Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

Earnouts are a common feature in M&A agreements, where part of the purchase price is contingent on the acquired business meeting specific performance targets. While they can bridge valuation gaps, they often lead to disputes. To draft enforceable earnout clauses, focus on:

- Clear Metrics: Use measurable, time-bound targets like revenue or EBITDA. Define terms precisely to prevent misinterpretation.

- Payment Terms: Specify payment schedules, methods, and deadlines. Include provisions for late payments and interest.

- Operating Rules: Establish buyer obligations post-closing to protect earnout goals, such as resource allocation or maintaining separate financials.

- Accounting Standards: Detail how metrics will be calculated, avoiding reliance on generic GAAP references.

- Dispute Resolution: Use independent accounting firms for technical disputes and arbitration for legal issues.

- Risk Mitigation: Include security measures like escrow accounts or parent guarantees to ensure payment.

Setting Clear and Measurable Performance Metrics

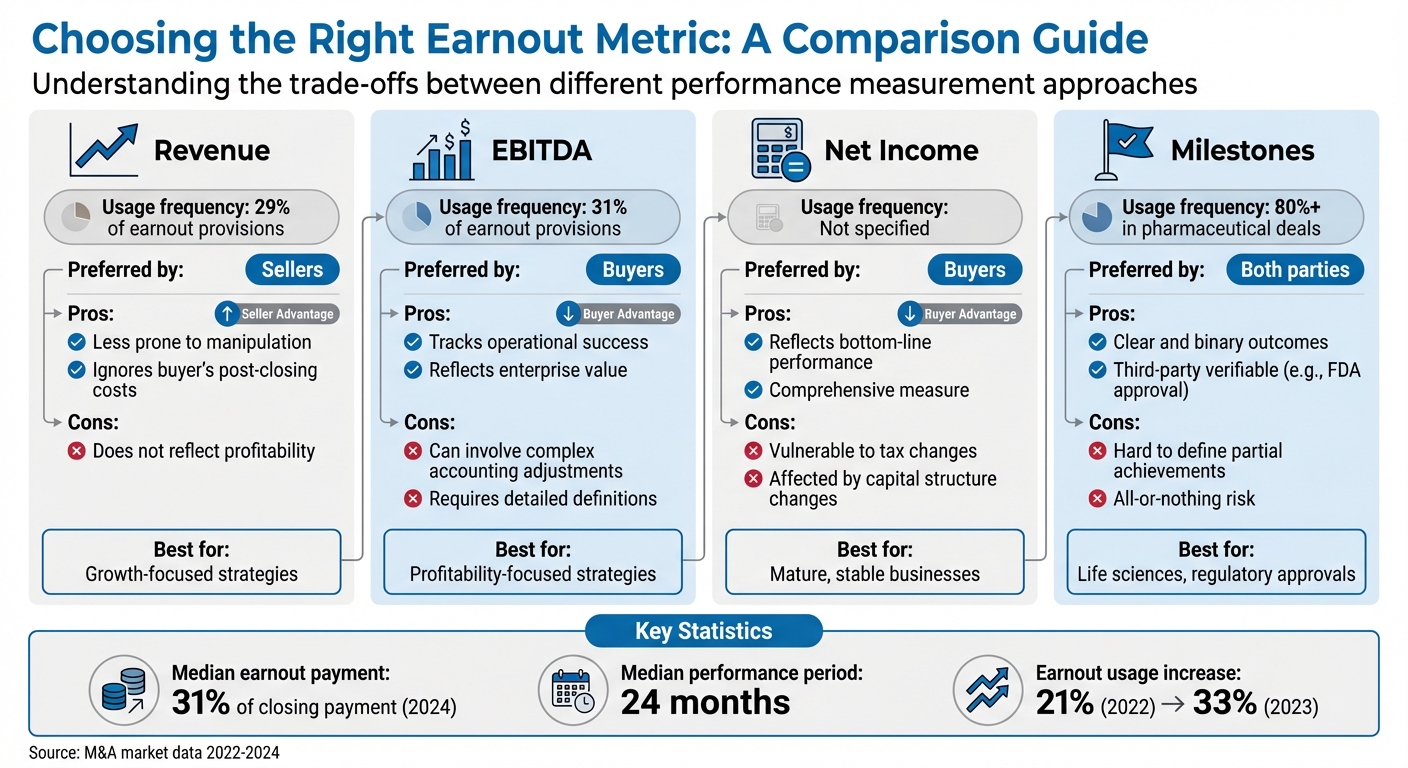

Earnout Performance Metrics Comparison: Revenue vs EBITDA vs Net Income vs Milestones

