Codely v2.0 public release is here

Lorem ipsum dolor sit amet, consectetur adipiscing elit lobortis arcu enim urna adipiscing praesent velit viverra sit semper lorem eu cursus vel hendrerit elementum morbi curabitur etiam nibh justo, lorem aliquet donec sed sit mi dignissim at ante massa mattis.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potent i

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

What has changed in our latest release?

Vitae congue eu consequat ac felis placerat vestibulum lectus mauris ultrices cursus sit amet dictum sit amet justo donec enim diam porttitor lacus luctus accumsan tortor posuere praesent tristique magna sit amet purus gravida quis blandit turpis.

All new features available for all public channel users

At risus viverra adipiscing at in tellus integer feugiat nisl pretium fusce id velit ut tortor sagittis orci a scelerisque purus semper eget at lectus urna duis convallis. porta nibh venenatis cras sed felis eget neque laoreet suspendisse interdum consectetur libero id faucibus nisl donec pretium vulputate sapien nec sagittis aliquam nunc lobortis mattis aliquam faucibus purus in.

- Neque sodales ut etiam sit amet nisl purus non tellus orci ac auctor

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

- Mauris commodo quis imperdiet massa tincidunt nunc pulvinar

- Adipiscing elit ut aliquam purus sit amet viverra suspendisse potenti

Coding collaboration with over 200 users at once

Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque. Velit euismod in pellentesque massa placerat volutpat lacus laoreet non curabitur gravida odio aenean sed adipiscing diam donec adipiscing tristique risus. amet est placerat in egestas erat imperdiet sed euismod nisi.

“Nisi quis eleifend quam adipiscing vitae aliquet bibendum enim facilisis gravida neque velit euismod in pellentesque massa placerat”

Real-time code save every 0.1 seconds

Eget lorem dolor sed viverra ipsum nunc aliquet bibendum felis donec et odio pellentesque diam volutpat commodo sed egestas aliquam sem fringilla ut morbi tincidunt augue interdum velit euismod eu tincidunt tortor aliquam nulla facilisi aenean sed adipiscing diam donec adipiscing ut lectus arcu bibendum at varius vel pharetra nibh venenatis cras sed felis eget dolor cosnectur drolo.

The SBA 504 loan is a financing program tailored for small and medium-sized businesses (SMBs) to fund long-term investments in fixed assets like real estate, equipment, and facility improvements. With loans up to $5.5 million, repayment terms of up to 25 years, and fixed interest rates, it’s designed to support business growth while preserving cash flow. Borrowers benefit from a low down payment of 10%, although this may increase for startups or special-use properties.

Key use cases include:

- Purchasing Commercial Real Estate: Covers land, buildings, and improvements with a 10% down payment and a job creation requirement (1 job per $90,000 of SBA funds).

- Constructing or Upgrading Facilities: Funds new builds, expansions, and upgrades, including energy-efficient projects.

- Acquiring Machinery and Equipment: For durable assets with a 10+ year lifespan, like manufacturing machinery, with a 10% down payment.

- Business Acquisitions: Supports acquisitions involving fixed assets, requiring 10%-20% down depending on the business type.

- Refinancing Existing Debt: Replaces high-interest loans tied to fixed assets, offering long-term rate stability.

This program is ideal for SMBs looking to invest in their growth while maintaining financial flexibility. Below, we explore these use cases in detail, including eligibility, costs covered, and job creation requirements.

What Can I Use an SBA 504 Loan For?

1. Purchasing Commercial Real Estate

The SBA 504 loan is a powerful tool for financing the purchase of commercial real estate. It can be used for buying existing properties, land, new construction, and even property improvements like upgrading facilities, utilities, parking areas, or landscaping. Let’s break down the specifics of what this financing option covers.

Eligible Project Costs Financed

One of the standout features of the SBA 504 loan is its ability to cover more than just the purchase price. It also finances soft costs like appraisals, environmental studies, architectural fees, title work, surveys, and closing costs. This means less upfront cash is needed at closing compared to traditional loans, where these expenses often have to come out of pocket.

Down Payment Requirements

The SBA 504 loan requires a down payment of just 10%, significantly lower than the 20–30% typically required for conventional commercial loans. However, the down payment increases to 15% for startups and 20% for special-use properties. The financing structure is split into three parts: 50% from a third-party lender, 40% from a Certified Development Company (CDC), and 10% from the borrower.

