS Form 8822-B within 60 days of the acquisition. This updates the responsible party on record, ensuring your team receives all future tax correspondence.

"Changes in responsible parties must be reported to the IRS within 60 days." - Internal Revenue Service

Set up periodic reviews to monitor changes in state and local tax obligations where the business operates. Keep an eye on key metrics like the frequency of tax notices, the status of pending audits, and how inherited tax credits are being used. If the acquired company has net operating losses (NOLs) or tax credits, make sure to track any limitations on their use under Section 382 post-acquisition.

It’s also worth evaluating how the previous owner handled tax notices in the past. Were disputes resolved effectively, or were they ignored? A history of poor management could signal ongoing risks. By staying proactive, you can ensure that legacy tax issues don’t disrupt the business’s future compliance or financial health.

Using Kumo for Tax Compliance Planning

Centralizing Tax Risk Data Across Deals

Kumo simplifies the process of tracking tax risks by gathering data from over 120,000 active deals sourced from thousands of brokers and marketplaces, all into one centralized platform. This allows you to keep an eye on more than $26 billion in listings. Its deduplication feature eliminates duplicate listings, ensuring you focus only on unique tax obligations. Plus, advanced search filters let you zero in on targets based on structural elements - like asset versus stock sales - that directly impact your post-acquisition tax compliance strategy.

"Kumo aggregates hundreds of thousands of deals into one easy-to-use platform so that you can spend less time sourcing, and more time closing deals." - Kumo

This consolidated view lays the groundwork for streamlined and consistent compliance processes.

Maintaining Consistent Compliance Workflows

With centralized data management as its foundation, Kumo also ensures consistency during tax due diligence across your acquisitions. Automated daily email alerts notify you when new deals align with your specific criteria, including jurisdictional factors critical for state and local tax nexus planning. With over 700 unique deals added to the platform every day, these alerts save you from constant manual monitoring.

Additionally, Kumo provides curated educational resources that spotlight common mistakes on corporate tax returns during the due diligence phase. By leveraging these tools, you can standardize your early-stage due diligence process, effectively filter out high-risk tax profiles, and ensure every acquisition is scrutinized with the same level of care from the outset.

Conclusion

The first 90 days after closing are a make-or-break period for managing deadlines, aligning tax elections with your acquisition structure, and putting controls in place to avoid financial headaches. Kim Pace from LBMC emphasizes the importance of this window, stating, "The tax situation of the acquisition also needs to be assessed, agreed upon and locked down in this 90-day period". Neglecting this process could lead to serious consequences, like inheriting unpaid liabilities, triggering IRS audits, or losing tax benefits such as net operating losses. Bringing in your tax team early - ideally during due diligence - helps you navigate transaction costs and meet critical deadlines before finalizing the deal.

"Without tax involvement in the M&A integration program, sooner or later a post-integration tax mine will likely be tripped." - Deloitte

To stay on track, you need a clear, actionable strategy. A comprehensive checklist can help maintain accountability. Assigning a tax project manager is key - they'll oversee filings, keep an eye on legacy liabilities, and ensure regulatory deadlines are met. Don’t overlook practical steps like canceling outdated credit lines, reviewing payroll records for redundant roles, and conducting nexus reviews to identify new state and local tax obligations.

FAQs

What are the main tax compliance differences between stock and asset acquisitions?

In a stock acquisition, the buyer takes ownership of the target company’s equity, which means they acquire not just the company’s assets but also its liabilities and tax attributes. Tax compliance in this scenario often involves decisions like making a Section 338 (or 338(h)(10)) election if the buyer wants a step-up in basis for tax purposes. Without this election, the assets retain their original tax basis. Buyers also need to consider factors such as the treatment of goodwill, the use of net operating loss (NOL) carryovers, and any restrictions under Section 382.

On the other hand, an asset acquisition allows the buyer to pick and choose specific assets - such as equipment, real estate, or intellectual property - while generally avoiding unwanted liabilities. In this type of deal, the purchase price is allocated across the acquired assets, resulting in a step-up in tax basis. This step-up impacts future depreciation and amortization deductions. Both the buyer and the seller are required to file IRS Form 8594 to report the allocation of the purchase price. Other compliance steps might include reviewing sales tax obligations for transferred inventory and properly managing any assumed liabilities. These allocation and filing requirements highlight the primary tax differences between stock and asset acquisitions.

What is a Section 338 election, and how does it affect post-acquisition tax compliance?

A Section 338 election lets the buyer of a business treat the purchase as though the target company sold all its assets at fair market value on the date of acquisition. This approach gives the buyer a "stepped-up basis" in the assets, which can lead to future tax perks like depreciation and amortization deductions. However, for the seller, it triggers an immediate taxable gain because of the deemed asset sale.

While this election can be beneficial for the buyer in the long run, it requires careful planning to address the seller's tax burden and to meet IRS filing rules. It's crucial to work with a tax professional to handle the complexities and understand how this election could affect your post-acquisition responsibilities.

What are the key steps for managing state and local tax compliance after acquiring a business?

To stay on top of state and local tax compliance after an acquisition, start by pinpointing where the newly acquired business has a tax nexus. Carefully review the acquired company’s existing tax registrations to see if you need additional state tax IDs, sales tax permits, or payroll tax accounts for any new jurisdictions. It’s also crucial to examine the target company’s past filings for any unpaid balances, pending audits, or returns that might require amendments - issues like these can result in successor liability.

Once that’s done, update your tax calendar to reflect filing deadlines for all relevant taxes, including income, sales, franchise, and property taxes. Make sure to factor in any recent state law changes, such as updated tax rates or new reporting rules, that could impact the business. Don’t overlook payroll systems - ensure they’re updated to comply with revised withholding and unemployment tax requirements. Lastly, maintain detailed records of all registrations and filings, as they’ll be essential for future audits.

By addressing these steps early, you can reduce compliance risks and smoothly integrate the tax responsibilities of the acquired business.