Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

Form 8594 is essential for SMB asset sales. It ensures the purchase price is allocated across assets like inventory, equipment, goodwill, and intangibles. Both buyers and sellers must file identical forms with their tax returns for the year of the sale. Proper allocation impacts tax outcomes, such as depreciation for buyers and income classification for sellers. Errors or mismatched filings can trigger IRS audits and penalties.

Key Takeaways:

- Purpose: Allocate the purchase price across seven asset classes using the residual method.

- Who Files: Both buyer and seller must file Form 8594 with their tax returns.

- Impact: Buyers determine asset depreciation; sellers calculate taxable gains.

- Common Errors: Inconsistent filings, omitting forms of consideration, or ignoring adjustments.

- Best Practices:

- Align allocations in the purchase agreement.

- Use fair market values for accurate reporting.

- File supplemental forms for post-sale adjustments.

Filing correctly protects your tax benefits and avoids IRS scrutiny. Early coordination with tax professionals and proper documentation are critical.

IRS Form 8594 walkthrough (Asset Acquisition Statement under IRC Section 1060)

Purchase Price Allocation and Asset Classes

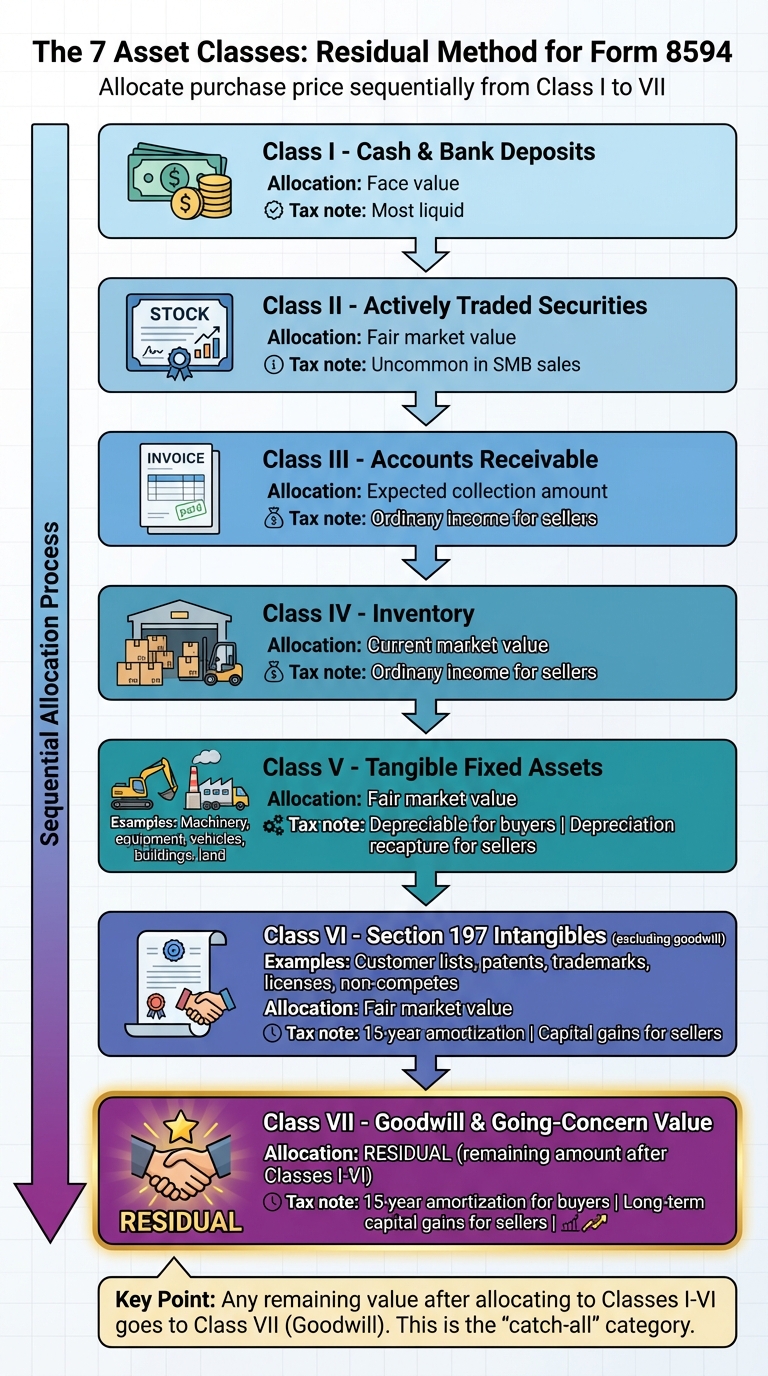

Form 8594 Seven Asset Classes for Purchase Price Allocation

Purchase price allocation (PPA) is the process of dividing the total purchase price of a business among its various assets. In small and medium-sized business (SMB) sales, this allocation directly impacts the buyer’s ability to claim depreciation and amortization deductions, while determining the seller’s taxable gain. The IRS requires both buyers and sellers to report this allocation using seven specific asset classes on Form 8594, following a specific order.