Job Creation Mandates

The program also includes a job creation requirement, which aims to support local employment. Borrowers must create one job for every $90,000 of SBA-financed funds. This mandate underscores the program’s goal of fostering economic growth within communities.

Suitability for SMB Buyers

The SBA 504 loan is particularly appealing to small and medium-sized businesses (SMBs) that need a stable, operational base. The program mandates owner-occupancy of at least 51% for existing buildings and 60% for new construction. This ensures the property is used for business operations rather than as an investment.

The low down payment (as little as 10% for owner-occupied properties) and long-term, fixed interest rates help SMBs preserve their working capital for other business needs.

"Your down payment may be as low as 10%, which can preserve cash for your business" - Western Alliance Bank.

2. Constructing or Improving New Facilities

When it comes to building new facilities or upgrading existing ones, SBA 504 loans provide funding for ground-up construction, expansion, conversions, and modernization projects. These loans are tailored for businesses looking to scale their operations, offering a range of possibilities to suit different needs.

What Costs Can Be Financed?

SBA 504 loans cover a wide array of project costs, including:

- Land acquisition

- Grading, drainage, and site improvements (such as streets, access roads, and parking lots)

- Utilities and landscaping (curbs and sidewalks)

Energy-efficient upgrades are also eligible, as long as they’re supported by an independent audit or engineering report. Additionally, the loans can include soft costs like appraisals, surveys, title searches, attorney’s fees, and zoning or permitting expenses.

Down Payment Details

For most projects, the down payment is set at 10%. However, this increases to 15% for startups or properties considered "special purpose" (like hotels or car washes). If both conditions apply, the down payment rises to 20%.

For new construction, there’s a unique occupancy requirement: borrowers must occupy at least 60% of the facility immediately and reach 80% occupancy within 10 years. This stipulation sets construction projects apart from standard real estate purchases.

Job Creation Requirements

To qualify for SBA 504 funding, projects must create or retain one job for every $90,000 of SBA-backed funds. Small manufacturers and energy-related projects may have different thresholds or qualify through public policy objectives, such as supporting rural development.

Why It’s a Smart Choice for SMBs

For small and mid-sized businesses (SMBs), the terms of SBA 504 loans make them an attractive option. Low down payments and the ability to finance fees and closing costs help reduce upfront expenses, allowing businesses to preserve working capital for other priorities.

"With low down payments (as little as 10%), financing of fees and closing costs, and no balloon payments, the 504 program is an attractive option for... business owners who want to conserve their working capital." - UCEDC

The SBA-backed portion of the loan typically caps at $5 million but can go up to $5.5 million for small manufacturers or energy-efficient projects. This flexibility makes SBA 504 loans a practical solution for SMBs aiming to grow without overextending their resources.

3. Acquiring Long-Term Machinery and Equipment

SBA 504 loans are a great option for financing the purchase of machinery and equipment, provided the assets have a minimum useful life of 10 years. This requirement ensures the loan is used for long-term business growth rather than short-term operational needs. Much like other fixed asset investments, machinery and equipment purchased through the 504 program are meant to support long-term operations.

Eligible Project Costs Covered

The SBA 504 loan covers more than just the purchase price. It also includes transportation, installation, and soft costs like legal fees and appraisals. However, the equipment must generally be permanently installed or fixed at a specific location. Examples of eligible assets include manufacturing machinery, printing presses, and AI-enabled production equipment.

That said, some costs are not covered. These include working capital, inventory, and intangible assets like software, cloud services, or intellectual property. Only minor furniture expenses that are deemed essential may qualify.

Down Payment Requirements

For established businesses, the standard down payment is 10%. If your business has been operating for less than two years, the down payment increases to 15%. For special-purpose equipment, the requirement also rises to 15%, and if you're both a startup and purchasing special-purpose assets, you'll need to put down 20%. This tiered structure aligns with the SBA's focus on job creation and responsible repayment.

Job Creation Mandates

When using SBA funds to purchase equipment, businesses are required to create or retain one job for every $90,000 borrowed. For small manufacturers and energy-related projects, the thresholds may differ, and alternative public policy goals - such as rural development or energy efficiency - can be considered if the standard job creation requirement isn't met.

Why This Works for SMB Buyers

Equipment projects financed under the SBA 504 program typically come with a 10-year repayment term and fixed interest rates (5.65% as of December 2025). Loan amounts are capped at $5 million, or $5.5 million for manufacturing or energy-efficient projects. Fees generally range from 2% to 3%.

"The SBA 504 Loan Program is designed to help growing businesses to expand and create new jobs by providing long-term financing for... the purchase of major equipment and machinery." – UCEDC

For small and medium-sized businesses, the 504 loan structure offers predictable payments and helps preserve working capital. This makes it an attractive alternative to traditional equipment financing, which often comes with shorter terms and higher overall costs. However, borrowers should be aware of the longer closing timeline - typically 30 to 90 days - due to the multi-party approval process involving the CDC and SBA.

sbb-itb-97ecd51

4. Business Acquisitions and Expansions

SBA 504 loans aren't just for fixed asset purchases - they also support business acquisitions and expansions when substantial fixed assets are involved. These loans can finance projects that include owner-occupied real estate or long-term machinery, much like those for purchasing property or constructing facilities. However, the program doesn't cover working capital, inventory, or speculative real estate investments. Occupancy requirements remain 51% for existing buildings and 60% for new construction .

Eligible Project Costs Financed

A 504 loan can cover a range of costs, including the purchase price, new construction, renovations, and site improvements . Even soft costs - like appraisal fees, legal expenses, and title insurance - can be included in the financing . Modernization efforts, such as upgrading facilities to meet health and safety standards or integrating robotics, are also eligible. For machinery or equipment to qualify, it must have at least 10 years of useful life remaining .

Down Payment Requirements

The down payment structure for acquisitions and expansions mirrors that of fixed asset financing. Established businesses operating for two or more years need a 10% down payment . Startups or businesses with new ownership must put down 15% . If the project involves a special-use property - like a hotel, cold storage facility, or winery - an additional 5% is required. For example, a startup acquiring a special-use property would need a 20% down payment. This is still more affordable compared to conventional commercial loans, where lenders often demand 20% to 30% upfront .

Job Creation Mandates

SBA 504 projects must create or retain one job per $90,000 of financing. Small manufacturers get a bit more leeway, requiring one job per $140,000. If your project doesn't meet these job creation numbers, you might still qualify by meeting public policy goals. These could include promoting rural development, supporting veteran-owned businesses, or improving energy efficiency by at least 10%. In such cases, the Certified Development Company (CDC) overseeing the loan must maintain an average job creation rate across its portfolio to approve these exceptions.

Suitability for SMB Buyers

To qualify, a business must have a tangible net worth under $20 million and an average net income of less than $6.5 million (after taxes) over the last two years . The SBA portion of the loan is typically capped at $5 million but can go up to $5.5 million for manufacturing or energy-efficient projects . Fixed interest rates are tied to U.S. Treasury rates, and total fees are limited to 3% of the loan amount . For SMB buyers actively searching for acquisition opportunities, platforms like Kumo (https://withkumo.com) can help by aggregating business listings that meet SBA 504 loan criteria.

Next, we’ll dive into the pros and cons of these financing options.

5. Refinancing Existing Debt for Fixed Assets

The SBA 504 program offers a refinancing option for existing debt tied to fixed assets like commercial real estate, buildings, or long-term equipment. If you're dealing with high-interest mortgages or balloon payments, refinancing into a 504 loan can lock in a fixed rate for up to 25 years, potentially lowering your monthly payments. This option complements other uses of the SBA 504 program by providing rate stability and improving cash flow.

Eligible Project Costs Financed

Refinancing under the SBA 504 program focuses on maintaining working capital while leveraging the equity in your existing assets. To qualify, your debt must meet specific criteria. The loan being refinanced must have been in place for at least six months and secured by eligible fixed assets - such as land, buildings, machinery, or equipment - for the same period. Additionally, at least 75% of the original loan proceeds must have been used for SBA 504-eligible purposes like acquiring, constructing, or improving fixed assets. Even existing SBA 7(a) loans or other federal debt can be refinanced through this program. For businesses with multiple commercial loans, consolidating them into a single 504 loan can simplify payments. The property involved must also be at least 51% owner-occupied.

One standout feature is the cash-out option, which allows you to access your built-up equity for eligible business expenses. These expenses could include non-owner salaries, rent, utilities, inventory, or even business credit card debt. The maximum loan-to-value (LTV) is generally 90% for straight refinancing, but it decreases to 85% if cash is taken out. As of December 2025, the effective interest rate for a 25-year fixed-rate refinance stood at 5.82%.

Down Payment Requirements

The down payment structure for refinancing makes it a practical option for many businesses. For companies operating for at least two years, the standard down payment is 10%. If you're refinancing real estate, your existing equity in the property can often satisfy this requirement. For businesses less than two years old or for special-purpose properties like hotels or gas stations, the down payment increases to 15%. If both conditions apply, the requirement rises to 20%.

Job Creation Mandates

Refinanced projects must create or retain one job for every $90,000 of financing, or one job per $140,000 for small manufacturers. If these targets aren't met, you may still qualify by meeting public policy goals, such as supporting veteran-owned businesses or achieving at least a 10% improvement in energy efficiency.

Suitability for SMB Buyers

Small and medium-sized businesses (SMBs) that meet standard SBA eligibility guidelines can access SBA-backed portions of loans up to $5.5 million for most projects. Just like when purchasing or constructing fixed assets, refinancing provides SMBs with predictable terms and long-term stability. If you're facing balloon payments or dealing with variable-rate debt, transitioning to a 504 loan can offer long-term rate security while preserving working capital for day-to-day operations. Keep in mind that your business must have been operating for at least two years to qualify.

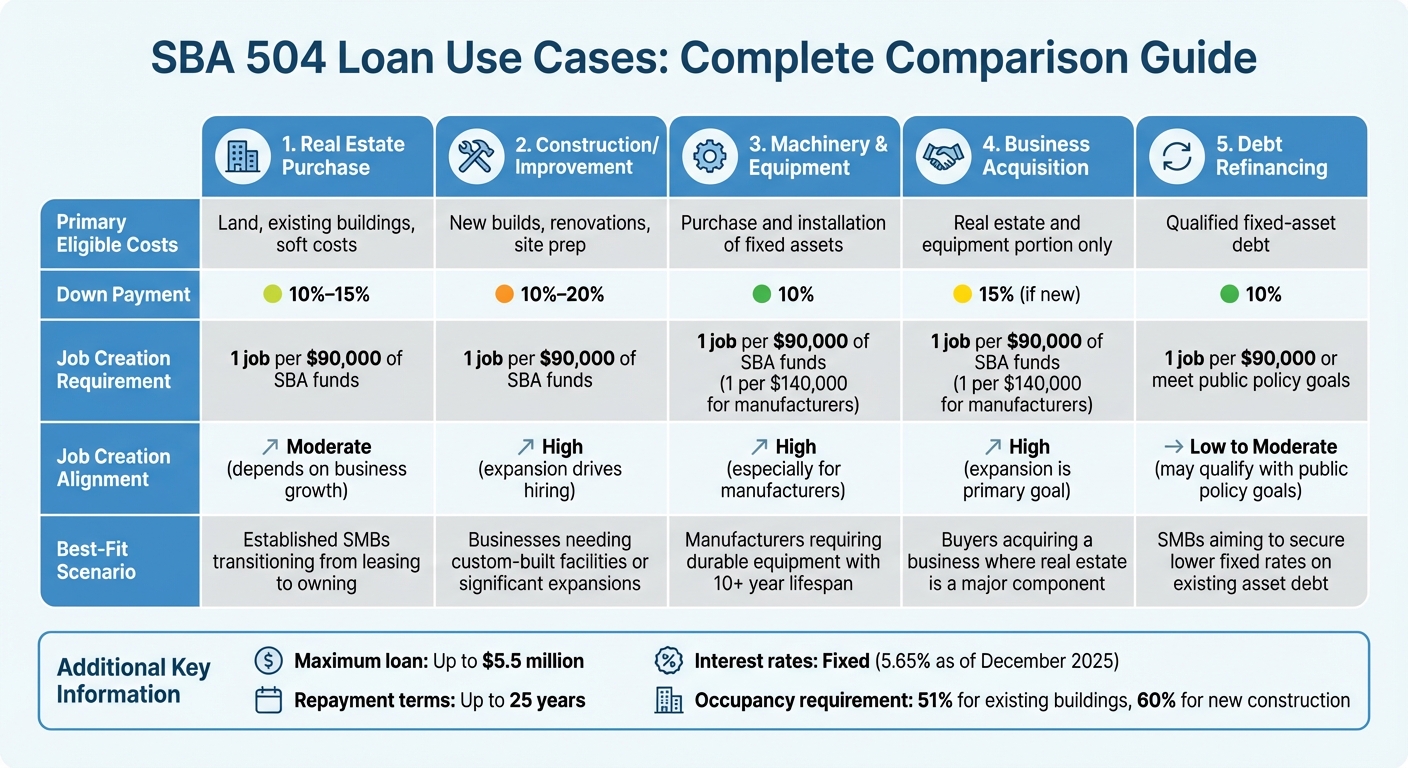

Comparison: Pros and Cons of Each Use Case

SBA 504 Loan Use Cases Comparison: Down Payments, Costs, and Requirements

Each SBA 504 use case comes with its own set of benefits and limitations, shaping how businesses approach their financing strategy. Here's a breakdown of the key factors for each scenario:

| Use Case | Primary Eligible Costs | Down Payment | Job Creation Alignment | Best-Fit Scenario |

|---|---|---|---|---|

| Real Estate Purchase | Land, existing buildings, soft costs | 10%–15% | Moderate; depends on business growth | Established SMBs transitioning from leasing to owning |

| Construction/Improvement | New builds, renovations, site prep | 10%–20% | High; expansion drives hiring | Businesses needing custom-built facilities or significant expansions |

| Machinery & Equipment | Purchase and installation of fixed assets | 10% | High; especially for manufacturers | Manufacturers requiring durable equipment with a 10+ year lifespan |

| Business Acquisition | Real estate and equipment portion only | 15% (if new) | High; expansion is the primary goal | Buyers acquiring a business where real estate is a major component |

| Debt Refinancing | Qualified fixed-asset debt | 10% | Low to Moderate; may qualify with public policy goals | SMBs aiming to secure lower fixed rates on existing asset debt |

This table highlights the main differences between use cases. Let’s dive deeper into the trade-offs and considerations for each.

Cash Flow vs. Flexibility

One of the biggest factors to weigh is the balance between upfront cash requirements and maintaining operational flexibility. For example, real estate purchases and debt refinancing generally require the standard 10% down payment, which helps preserve working capital for daily operations. However, new businesses or those investing in special-use properties may face higher down payments of 15%–20%, which can tighten cash flow during critical growth phases.

Job Creation Requirements

The SBA 504 program emphasizes job creation, which adds another layer of complexity. Construction projects and equipment purchases often align well with the requirement to create one job per $90,000 of SBA funding because they directly expand a company’s capacity. On the other hand, refinancing tends to have a lower impact on job creation and often relies on meeting public policy objectives, like achieving a 10% improvement in energy efficiency.

Equipment Eligibility

When financing machinery or equipment, the assets must have a minimum useful life of 10 years to qualify. This restricts eligibility to durable, long-term investments, making it a strong option for manufacturers but less so for industries with rapidly evolving technology needs.

Limitations on Intangible Assets

It’s important to note that SBA 504 funds cannot be used for intangible assets like goodwill, customer lists, or brand value. If a significant portion of a business acquisition involves intangible assets, you’ll need additional financing, such as an SBA 7(a) loan, to cover those costs.

Refinancing Considerations

For SMBs looking to refinance, there are specific requirements: the debt must be at least two years old, and 85% of the loan proceeds must have been used to finance eligible fixed assets. Refinancing can be a great way to secure lower fixed interest rates, but it’s less impactful in terms of job creation.

This comparison serves as a guide to help SMBs align their financing choices with their broader strategic objectives, ensuring the selected option supports both short-term needs and long-term goals.

Conclusion

Pick the SBA 504 loan option that matches your business’s current needs and future goals. If you're an established small or medium business aiming to transition from renting to owning, this program offers long-term stability with predictable occupancy costs for 20–25 years - all with just a 10% down payment. For businesses focused on acquiring long-term assets, equipment financing is a practical solution. