Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

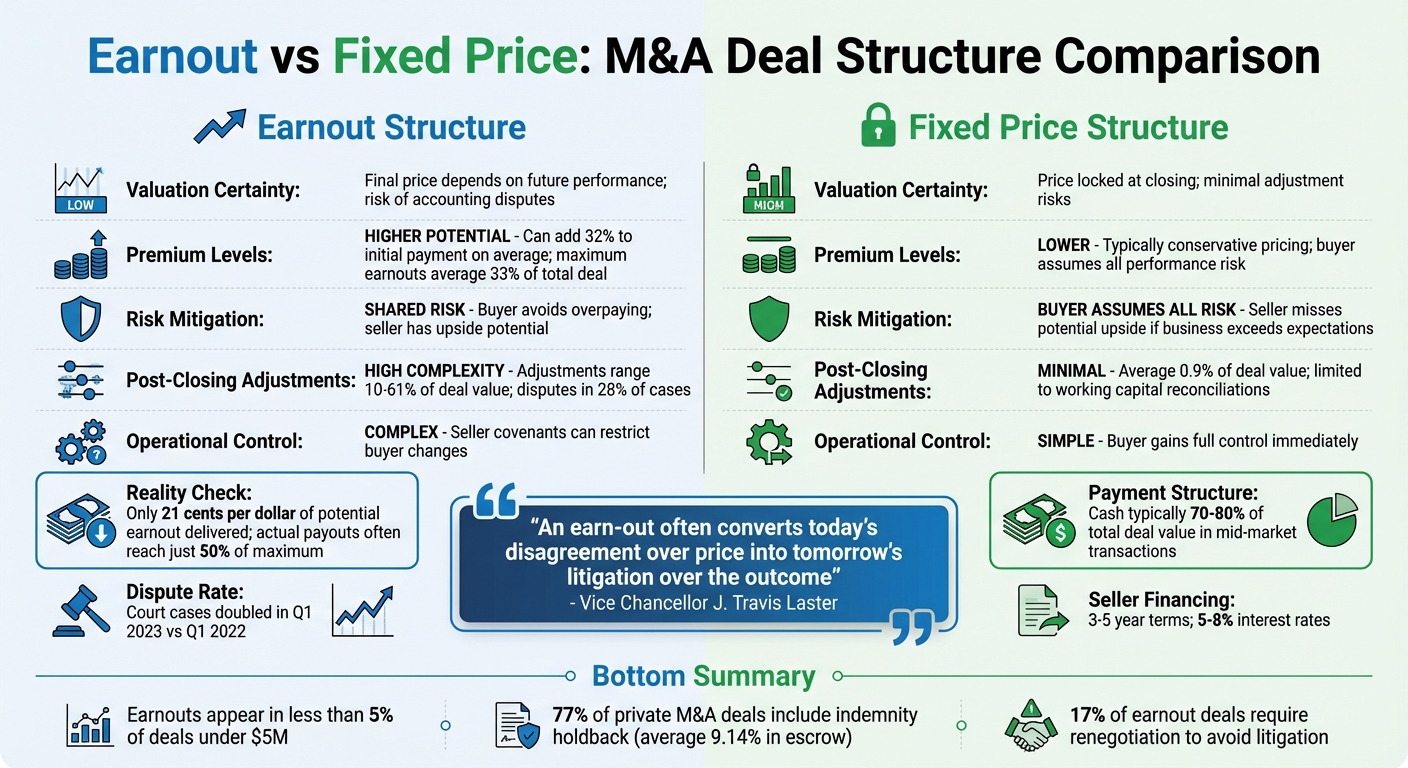

When buyers and sellers can’t agree on a business's value, earnouts often help close the gap. An earnout ties part of the purchase price to specific performance milestones after the deal closes. This approach reduces risk for buyers while offering sellers the chance for higher payouts if targets are met. However, earnouts can lead to disputes and require ongoing collaboration, which adds complexity.

In contrast, fixed price structures set the total purchase amount upfront, providing certainty for both parties. While simpler, this approach often results in lower valuations because buyers take on all the performance risk.

Key Differences:

- Earnouts: Flexible, performance-based, but prone to disputes. Can increase total payout by up to 33%.

- Fixed Price: Simple and upfront, but often conservatively priced and less adaptable to future outcomes.

Choosing the right structure depends on the deal’s specifics, including growth potential, risk tolerance, and the need for post-closing involvement.

Earnout Modeling in M&A Deals and Merger Models

1. Earnout Structures

An earnout structure allows part of the purchase price to be deferred, tying it to the business achieving specific post-deal targets. Essentially, the final price depends on actual performance rather than just projections.

"An earnout is a useful means of bridging a valuation gap and getting a deal done." - Jacob Orosz, President, Morgan & Westfield

Valuation Certainty

Earnouts offer a performance-based approach to valuation. Instead of relying solely on forecasts, the ultimate purchase price is determined by the business's actual performance after the deal. This method is especially relevant in industries where future value hinges on uncertain outcomes, like FDA approvals in life sciences or patent issuances in tech.

Premium Levels

With earnouts, sellers have the potential to secure higher payouts since buyers reward proven growth. When performance targets are met, earnouts can significantly boost the total transaction value, with maximum earnouts typically averaging around 33% of the total deal.

Risk Mitigation

Earnouts create a balanced risk-sharing arrangement between buyers and sellers. Buyers avoid overpaying if the business underperforms, while sellers stand to gain if the business exceeds growth expectations. This type of structure is more common in markets where buyers can shift some of the uncertainty onto the seller. However, earnouts are rare in smaller deals under $5 million, appearing in less than 5% of such transactions.

Post-Closing Adjustments

Unlike fixed-price agreements that conclude the financial relationship at closing, earnouts require ongoing collaboration between the buyer and seller. Buyers must provide detailed financial reports to help sellers confirm whether targets are being met. This structure also keeps sellers engaged during the transition period, helping to maintain critical relationships and achieve key milestones. That said, earnouts can introduce complications. Disputes over earnout provisions arise in at least 28% of cases, and 17% of deals involving earnouts have required renegotiation to avoid litigation.

Next, let’s explore how fixed-price structures address valuation challenges.

2. Fixed Price Structures

A fixed price structure establishes a set purchase amount and payment schedule upfront. Payments are made either in cash or through seller financing notes with fixed interest rates and terms. Below, we’ll explore how fixed price structures bring clarity, influence valuation, manage risk, and address post-closing adjustments.

"Seller financing differs from earnouts in that a fixed amount and payment schedule are agreed to in advance. In contrast, an earnout is contingent on a future event, and the amount is therefore unpredictable." - Jacob Orosz, President, Morgan & Westfield

Valuation Certainty

One of the biggest benefits of fixed price structures is the certainty they provide. Sellers know exactly how much they’ll receive, eliminating concerns about hitting performance targets or how financial metrics might be interpreted. In mid-market transactions, cash typically accounts for 70% to 80% of the total deal value. This structure allows sellers to cash out fully at closing, avoiding the need to keep "skin in the game".

Premium Levels

The trade-off for this certainty often comes in the form of a lower valuation. Buyers, who bear the performance risk, tend to offer more conservative prices compared to earnout-based deals. While earnout structures can result in a higher overall sales price by tying payments to actual performance, fixed price deals prioritize immediate funds, sometimes at the expense of potential upside.

Risk Mitigation

In a fixed price arrangement, the buyer takes on the risk of the business not meeting its projections after the deal closes. Despite this, the buyer is still obligated to pay the full agreed-upon amount. For sellers, this structure avoids the disputes common in earnout deals, such as disagreements over accounting methods or concerns about EBITDA manipulation.

Post-Closing Adjustments

Even with a fixed purchase price, most deals include working capital adjustments to ensure the buyer receives the business with a normalized level of assets. These adjustments account for changes in the company’s financial condition between signing and closing, such as shifts in cash, debt, or inventory. For example, a 2014 survey found that 77% of private M&A deals included an indemnity holdback, with an average of 9.14% of the purchase price placed in escrow to cover post-closing obligations. Seller financing notes typically span three to five years, carry interest rates between 5% and 8%, and often include a "right of offset" for indemnification claims.

With these details in mind, let’s examine how fixed price structures compare to other transaction approaches.

sbb-itb-97ecd51

Pros and Cons

Earnout vs Fixed Price M&A Deal Structures Comparison

When deciding between an earnout and a fixed price deal structure, the choice often boils down to balancing certainty with the possibility of greater financial rewards. Each option shifts the risk differently between the buyer and seller, and understanding these dynamics is essential during negotiations. Below is a comparison of how these two structures measure up across key factors that influence valuation and risk.