The allocation process uses a residual method under IRC §1060. This method begins with the total consideration paid for the business, which includes cash, assumed liabilities, and any contingent payments with a determinable value. The total is then allocated sequentially to each asset class based on fair market value (FMV). Any leftover value after accounting for Classes I through VI is assigned to goodwill and going-concern value in Class VII. This approach ensures that goodwill acts as the "catch-all" category, capturing any remaining value once all other identifiable assets are accounted for. Below is a breakdown of each asset class and its role in the allocation process.

The Seven Asset Classes Explained

The asset classes are arranged in order of liquidity, starting with the most liquid and moving toward intangible assets:

- Class I: Cash and bank deposits. These are allocated at face value.

- Class II: Actively traded securities, such as publicly traded stocks or Treasury bills. These are uncommon in typical SMB business sales.

- Class III: Accounts receivable and customer notes receivable. For sellers, amounts allocated here are generally taxed as ordinary income.

- Class IV: Inventory, including finished goods, work-in-process, and raw materials. Like Class III, inventory sales are also taxed as ordinary income.

- Class V: Tangible fixed assets like machinery, equipment, vehicles, furniture, buildings, and land. Buyers often prefer higher allocations here because these assets can be depreciated, and some may qualify for bonus depreciation or Section 179 expensing. Sellers, however, may face depreciation recapture, which taxes part of the gain at ordinary income rates rather than the lower capital gains rate.

- Class VI: Section 197 intangibles, excluding goodwill. This includes customer lists, patents, licenses, trademarks, and non-compete agreements. Buyers amortize these over 15 years, while sellers typically recognize capital gains.

- Class VII: Goodwill and going-concern value. For buyers, goodwill is amortized over 15 years on a straight-line basis, without bonus depreciation. Sellers, on the other hand, often benefit from the lower tax rates associated with long-term capital gains. This makes Class VII a critical point in negotiations - buyers aim to minimize it for faster deductions elsewhere, while sellers prefer it for favorable tax treatment.

Proper classification is crucial for compliance with Form 8594 and for optimizing tax outcomes for both parties.

How the Residual Allocation Method Works

Here’s how the residual method is applied step-by-step. Start with the total purchase consideration, which includes cash, assumed liabilities, and any contingent payments with determinable FMV. First, allocate to Class I assets at their face value. Once that’s done, move to Class II, assigning value up to the FMV of any securities. Continue this process through Classes III, IV, V, and VI, always allocating up to each class’s FMV before proceeding to the next.

The remaining amount, after all identifiable assets in Classes I through VI have been accounted for, is assigned to Class VII - goodwill and going-concern value. This residual amount reflects the premium paid for elements like the business’s reputation, customer relationships, workforce synergies, and other intangible factors that don’t fit into earlier classes.

Accurate FMV assessments for tangible and identifiable intangible assets are essential. Overvaluing inventory or equipment can artificially lower goodwill, while undervaluing them inflates it. Either scenario can draw IRS scrutiny if the allocation appears unreasonable or inconsistent with market norms.

How to Prepare Form 8594 Correctly

Getting Form 8594 right requires careful coordination, accurate valuations, and thorough documentation. The asset allocation you report must align with your purchase agreement, and every asset class needs proper fair market value (FMV) documentation. Doing this correctly from the outset helps avoid IRS scrutiny and ensures both parties can claim the tax benefits they’re entitled to.

Match Allocations in Your Purchase Agreement

To ensure consistency, the allocations in your purchase agreement should match the details reported on Form 8594. Finalize the purchase price allocation during the drafting of the Asset Purchase Agreement (APA) - don’t leave it for after the deal closes. Include a clause in the APA that obligates both parties to report the asset values on their respective Form 8594 filings exactly as agreed. These allocations are binding unless the IRS deems them improper and makes adjustments, which can impact the seller’s taxable gain and the buyer’s depreciation basis.

For example, if the buyer and seller report different values for Class V equipment ($300,000 vs. $200,000), it could trigger an IRS investigation. Work with a tax advisor to document the allocation method, FMV assessments, and the rationale behind the values assigned to each asset class. This step is critical to avoid discrepancies and ensure smooth compliance.

How to Value Tangible Assets

For tangible assets, valuation methods vary by class. Cash and bank deposits (Class I) are straightforward and assigned their face value. Accounts receivable (Class III) should reflect the amount expected to be collected, taking into account any doubtful accounts. Inventory (Class IV) should be valued based on current market prices, factoring in age, condition, and turnover rates.

