Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

When valuing software companies, physical assets like servers or office furniture often hold little weight. Instead, the focus shifts to intangible assets - proprietary code, patents, customer relationships, brand reputation, and trade secrets. These assets are critical because they often account for the majority of a software company's value, with goodwill alone typically making up two-thirds of acquisition prices. However, these assets often don’t appear on balance sheets due to accounting rules, creating a gap between market value and book value.

Key methods to evaluate software intangibles include:

- Income Approach: Focuses on future cash flows, often using discounted cash flow (DCF) analysis.

- Market Approach: Compares similar transactions or assets, though finding true comparables can be challenging.

- Cost Approach: Estimates the expense of recreating or replacing the asset but doesn’t reflect future earnings potential.

Specialized techniques like the Relief from Royalty Method, Multi-Period Excess Earnings Method, and With and Without Method help refine valuations by focusing on licensing cost savings, excess earnings, or alternative scenarios.

Challenges include subjective valuations, technology obsolescence, and market volatility. Blending multiple methods and validating results can improve accuracy. For SaaS companies, metrics like Monthly Recurring Revenue (MRR) and the Rule of 40 (growth rate + profit margin ≥ 40%) are often used for benchmarking.

Accurate valuation isn’t just about pricing - it informs better decision-making, from securing investments to planning acquisitions.

Revealed: How to Maximize Your Tech Company’s Worth with These 3 Appraisal Methods!

Primary Valuation Methods for Software Intangibles

Three Primary Software Valuation Methods Compared

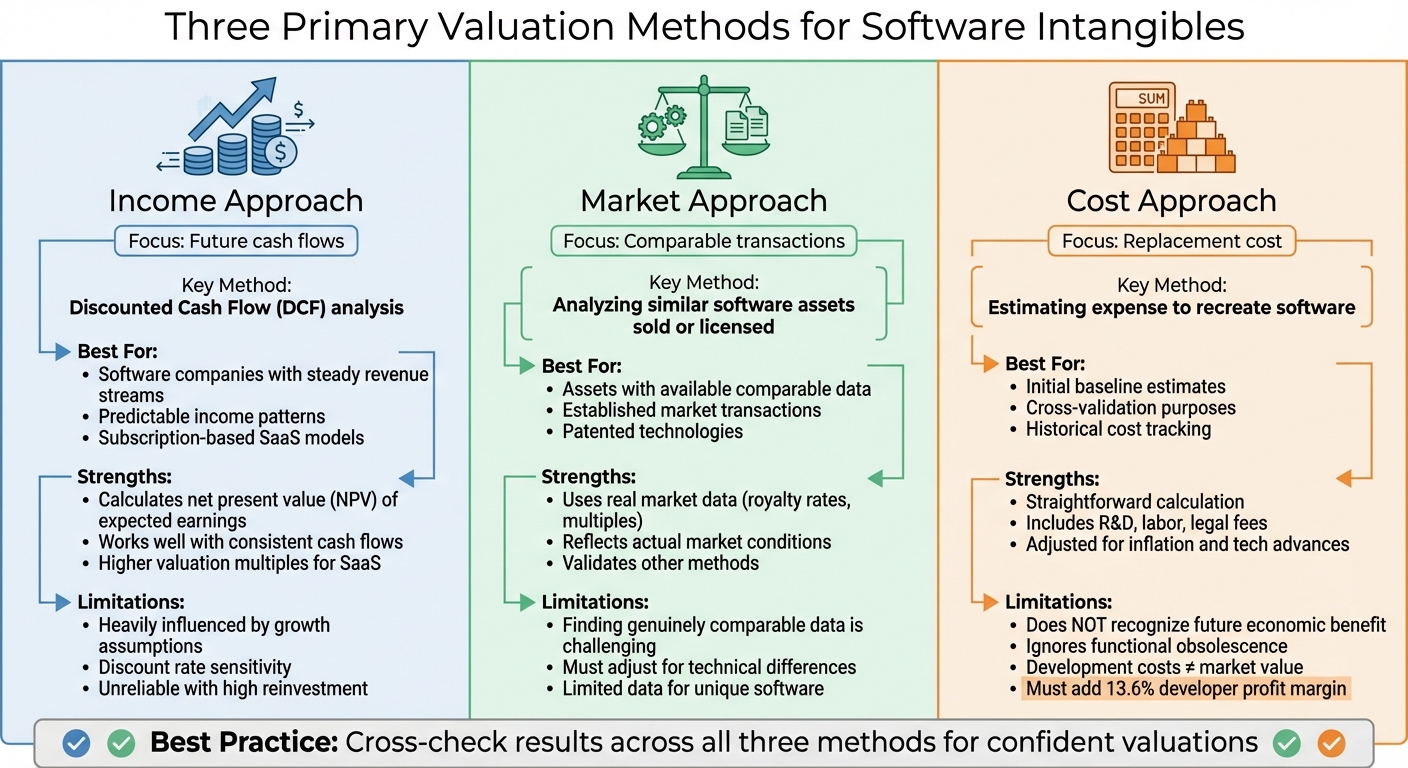

When it comes to valuing software intangibles, three primary methods take center stage: the income approach, the market approach, and the cost approach. Each method offers a unique perspective, and understanding their ins and outs helps provide a well-rounded evaluation of a software acquisition. Let’s break down how each approach works and where it shines - or falls short.