Here’s a breakdown of the main differences:

| Feature | Earnout Structure | Fixed Price Structure |

|---|---|---|

| Valuation Certainty | Low; the final price hinges on future performance, which can lead to accounting disputes. | High; the price is locked in at closing, reducing adjustment risks. |

| Premium Levels | Offers the chance for a higher total payout if performance goals are achieved. On average, earnouts can add 32% to the initial payment. | Typically lower; buyers factor in the performance risks they’re taking on. |

| Risk Mitigation | Risk is shared; the buyer avoids overpaying, while the seller has a shot at additional earnings. | The buyer assumes all performance risk, while the seller could miss out on extra gains if the business exceeds expectations. |

| Post-Closing Adjustments | Can involve substantial adjustments (ranging from 10% to 61% of the deal value), with disputes arising in roughly 28% of cases. | Minimal adjustments (averaging just 0.9% of the deal value), usually limited to working capital reconciliations. |

| Operational Control | More complex; sellers often impose covenants to protect their earnout, which can restrict the buyer's ability to make changes. | Straightforward; buyers gain full operational control immediately. |

These figures highlight the trade-offs between performance-based and fixed valuation approaches. With earnouts, sellers may face challenges in realizing their full potential payout. On average, only 21 cents per dollar of potential earnout is delivered, and actual payouts often reach just 50% of the maximum. Moreover, disputes are common - court cases involving "earnout" and "M&A" doubled in Q1 2023 compared to the same period in 2022, underscoring the legal risks tied to these arrangements.

Vice Chancellor J. Travis Laster of the Delaware Court of Chancery aptly summarized the challenge:

"An earn-out often converts today's disagreement over price into tomorrow's litigation over the outcome".

In contrast, fixed-price deals prioritize immediate clarity and simplicity, though they may leave potential gains on the table.

Conclusion

Earnouts have become a pivotal tool in M&A deals, helping bridge valuation gaps that might otherwise derail transactions. By shifting how risk is shared, they allow buyers to avoid overpaying for potential that hasn’t yet materialized, while giving sellers a chance to secure higher payouts if their business performs as expected.

Choosing between an earnout and a fixed price structure depends on the unique dynamics of each deal. Earnouts are particularly useful when there’s disagreement over future growth, when the business relies on key management staying involved, or when economic uncertainty clouds visibility. In these cases, earnouts can boost the overall transaction value. Fixed price structures, on the other hand, make sense for businesses with a stable history of earnings, sellers looking for full liquidity at closing, or buyers who need immediate control without the complexities of tracking performance metrics.

However, the accounting treatment of earnouts under ASC 805 adds another layer of complexity. Earnouts must be recorded at fair value on the acquisition date, and any adjustments can impact reported earnings, potentially introducing volatility - especially when payment structures involve caps or floors that create uneven risk distributions. These factors make careful deal structuring absolutely essential.

Given that earnouts often lead to disputes, it’s critical to establish clear metrics and robust resolution mechanisms. Metrics should be well-defined, rely on objective milestones whenever possible, and include strong dispute resolution clauses in the purchase agreement to address disagreements effectively.

FAQs

What risks should you consider with earnouts in M&A deals?

Earnouts in M&A deals can be tricky because they hinge on hitting future performance goals. If the criteria for those goals aren’t spelled out clearly, it can lead to disputes between buyers and sellers. This is why having well-defined metrics and detailed contractual terms is so important - it helps prevent misunderstandings and ensures everyone is on the same page.

Another issue is operational misalignment. After the acquisition, sellers might lose the drive to meet earnout targets, or in some cases, they might even manipulate results to boost payouts. On top of that, the process of structuring earnouts can get complicated, especially when it comes to agreeing on performance timelines or financial benchmarks. Miscommunication during this phase can create further challenges.

Even though earnouts can be a useful tool to bridge valuation differences and finalize deals, their uncertain nature means they require thorough planning and open communication to avoid potential pitfalls.

How do earnouts influence a business's valuation during a deal?

Earnouts can play a big role in determining a business's value by tying part of the payment to how the company performs in the future or hits specific milestones. This setup helps balance the risk between buyers and sellers since the final price hinges on meeting those agreed-upon goals.

For buyers, earnouts are a way to keep the seller invested in the company’s success after the sale. For sellers, they present an opportunity to earn more if the business thrives post-sale. That said, it’s crucial to clearly outline the terms and performance metrics to avoid misunderstandings and ensure both sides are on the same page.

Why would a seller choose a fixed price over an earnout in a deal?

When selling a business, some sellers prefer a fixed price structure over an earnout to eliminate uncertainty and guarantee an upfront payment. Earnouts are tied to the business's future performance, which can be unpredictable and might spark disagreements over whether specific performance goals are met.

Opting for a fixed price ensures the seller avoids potential disputes down the road. It also provides a clear and immediate payout, offering financial security and a smoother transaction experience.