The foundation of an enforceable earnout lies in clearly defining what success looks like. Ambiguity in metrics can lead to disputes and even litigation. A notable example is the April 2022 case of Schneider Natl. Carriers, Inc. v. Kuntz. The disagreement revolved around a metric requiring the buyer to purchase "60 tractors" annually. The seller interpreted this as an expansion of the fleet by 60 units, while the buyer claimed it simply meant acquiring 60 tractors, regardless of fleet growth. After reviewing 300 exhibits of negotiation history, the court ruled in favor of the seller, resulting in a $40 million earnout payment. This case highlights how even seemingly straightforward metrics can become contentious without precise language.

What Makes a Good Performance Metric

The best performance metrics are those that are objective, measurable, and time-bound. Financial metrics like revenue, EBITDA, gross profit, or net income are frequently used. For instance, EBITDA appears in 31% of earnout provisions, while revenue is used in 29%. Non-financial milestones, such as FDA approvals, patent grants, or product launches, are also effective - particularly in the life sciences sector, where earnouts are part of over 80% of private pharmaceutical deals. Metrics like customer retention rates or regulatory certifications are also relevant in other industries.

The choice of metric should align with the buyer’s post-closing strategy. If the buyer plans to focus on growth at the expense of short-term profitability, revenue-based targets may be more appropriate than EBITDA. Sellers, on the other hand, often prefer revenue metrics because they are less susceptible to manipulation through post-closing expense allocations.

| Metric Type | Preferred by | Pros | Cons |

|---|---|---|---|

| Revenue | Seller | Less prone to manipulation; ignores buyer’s post-closing costs | Does not reflect profitability |

| EBITDA | Buyer | Tracks operational success and enterprise value | Can involve complex accounting adjustments |

| Net Income | Buyer | Reflects bottom-line performance | Vulnerable to tax and capital structure changes |

| Milestones | Both | Clear and binary (e.g., FDA approval) | Hard to define partial achievements |

How to Set Achievable Targets

Achievable targets require thorough planning and scenario analysis. Run sensitivity tests to account for potential risks, such as losing a major customer or supply chain disruptions. Using cumulative measurement periods (e.g., over three years) instead of annual periods can help smooth out volatility, making targets more attainable during market fluctuations. Sellers typically favor cumulative targets because strong performance in one year can offset weaker results in another, whereas buyers may prefer annual targets to ensure consistent performance.

When setting targets, it’s essential to define terms like "Adjusted EBITDA" by detailing permitted add-backs for non-recurring items, transaction costs, litigation settlements, and extraordinary events. This ensures the metric reflects the core performance of the business. For reference, the median earnout payment outside the life sciences sector in 2024 was 31% of the closing payment, with a median performance period of 24 months. These benchmarks can serve as a starting point for negotiations. Lastly, refine the language in your agreements to eliminate any ambiguity in how metrics are calculated.

Writing Metrics with Precise Language

Simply referencing generic GAAP standards isn’t enough, as GAAP allows for multiple interpretations. As Prof. Chad D. Cummings, CPA and attorney, explains:

"The most pervasive misconception is that referencing a common metric, such as EBITDA, makes an earn-out objective and dispute-free. In reality, EBITDA is a bundle of judgments."

To avoid disputes, include a detailed accounting schedule that specifies revenue recognition, reserve methodologies, and inventory valuation. Consider adding an EBITDA model as an illustrative calculation to clarify how the formula should be applied. Also, define the "earnout business" explicitly by identifying specific products, SKUs, or customer accounts to ensure the metrics apply only to the legacy business.

For example, in December 2022, the Delaware Superior Court ruled in Fortis Advisors v. Dematic Corporation over a dispute about the definition of "Company Products." The buyer had integrated the acquired products into its existing lines and excluded those sales from the earnout calculation. The court sided with the seller, ruling that the metric should include sales of integrated products that used the acquired software’s source code, resulting in a multimillion-dollar judgment. To avoid such conflicts, clearly state whether the metric applies only to the legacy business or extends to expanded operations.

Structuring Payment Terms and Schedules

After defining what success looks like, the next step is to lay out how and when the earnout will be paid. Clear payment terms are essential to avoid disputes, as payment mechanics are often a source of contention. Typically, earnout periods span one to three years. Payments can be structured as a single lump sum or divided into multiple installments, often paid annually or quarterly.

Payment Timing and Methods

It’s important to specify the payment timeline. For example, you might require the buyer to deliver the earnout statement within 60 days after the measurement period ends, with payment due within 10 days after that. This level of precision eliminates ambiguity and sets enforceable deadlines.

Cash is the most common payment method, but earnout agreements can also include buyer equity or promissory notes. For cash payments, the agreement should specify the currency (e.g., U.S. dollars) and include detailed wire transfer instructions. If the earnout uses a tiered structure - where different performance outcomes trigger varying payments - attach a clear "waterfall" schedule with examples to show how the formula works.

Sellers often prefer cumulative measurement periods (e.g., total revenue over three years), as strong performance in one period can make up for weaker results in another. Buyers, on the other hand, typically favor discrete annual periods to ensure consistent performance every year.

It's also wise to define acceleration triggers that require immediate payment of the remaining earnout. Common triggers include a change of control, the sale of the acquired business, buyer bankruptcy or insolvency, or the termination of key employees without cause. Interestingly, fewer than half of private acquisition agreements automatically accelerate earnouts in the event of a change of control, so sellers should negotiate for this protection explicitly.

Next, let’s dive into the specifics of equity-based earnouts.

Handling Equity-Based Earnouts

Equity-based earnouts come with their own set of challenges. First, determine how the equity will be valued. Will it have a fixed price per share at closing, or will the price float based on market conditions at the time of issuance? Fixed-share earnouts are usually classified as equity for accounting purposes, while variable-share earnouts may be treated as liabilities, requiring periodic fair-value adjustments.

Sellers receiving equity should negotiate liquidity protections. These might include registration rights if the buyer is a public company, clear vesting schedules, and specific transfer restrictions. It’s also important to include dilution protections to ensure that future share issuances don’t unfairly reduce your equity stake.

Tax considerations are crucial as well. If earnout payments are tied solely to employment milestones, they could be reclassified as compensation rather than part of the purchase price. To maintain favorable tax treatment, document the commercial rationale for the earnout, separate from any employment conditions.

Late Payment and Interest Provisions

To protect against late payments, include an interest penalty clause. For instance, you could specify an interest rate like the prime rate plus 2% or a fixed 8% per year, with interest accruing immediately after the payment deadline.

To reduce credit risk, negotiate payment security measures. Options include escrow accounts, standby letters of credit, parent guarantees, or security interests. Each option has trade-offs: escrow accounts offer high security but tie up the buyer’s capital, while parent guarantees depend on the parent company’s creditworthiness.

Watch out for set-off rights, which allow buyers to withhold earnout payments to cover unresolved indemnity claims or purchase price adjustments. You can limit these rights by requiring that losses be "finally determined" through arbitration or a court ruling before funds are withheld.

Finally, consider adding a buyout option. This would allow the buyer to settle all future earnout obligations with a one-time acceleration payment, often calculated as the net present value of the remaining payments. Such a provision gives the buyer operational flexibility while providing the seller with immediate liquidity and certainty. Together with clear performance metrics and payment schedules, these measures help create enforceable and practical earnout agreements.