The income approach zeroes in on future cash flows. Using discounted cash flow (DCF) analysis, it calculates the net present value (NPV) of expected earnings over the asset's lifespan. This method works best for software companies with steady revenue streams and predictable income. However, it’s heavily influenced by growth assumptions and discount rates. Since high reinvestment often reduces current profitability, analysts frequently rely on revenue multiples rather than traditional metrics like EBITDA. For instance, subscription-based SaaS models typically generate consistent cash flows, making them prime candidates for higher valuation multiples.

The market approach takes a comparative route, assessing value by examining similar software assets that have been sold or licensed. This involves studying comparable transactions, such as royalty rates, market multiples, or prior acquisitions, while adjusting for differences in technical features or market conditions. According to Scott Weingust and Emma Bienias from Stout, this method often requires analyzing deals involving comparable patented technologies or, ideally, the specific software being valued. The challenge? Finding genuinely comparable data for unique software assets. When reviewing comparables, it’s essential to consider factors like technical similarities, jurisdictional differences, and any ongoing litigation.

The cost approach estimates value based on the expense of recreating or replacing the software’s functionality. This includes costs like R&D, labor, and legal fees, adjusted for inflation and technological advancements. While straightforward, this method has notable limitations for software valuation. Scott Weingust, Managing Director at Stout, highlights its primary weakness:

The main drawback of the Cost Approach is that it does not recognize the future economic benefit provided to the owner of the asset.

Additionally, it doesn’t account for functional obsolescence. For example, software developed with outdated programming languages might have cost $1 million to create, but modern tools could replicate it for a fraction of that amount. To refine this approach, appraisers must adjust historical costs to current values and include factors like a 13.6% developer profit margin and entrepreneurial incentives.

A practical way to strengthen any valuation is by cross-checking results across these methods. When multiple approaches yield a similar range, it adds confidence to the final assessment. This multi-method strategy helps balance out the limitations inherent in each individual method.

Specialized Valuation Methods for Software Assets

Building on foundational approaches, these specialized methods delve into the distinct aspects of software assets by focusing on specific revenue streams and cost efficiencies. These techniques work alongside primary valuation methods to highlight the unique financial drivers tied to software.

Relief from Royalty Method

The Relief from Royalty Method (RRM) estimates the cost savings a company enjoys by owning an asset instead of licensing it. As Antonella Puca from the CFA Institute explains:

"Owning an intangible asset means the underlying entity doesn't have to pay for the privilege of deploying that asset."

This method blends market data - like royalty rates from comparable licenses - with income forecasts, such as projected revenues and discounted cash flows. The process involves forecasting revenue, applying a market-based royalty rate, estimating the asset's useful life, and discounting the expected royalty savings. Analysts often turn to resources like KtMINE or Royalty Source, or review SEC filings from similar companies, to determine reliable royalty rates. Additionally, a thorough RRM valuation factors in tax savings from asset amortization. A key challenge with this method lies in finding precise comparables, given the unique nature of proprietary software.

While RRM focuses on licensing cost savings, the Multi-Period Excess Earnings Method zeroes in on the extra earnings generated by a core intangible asset.

Multi-Period Excess Earnings Method

The Multi-Period Excess Earnings Method (MPEEM) isolates the cash flows driven by a company's primary intangible asset, making it particularly suitable for assets like proprietary software or customer relationships that heavily influence a company's value. Paul Vogt from PCE Companies puts it succinctly:

"In essence, you're valuing what's left, the 'excess' earnings generated by your key intangible asset."

This method calculates excess earnings by subtracting "contributory asset charges" (CACs) - returns attributed to supporting assets such as working capital, equipment, and secondary intangibles - from the total business earnings. For software-related customer assets, historical attrition rates (e.g., a 25% annual rate) are factored in to ensure the valuation reflects the current customer base. The discount rate is adjusted to include a risk premium above the company's Weighted Average Cost of Capital, accounting for the specific risks tied to the intangible asset. Additionally, the Section 197 tax amortization benefit - allowing the buyer to amortize the purchase price over 15 years - is incorporated into the valuation.

While these methods focus on savings and earnings, the With and Without Method takes a different approach by comparing value under alternative scenarios.

With and Without Method

The With and Without Method (WWM) evaluates the difference in a business's value when an asset is included versus when it is absent. Though often used for non-compete agreements, it is also effective for assessing the impact of proprietary software or algorithms on overall earnings. The incremental value of the asset is determined by comparing two discounted cash flow models - one with the asset in place and one without it.

To apply this method, financial projections are made for both scenarios. Free cash flows are calculated by subtracting expenses and reinvestments from revenues, then discounted to their present value. The difference between the two models reveals the asset's incremental value. Adjustments may be needed when there’s uncertainty about replicating the asset, such as the risk of competitors developing a similar feature. Lastly, the present value of tax savings from amortizing the asset over its useful life is added to the calculation. This approach is particularly useful for modeling potential revenue declines or cost increases if proprietary technology were replaced with a generic alternative.

sbb-itb-97ecd51

Challenges in Valuing Software Intangibles

Determining the value of software intangibles is no easy task. One major hurdle is the subjective nature of valuation - how much an asset is worth often depends on the buyer's portfolio and market position, making the process inherently complex. For early-stage software, the challenge grows as predicting future value becomes tricky due to uncertainties around intellectual property (IP) maturity and its remaining useful life.

Technology obsolescence adds another layer of difficulty. As the World Intellectual Property Organization (WIPO) explains:

Current and future value is determined by many factors, such as the risk of obsolescence, maturity of the IP, and expected development needs.

A survey by the Financial Reporting Council of 20 major acquisitions highlights this issue. It found that only one-third of the purchase price was allocated to recognized intangible assets, while the remaining two-thirds were classified as goodwill. Shân Kennedy, an independent expert in IFRS and valuation, notes:

The seemingly low amount allocated to intangible assets suggests that companies are omitting to identify all their acquired intangibles.

This shortfall often occurs because, under standards like IAS 38, software must meet strict criteria - it needs to be "separable" (capable of being licensed or sold independently) or legally secured - to qualify as a distinct intangible asset.

Market volatility further complicates the picture. Discounted cash flow (DCF) models, often used in valuations, struggle with unreliable growth projections. Thomas Smale, CEO of FE International, explains:

The multiple for private firms is generally discounted by a percentage that can scale with changes to public markets.

When public SaaS valuations drop during market downturns, private software companies often see their valuation multiples shrink as well.

Scalability concerns are another key factor. The SaaS model, while promising profit growth as businesses expand, depends entirely on the assumption that the software can scale to meet those forecasts. However, technical debt - caused by quick fixes - can lead to expensive rework and reduced value. Additionally, when a software's development heavily relies on its owner, replacement costs rise, and the pool of potential buyers narrows. These challenges underscore the need for combining multiple valuation methods to get a clearer picture.

Using Hybrid Valuation Approaches

Given the rapid pace of technological change and the complexities involved, relying on a single valuation method is often insufficient. Instead, blending multiple approaches provides a more balanced view. Appraisers frequently combine income-based methods with market data to validate their conclusions.

Sensitivity analysis plays a crucial role in hybrid approaches. By testing how different assumptions - like projections, discount rates, or useful life - impact valuation, appraisers can better understand potential outcomes. For high-risk or volatile intangibles, Monte Carlo simulations offer a way to account for uncertainty. These statistical models generate a range of possible outcomes, providing a more nuanced view than a single-point estimate.

Scott Weingust, Managing Director at Stout, highlights the importance of this approach when discussing patents:

In most cases related to patents, cost bears little relationship to value as it does not reflect the earnings potential of the subject patent asset.

Since development costs rarely align with market value, combining cost, income, and market approaches often yields a more reliable result. For software assets, this means incorporating insights from both technical and market perspectives. Technology transfer professionals, working alongside IP valuation experts, can ensure that hybrid methods account for competitive positioning and longevity. Without this collaboration, even the most detailed DCF analyses may fall short.

Applying Industry Multiples

Industry-specific revenue and EBITDA multiples serve as critical benchmarks for software valuations, especially for companies without a long revenue history. The right multiple depends on factors like the company's size and business model. For SaaS businesses valued under $2 million, multiples typically range from 5.0x to 7.0x Seller Discretionary Earnings (SDE), while companies valued above $2 million often see multiples between 7.0x and 10.0x.

High-growth SaaS companies often rely on revenue multiples instead of earnings-based metrics. This is because heavy reinvestment in growth can leave them with minimal current EBITDA. However, as Thomas Smale warns:

Measuring revenue makes sense for a growing SaaS valuation, but it is very important to note that this valuation philosophy is entirely based on growth.

If growth slows during market downturns, revenue-based valuations can falter, as they assume continued profit expansion that may not materialize.

The Rule of 40 has become a popular benchmark for SaaS businesses. This rule states that a healthy company's combined revenue growth rate and profit margin should equal at least 40%. For instance, a company growing at 30% annually should maintain profit margins of at least 10% to meet this threshold.

| Growth Rate | Average Revenue Multiple | Cash Burn Tolerance | Market Size Impact |

|---|---|---|---|

| 0-20% | 5-8x | Low | Moderate |

| 20-50% | 8-12x | Medium | Significant |

| 50%+ | 12-20x+ | High | Major |

Monthly Recurring Revenue (MRR) often commands a premium, sometimes valued at twice the rate of other revenue streams, due to its predictability and scalability. This distinction is crucial when applying industry multiples, as the composition of revenue directly influences which benchmarks are most appropriate.

Conclusion

Valuing intangible assets is a critical step in making informed acquisition and investment decisions. In software transactions, where tangible assets often hold little to no value, the entire purchase price typically reflects intangible assets and goodwill. Research indicates that goodwill alone accounts for approximately two-thirds of the purchase price, leaving only one-third allocated to specific intangible assets. This highlights the pressing need for thorough valuation practices. As Shân Kennedy, an independent expert in IFRS and valuation, aptly states:

Accounting for goodwill and intangible assets is critical to an understanding of the transaction.

Failing to conduct a comprehensive valuation of acquired intangibles can lead to overpaying and missing out on strategic opportunities.

Proper valuation is not just about ensuring transaction accuracy - it’s also a cornerstone for effective long-term planning. Employing multiple valuation methods to cross-check results enhances reliability and confidence in the outcomes. Scott Weingust, Managing Director at Stout, underscores this by noting:

In most cases related to patents, cost bears little relationship to value as it does not reflect the earnings potential of the subject patent asset.

Accurate valuations extend beyond the transaction itself. They play a key role in broader strategic goals, such as securing financing, attracting investors, and providing a foundation for legal settlements. Additionally, they serve as a reasonableness check, ensuring that the price paid aligns with the strategic importance of assets like technology or customer relationships, as highlighted by company directors. For those navigating the complexities of software acquisitions, mastering these valuation principles isn’t optional - it’s the difference between a strategic success and a costly misstep.

FAQs

How do intangible assets affect the valuation of software companies?

Intangible assets are a significant piece of the puzzle when it comes to valuing software companies. These include things like intellectual property, proprietary technology, and brand equity - assets that drive revenue, improve efficiency, and create competitive edges. Yet, traditional accounting often struggles to reflect their true value, which can lead to these companies being undervalued.

Assessing these assets requires a focus on how they contribute to the company’s future earnings and market standing. For tangible intangibles like patents or software licenses that can be sold or used as collateral, market-based valuation methods are typically used. On the other hand, for assets that are harder to separate - like brand reputation - valuation often considers the entire enterprise value. This is usually done through approaches like discounted cash flow models or earnings multiples. A solid understanding of these intangibles is essential for making smart investment choices and evaluating software companies accurately, especially during acquisitions or financial reporting.

What makes valuing software intangible assets challenging using common valuation methods?

Valuing intangible assets like intellectual property, patents, and brand equity in software companies is no easy task. These assets are unique and often tricky to quantify. Take the income approach, for instance - it relies on projecting future cash flows. Sounds straightforward, right? Well, not when you factor in rapid technological shifts, unpredictable market trends, and the challenge of estimating long-term profitability. The future in tech can be murky, making these projections anything but simple.

Then there’s the market approach, which looks to comparable market transactions to determine value. The problem? Comparable transactions are often hard to find in the software world. Without similar benchmarks, arriving at a reliable market value becomes a guessing game.

Lastly, the cost approach bases value on development or replacement costs. While this might seem logical, it doesn’t always capture the full picture. For example, software with steep development costs but little market interest could end up overvalued. On the flip side, software that’s strategically vital but inexpensive to replace might be undervalued.

Adding to the complexity is the fast-paced nature of the software industry, where innovation and obsolescence are constant. To tackle these challenges, a mix of valuation methods and expert judgment is often the best bet for arriving at an accurate assessment.

What makes the Rule of 40 important for valuing SaaS companies?

The Rule of 40 is an essential metric for evaluating SaaS companies, offering a balanced perspective on growth and profitability. It allows investors and analysts to gauge a company's financial health and operational efficiency, particularly in industries where intangible assets - like intellectual property, patents, and brand equity - hold significant value.

This metric combines a company's revenue growth rate and profit margin, ensuring businesses strike the right balance between rapid expansion and long-term stability. For software companies, where intangible assets heavily influence valuations, maintaining this equilibrium is especially critical.