Fixed assets like equipment, vehicles, and buildings (Class V) require more detailed analysis. This might involve reviewing comparable sales, depreciation schedules, and replacement costs. For complex valuations - such as inventory (Class IV), fixed assets (Class V), or major intangibles - consider hiring third-party appraisers. An independent appraisal can provide defensible documentation if the IRS questions your allocation. For small and midsize business acquisitions, using appraisers with credentials like Accredited Senior Appraiser (ASA) or Certified Valuation Analyst (CVA) can add credibility to your filing. Accurate valuations not only simplify the filing process but also ensure compliance with tax regulations.

How to Assign Value to Goodwill and Intangibles

Once you’ve assigned FMV to Classes I–VI, the remaining value is allocated to Class VII - goodwill and going-concern value. This category includes intangible elements like the business’s reputation, customer relationships, and workforce synergies that don’t fit into other classes. Before allocating this residual value, it’s essential to separately value identifiable Class VI intangibles, such as customer lists, patents, trademarks, licenses, or non-compete agreements.

For instance, a non-compete agreement might be valued based on the seller’s ability to compete and the potential economic harm their competition could cause. Buyers typically prefer higher allocations in Class V and VI because these assets allow for faster depreciation and amortization. On the other hand, sellers often favor Class VII allocations, as they benefit from capital gains treatment. To defend your allocations, document your methodology with appraisals and market comparables. This approach ensures proper filing and minimizes the risk of IRS penalties.

sbb-itb-97ecd51

How to Complete and File Form 8594

Form 8594 is divided into three key sections, each serving a specific purpose in reporting asset acquisition details. Here's a breakdown of what each part covers:

- Part I – General Information: This section requires basic details about the transaction, including the names, addresses, and taxpayer identification numbers (TINs) of both parties, the exact closing date of the sale (as stated in the asset purchase agreement), and the total consideration paid. For individuals or sole proprietors, use the seller's Social Security Number (SSN); for entities, provide their Employer Identification Number (EIN). You'll also indicate whether the buyer and seller agreed on the same allocation and whether the form is an original or supplemental filing.

- Part II – Original Statement of Assets Transferred: Here, you allocate the purchase price across seven asset classes. Instead of listing each asset individually, report the total amount allocated to each class. The total allocation must equal the purchase price reported in Part I and match the allocation stated in the purchase agreement.

- Part III – Supplemental Statement: This section is only required if there are changes to the purchase price after the initial filing, such as adjustments for earn-outs, working capital, or dispute settlements. Both parties must file an updated Form 8594 for the tax year in which the change occurs, reflecting the revised allocations.

Who Must File and When

Both buyers and sellers are required to file Form 8594 for any "applicable asset acquisition." This applies to the sale of a group of assets that constitute a trade or business, particularly when goodwill or going-concern value is involved. Each party must attach the form to their respective federal income tax return (e.g., Form 1040, 1120, 1120-S, etc.) for the tax year in which the sale took place. The form is due with the tax return for that year or by the extended filing deadline.

It's crucial that the allocations reported on Form 8594 align with other tax filings. For buyers, the reported asset basis is used in depreciation and amortization schedules starting the year after the acquisition. For sellers, these amounts flow into Form 4797 (to report business property sales and depreciation recapture) and Schedule D (to report capital gains on assets like goodwill). Any mismatches between these forms can raise red flags, potentially triggering IRS audits. Ensuring consistency across filings is essential.

Mistakes to Avoid When Filing

Errors on Form 8594 can lead to IRS scrutiny, reallocation of the purchase price, and even penalties. Here are common pitfalls to watch for:

- Leaving Out Forms of Consideration: Make sure to include all forms of consideration on Line 3 of Part I. This includes not just cash but also assumed liabilities, seller notes, and contingent payments. Omitting these can result in an inaccurate purchase price and misaligned tax reporting.

- Failing to File Supplemental Forms: If the purchase price changes due to post-closing adjustments - like earn-outs or dispute resolutions - you must file a supplemental Form 8594. The IRS requires updated forms in any year where the buyer’s cost or seller’s realized amount changes.

- Discrepancies Between Filings: If the buyer and seller report different allocations, it can trigger an IRS audit. The IRS may disregard both parties' filings and impose its own allocation, which often results in less favorable tax outcomes. To avoid this, coordinate closely with the other party, document your allocation method using appraisals or schedules, and ensure your Form 8594 aligns with Form 4797, Schedule D, and depreciation records.

How to Avoid IRS Penalties

When it comes to purchase price allocation, the IRS considers the purchase agreement as binding evidence - unless it finds the amounts to be improper. If the numbers on your Form 8594 don’t align with the purchase agreement, or if the buyer and seller report different totals, the IRS may reallocate the amounts and impose penalties. Tax advisors point out that mismatches between buyer and seller filings often lead to IRS audits, with asset allocation disputes being a common focus during small business sale examinations.