Setting Post-Closing Operating Rules

After finalizing payment terms, it's crucial to establish clear post-closing operating rules for the buyer. Without these, buyers may unintentionally - or sometimes intentionally - make decisions that jeopardize earnout goals. This isn't just speculation; earnout-related lawsuits in the Delaware Court of Chancery surged fourfold in the first quarter of 2023 compared to the same period in 2022.

The challenge lies in finding a middle ground. Sellers want assurance that the buyer will strive to meet earnout milestones, while buyers need flexibility to adapt the acquired business to changing circumstances. By drafting precise operating covenants, you can reduce ambiguity, protect earnout targets, and ensure enforceable agreements.

Defining Buyer Conduct Standards

One of the most contentious provisions in earnout agreements is the "efforts" clause, which outlines the buyer's responsibility to achieve earnout goals. Vague terms like "commercially reasonable efforts" often lead to disputes because they can be interpreted in multiple ways. To avoid this, use a clear contractual framework that explicitly defines the buyer's obligations.

There are two main approaches to setting these standards:

- Inward-facing standards: These compare the buyer's efforts to its own historical practices. For instance, the buyer might commit to supporting the acquired product line with the same level of marketing or sales investment as its top-performing products. This method is generally more favorable to buyers.

- Outward-facing standards: These measure the buyer's actions against the norms of similar companies in the industry. For example, the agreement might require the buyer to allocate resources consistent with what other biopharmaceutical companies would typically do. This approach offers sellers more protection but can introduce some uncertainty.

A notable case is SRS v. Alexion Pharmaceuticals (September 2024). Alexion acquired Syntimmune for $400 million upfront and $800 million in potential earnouts. The agreement used an outward-facing standard to define "commercially reasonable efforts." After Alexion was acquired by AstraZeneca and halted development of a key drug, the Delaware Court of Chancery ruled that a comparable company would have continued development, leading to a breach of the efforts clause.

In addition to defining "efforts", operational covenants can further limit the buyer's discretion. Common examples include:

- Running the business in line with prior practices or an approved plan.

- Keeping the acquired business as a standalone division with separate financial records.

- Maintaining minimum levels of working capital or staff.

- Restricting asset sales or new debt beyond agreed limits.

Negative covenants - prohibiting actions that could intentionally reduce earnout payments - are also essential. However, these alone aren't enough. Delaware courts have clarified that the implied covenant of good faith and fair dealing acts as a gap-filler, not a substitute for explicit terms granting the buyer discretion.

Permitted Changes and Force Majeure

While strict covenants protect earnout goals, buyers still need flexibility to handle unexpected events. Start by outlining specific actions the buyer can take without violating the earnout agreement. For example, the contract might allow the buyer to:

- Integrate the acquired product into existing lines, with clear rules on crediting integrated sales.

- Align accounting policies with its established GAAP-compliant practices.

- Adjust pricing or product offerings in response to market pressures.

- Close facilities or consolidate operations for legitimate reasons.

By listing these permitted actions explicitly, you reduce the risk of them being misinterpreted as attempts to undermine the earnout.

It's also wise to include a force majeure clause to address extraordinary events that could disrupt earnout targets. Clearly define events like:

- Natural disasters (e.g., hurricanes, earthquakes)

- Pandemics or government-mandated shutdowns

- Labor strikes or disputes

- Significant safety or efficacy concerns for regulated products

- The emergence of a competing product

The clause should specify whether such events pause (or "toll") the earnout period or allow it to expire as scheduled. Additionally, clarify how force majeure impacts the buyer's obligations - such as whether they must still make reasonable efforts to mitigate the event's effects.

A case worth noting is S'holder Representative Servs. LLC v. Shire US Holdings, Inc. (October 2020). Here, a $45 million earnout hinged on a clinical trial. The agreement included a clause nullifying the payment if material safety or efficacy issues arose. The court ultimately required the buyer to prove that these concerns justified missing the milestone.

Approval and Consent Requirements

Specific approval and consent rights can further safeguard earnout outcomes. Sellers may negotiate veto rights over certain high-impact decisions, but these should be narrowly defined to avoid giving sellers excessive control over daily operations. Common areas where sellers might seek approval include:

- Terminating key employees without cause.

- Modifying clinical trial protocols or regulatory plans.

- Diverting focus away from the acquired product line.

- Selling or licensing critical intellectual property.

- Entering exclusive distribution agreements that limit market access.

It's also helpful to set thresholds for decisions requiring seller consent. For example, the agreement might stipulate that significant capital expenditures or major asset sales need prior seller approval.

In Johnson & Johnson v. Auris Health, J&J acquired Auris for $3.4 billion with potential earnouts of $2.35 billion. The agreement required J&J to prioritize the acquired technology. However, when J&J merged the technology with an internal competing project, causing delays, the court found that J&J had breached its obligations and misrepresented its intentions.

Finally, establish clear timelines for approval requests. For instance, the contract might state that the seller must respond within a set timeframe, with no response treated as consent. In 2022, only 23% of deals included covenants requiring buyers to manage businesses consistently with past practices. Given the rise in earnout disputes, sellers should push for detailed operating rules while allowing buyers enough flexibility to manage effectively. A well-crafted framework can align both parties' interests and pave the way for a smoother post-closing relationship.

Standardizing Accounting Policies and Measurement Methods

After setting your operating rules, the next step is ensuring consistent methods for measuring performance. Accounting disagreements are one of the top reasons earnouts end up in litigation. In fact, the number of U.S. lawsuits involving earnouts nearly doubled between the first quarter of 2022 and the first quarter of 2023. The core issue lies in the flexibility of accounting standards like GAAP, which involve a lot of judgment. This means two companies following GAAP can still report significantly different results. Establishing clear measurement methods alongside operating rules helps ensure fair and consistent performance evaluations.

Using Consistent Accounting Standards

Simply stating "GAAP" in agreements won't cut it - it leaves room for multiple interpretations. To avoid confusion, the SPA (Sales and Purchase Agreement) should outline a clear accounting hierarchy. Here's the recommended order:

- First, specific accounting policies explicitly defined in the SPA.

- Second, the historical accounting methods used by the target business before the deal closed.

- Third, general GAAP or IFRS standards.

To maintain consistency, freeze the accounting standards as of the signing date. This prevents any future changes from skewing calculations. Include a detailed breakdown of key accounting practices, such as revenue recognition, inventory valuation, capitalization policies, and intercompany pricing.

Since EBITDA isn’t a standardized GAAP term, it’s crucial to define it precisely. Specify allowable add-backs like transaction costs, non-recurring items, stock-based compensation, and extraordinary events. This ensures a fair comparison with pre-closing performance. Including a worked example or pro forma calculation in the SPA can help both parties interpret the formulas consistently.

Data Access and Audit Rights

To maintain transparency, give the seller explicit rights to access financial statements, supporting schedules, and the buyer’s personnel and systems. Standard agreements often allow for one audit per calendar year during the earnout period, with 30–60 days’ notice. These audits are typically conducted by an independent CPA firm to maintain objectivity.

If discrepancies arise, the buyer should provide access to underlying workpapers to resolve issues efficiently. For businesses integrated into the buyer’s operations, maintain a separate ledger - or "fence" - for the target’s books to ensure accurate performance tracking. Additionally, agreements should require financial records to be kept for at least three to four years after the deal ends.

Many audit clauses include a cost-shifting provision. For example, if an audit reveals that payments or net sales were understated by more than 10%, the buyer may be required to cover the auditor’s fees. Establishing clear audit rights can simplify resolving calculation disputes.

Resolving Calculation Disputes

A two-step dispute resolution process can help address issues efficiently. For technical disputes over calculations, use an independent accounting firm. For breaches of operational covenants or claims of bad faith, turn to a legal forum like arbitration or court.

When drafting the dispute resolution clause, clearly outline whether the third-party accountant will act as an expert or as an arbitrator. Set clear deadlines for submitting draft earnout statements, raising objections, and resolving disputes. Additionally, require any auditors involved to sign a non-disclosure agreement (NDA) to protect sensitive information. This structured approach ensures disputes are handled fairly and efficiently.

sbb-itb-97ecd51

Forfeiture, Termination, and Dispute Resolution

A well-drafted earnout agreement can still fall apart without clear remedies in place. To manage risks effectively, it’s essential to understand how forfeiture conditions work and how disputes can be resolved. This section dives into remedies, resolution strategies, and safeguards to ensure payment obligations are upheld.

When Earnout Rights Can Be Forfeited

The structure of an earnout determines who carries the burden of proof. If the earnout is a "condition precedent," the seller must demonstrate that the milestone has been achieved to claim payment. On the other hand, if it’s a "condition subsequent," the buyer must prove why the payment obligation no longer applies.

A case in point: In October 2020, the Delaware Court of Chancery reviewed S'holder Representative Servs. LLC v. Shire US Holdings, Inc., which involved a $45 million earnout tied to an experimental drug. The contract specified that payment was due unless "material safety or efficacy concerns" made regulatory approval impractical. Since the earnout was structured as a condition subsequent, the buyer (Shire) had to prove the existence of those safety concerns to avoid payment. This highlights how crucial it is to define precise forfeiture triggers in your agreements.

Your agreement should clearly outline the conditions that could lead to forfeiture, such as material breaches, fraud, or failure to meet regulatory milestones. Many agreements also allow buyers to offset earnout payments against indemnification claims for breaches of warranties.

Choosing a Dispute Resolution Method

Not every dispute should be handled the same way. Technical disagreements - like those involving revenue calculations or EBITDA adjustments - are often best resolved by an independent accounting firm. In contrast, legal disputes over contract interpretation or allegations of bad faith may need arbitration or court proceedings.

When selecting a dispute resolution method, decide whether the neutral party will act as an "expert" or an "arbitrator." Keep in mind that decisions made by arbitrators are largely unchallengeable due to FAA deference, while expert determinations are more limited in scope. Defining the neutral's role clearly can help avoid jurisdictional confusion later.

For example, in December 2022, the case of Fortis Advisors v. Dematic Corp. revolved around whether integrated products qualified as "Company Products" under earnout milestones. The buyer sought to refer the issue to a neutral accounting expert, but the court ruled that since the matter involved contract interpretation - a legal question - it had to be resolved in court instead of by the expert.

To streamline the process, establish strict timelines for resolving disputes. A common timeframe is 90 days for an expert to deliver a decision. Include language in the agreement stating that the decision is "final, binding, and non-appealable" to avoid prolonged disputes. Additionally, consider negotiating a buyout clause that allows the buyer to terminate the earnout early by paying a predetermined amount, sidestepping future disagreements.

Securing Payment Obligations

To ensure payments are protected, implement strong security measures alongside clear operational rules. Popular options include escrow accounts, holdbacks, letters of credit, and parent guarantees. In 2023, 90% of M&A deals incorporated at least one escrow account, and over half used multiple security mechanisms.

- Escrow accounts: A neutral third party, typically a bank, holds a portion of the purchase price until the earnout milestones are met. This approach provides security for both parties but ties up capital and incurs fees.

- Holdbacks: Buyers retain the funds directly instead of depositing them with a third party. While simpler and fee-free, holdbacks increase the seller's risk since the buyer controls the funds.

- Parent guarantees: These protect sellers if the buyer is a subsidiary, ensuring the parent company covers the payment in case of financial trouble. However, this is only as reliable as the parent’s financial strength.

- Letters of credit: A bank guarantees the payment, offering security to the seller. However, this method comes with high administrative costs and fees.

Some agreements also include springing security interests, which give sellers a claim on specific assets if the buyer defaults on payments. To prevent confusion, define the specific triggers for releasing funds from escrow - such as joint signatures, audit confirmations, or third-party verifications. It’s also crucial to clarify whether buyers can offset indemnity claims against earnout payments. Without clear terms, courts may prohibit such offsets, leaving buyers exposed to dual obligations.

| Security Mechanism | Primary Benefit | Primary Drawback |

|---|---|---|

| Escrow | Neutral third party protects both sides | Immobilizes capital; involves fees |

| Holdback | Simple; no third-party fees | Buyer controls funds; higher risk |

| Letter of Credit | Bank-guaranteed security | High administrative cost and fees |

| Parent Guarantee | Protects against subsidiary insolvency | Only as strong as the parent's credit |

Testing Scenarios and Collaborative Drafting

After defining clear metrics and structured payment terms, it's crucial to rigorously test your earnout framework before finalizing the agreement. A well-thought-out earnout can help avoid disputes, but skipping this step increases the risk of costly litigation. In fact, earnout-related lawsuits in the U.S. nearly doubled between Q1 2022 and Q1 2023.

Modeling Different Scenarios

Stress-test your earnout framework by simulating realistic risks. Think about scenarios like losing key customers, supply chain interruptions, or major price swings. Start with your post-closing integration plan and work backward to pinpoint where revenue and costs will be recorded and how the data will be tracked.

If your earnout relies heavily on just a few assumptions, that's a warning sign. These "pressure points" suggest you might need a simpler structure. For instance, if one customer accounts for 40% of earnout revenue, test scenarios where that customer reduces orders by 25%, 50%, or even stops ordering altogether. Also, factor in how future acquisitions or integrating the target company into a larger division could influence metrics.

To reduce ambiguity, include a detailed numerical example in the purchase agreement. This should outline how EBITDA or revenue is calculated, with clear add-backs and exclusions. Don’t just reference GAAP - show the math. By providing specific numbers, you can stress-test assumptions and clarify the intent of all parties, minimizing disputes later on. This kind of proactive modeling bridges the gap between theoretical metrics and actual performance, paving the way for collaborative adjustments.

Working with Legal, Financial, and Tax Advisors

Bring in your legal, financial, and tax advisors early in the process. Legal counsel should focus on drafting operational covenants and dispute resolution clauses. CPAs need to define performance metrics and add-back rules, while tax advisors ensure the earnout is classified as part of the purchase price rather than compensation - an important distinction for tax purposes.

"If you think hiring a professional is expensive, wait until you hire an amateur." - Prof. Chad D. Cummings, CPA, Esq.

By coordinating input from these experts, you can align all aspects - from legal terms to tax treatment - into a cohesive framework. For example, legal covenants like "commercially reasonable efforts" should include specific actions rather than vague language that could lead to disputes. Keep a detailed record of negotiation history to support contract interpretation if disagreements arise. With expert guidance, you can also determine if a simpler earnout structure would better achieve your goals.

When to Simplify Earnout Structures

Complex earnout formulas aren't always the best choice. If your earnout relies on intricate EBITDA models with multiple adjustments, consider switching to simpler milestone payments. Milestones tied to clear, third-party verifiable events - like regulatory approvals or product launches - are less prone to disputes and accounting manipulation.

"If the earn-out is sensitive to a small number of assumptions, consider a simpler milestone structure or a fixed deferred payment instead." - Prof. Chad D. Cummings, CPA, Esq.

Revenue-based metrics are easier to measure than EBITDA but can still be manipulated through discounting or bundling. If the earnout hinges on just a few key assumptions, you might simplify it further with fixed milestone payments or a reverse earnout model. In a reverse earnout, the buyer issues a promissory note for the maximum amount at closing and forgives portions if targets aren't met. The goal here is to strike a balance between enforceability and practicality, creating a structure that avoids future disputes over today's valuation challenges.

Conclusion

Crafting enforceable earnout clauses requires precision, consistency, and collaboration. The growing reliance on earnouts - rising from 21% of deals in 2022 to 33% in 2023 - has coincided with a significant increase in earnout-related lawsuits during the same period. Many of these disputes arise from unclear language, inconsistent accounting methods, and vague operational covenants.

To tackle these issues, your agreement should include clear, measurable metrics with detailed examples of how calculations will be made. For "efforts" clauses, avoid ambiguous terms like "commercially reasonable" and instead provide specific, contractual benchmarks to guide interpretation. Include operational guardrails that strike a balance between the buyer’s business discretion and the seller’s protection against actions that could jeopardize earnout targets. This approach promotes consistency in operations and accounting practices.

When it comes to accounting, standardize with detailed schedules that clearly define revenue, expenses, and add-backs. Avoid relying solely on generic GAAP references. Incorporate strong audit rights and clearly differentiate between expert determination for calculation disputes and arbitration for breaches of contract. This separation ensures disputes are handled by the right professionals, reducing the likelihood of costly litigation and simplifying the resolution process.

Earnouts are intricate arrangements with many interdependent components. To ensure a solid structure, involve legal, financial, and tax advisors early in the process. Use scenario modeling to stress-test your framework. If your earnout depends heavily on a few key assumptions, it may be worth exploring simpler alternatives, such as milestone payments or fixed deferred structures.

FAQs

What are common disputes in earnout clauses, and how can they be prevented?

Disagreements over earnout clauses often stem from conflicting interpretations of performance metrics and how they’re calculated. For instance, disputes may arise over whether benchmarks like EBITDA, revenue, or net income have been met. This is especially tricky when terms like "adjusted EBITDA" or specific accounting methods aren’t clearly defined. Tensions can also escalate if buyers accuse sellers of financial misrepresentation or if sellers claim buyers deliberately underreported results.

Other common friction points include operational changes post-acquisition - like buyers modifying the business model in ways that affect performance - seller departures before the earnout period concludes, and unexpected events such as economic downturns or force majeure.

To minimize these risks, it’s crucial to spell out all metrics, accounting standards, and any necessary adjustments in the clause. Sellers should be granted audit rights, and the agreement should include provisions for a neutral third-party auditor to address disputes. Adding covenants to limit major operational changes without seller input and specifying how unforeseen events will be managed can also help. Finally, a dispute resolution mechanism, such as binding arbitration, can save both parties from lengthy and expensive litigation.

When considering acquisitions involving earnouts, tools like Kumo can assist in identifying potential targets and valuation discrepancies early on, allowing more time to craft detailed and enforceable agreements.

What performance metrics should buyers and sellers agree on for an earnout?

To ensure an earnout agreement is both fair and enforceable, buyers and sellers need to establish clear, measurable performance metrics that align with the business's main value drivers. These metrics often include financial indicators like gross revenue, EBITDA, or net income, but they can also focus on operational goals such as customer retention rates, new customer acquisition, or product-line growth - particularly if these are critical to the business's success.

It's equally important to spell out how these metrics will be calculated. This includes specifying the accounting standards to be used (e.g., GAAP), any adjustments that may apply, and the timing for financial reporting. Defining the measurement period - whether it spans one year or up to five years - and clarifying whether the targets are cumulative or assessed annually can help prevent confusion. To further minimize disputes, consider including audit rights or using an independent verification process to ensure the calculations are transparent and accurate.

Tools like Kumo can also be valuable for benchmarking these metrics against similar deals, helping to confirm that the targets are reasonable and consistent with industry norms. By agreeing on detailed terms and incorporating safeguards, both parties can protect their interests and reduce the chances of misunderstandings or disputes after the deal is finalized.

What steps can ensure earnout payments are secure?

To protect earnout payments and ensure they are enforceable, parties often rely on escrow accounts or holdback arrangements. In these setups, a portion of the purchase price is set aside with a neutral third party, like an escrow agent. The funds are only released once the agreed performance targets are met. This approach safeguards the seller while giving the buyer a structured way to manage contingent payments.

Another method involves granting a security interest or lien on specific assets of the acquired business, such as inventory or intellectual property. This provides the seller with a fallback option if the earnout payment isn't fulfilled. On top of that, incorporating audit rights allows the seller to independently verify performance metrics, minimizing disputes about whether the targets were achieved.

By using tools like escrow accounts, secured liens, and audit rights - alongside well-defined performance benchmarks and dispute resolution clauses - both buyers and sellers can approach earnout agreements with greater confidence.