To avoid these issues, make sure you and the other party coordinate your allocations before closing. This means agreeing on the allocations in the purchase agreement and exchanging draft Forms 8594 to ensure both parties report identical numbers. Don’t forget to include all forms of consideration in the total purchase price - this includes cash, assumed liabilities, installment notes, earn-outs, and non-cash items. Missing any of these can result in adjustments and potential penalties.

If there are post-closing adjustments that change the purchase price, you need to file a supplemental Form 8594 right away. Keep track of any contingent payments to ensure your filings stay up to date.

It’s also a good idea to involve a qualified CPA or tax attorney early in the process. They can help establish allocations based on fair-market value and ensure your Form 8594 aligns with your depreciation schedules, Form 4797, and Schedule D. Additionally, maintain detailed documentation, like appraisal reports and valuation studies, to back up your allocations if the IRS comes knocking.

Here’s a quick look at common errors and how to avoid them:

Table: Errors vs. Correct Practices

| Issue / Error Area | Common Error in SMB Deals | Correct Practice to Avoid IRS Penalties |

|---|---|---|

| Consistency between buyer & seller | Buyer and seller report different allocations or totals on Form 8594, or one party omits the form entirely. | Agree on a written allocation schedule in the purchase agreement and ensure identical numbers on both Forms 8594; coordinate closely. |

| Incomplete consideration | The allocation omits assumed liabilities, contingent payments, or non-cash consideration. | Include all forms of consideration in the total purchase price and reflect them consistently in the allocation and on Form 8594. |

| Ignoring post-closing adjustments | Post-closing changes - such as working capital true-ups, earn-outs, or disputes - are not updated on Form 8594. | If the buyer's cost or seller's amount realized changes, file a supplemental Form 8594 reflecting the updated allocation. |

Conclusion

Filing Form 8594 correctly is a crucial step in any small or medium-sized business (SMB) acquisition. The purchase price allocation you determine influences depreciation schedules, gain or loss calculations, and future tax obligations. Mistakes or mismatched filings can lead to audits, reallocation, and penalties.

To ensure accuracy, start with alignment between both parties. The allocation should be clearly agreed upon in the purchase agreement and reported identically on both Forms 8594. This includes accounting for all forms of consideration - cash, assumed liabilities, seller notes, and contingent payments. Using the residual method, allocate the purchase price across the seven asset classes. When the numbers align and the documentation is clear, you minimize the risk of IRS scrutiny and safeguard the tax benefits negotiated during the deal.

Timely filing is equally important. Attach Form 8594 to your federal income tax return for the year of the sale. If there are any post-closing adjustments, submit a supplemental filing to reflect the changes.

It’s wise to involve a qualified CPA or tax attorney early in the process. They can guide you in establishing fair market value allocations, coordinating with the other party, and ensuring your Form 8594 aligns with your depreciation schedules and other tax filings. Keep thorough records, such as appraisals, valuation studies, and correspondence, to be prepared in case the IRS raises questions. By focusing on accurate asset valuation, proper allocation, and timely filing, you can turn this compliance task into a way to protect your investment and optimize your tax outcomes.

FAQs

What happens if the buyer and seller report different information on Form 8594?

If the buyer and seller provide conflicting details on Form 8594, it can catch the attention of the IRS and might even lead to an audit. Such discrepancies can result in penalties, changes to the asset purchase price, and extra tax liabilities, which may include interest charges. On top of that, these inconsistencies could spark legal disputes between the parties, creating even more challenges. To steer clear of these problems, it’s essential for both parties to ensure their information on the form matches.

What is the residual method, and how does it affect the allocation of the purchase price in a business acquisition?

The residual method is a way to divide the purchase price of a business acquisition among various asset categories. It focuses first on assigning value to identifiable tangible and intangible assets - like equipment or patents - based on their fair market value. After this step, any leftover amount is allocated to goodwill or other intangible assets.

This method can play a major role in tax planning, as the amounts assigned to goodwill or intangible assets often follow different depreciation or amortization rules than tangible assets. Proper allocation is crucial to meet IRS requirements and make the most of potential tax advantages.

Why should I work with a tax professional when filing Form 8594?

When filing Form 8594, working with a tax professional can make a world of difference. Their expertise ensures your filing complies with IRS rules and helps you steer clear of expensive mistakes. They can spot potential red flags, like inconsistencies that could lead to audits or penalties, and offer insights into the tax effects of your transaction.

This expertise is particularly helpful in the case of small and medium-sized business (SMB) acquisitions, where correctly reporting purchase price allocations is critical. With their guidance, you can safeguard the accuracy of your tax documents and make the entire process far less stressful.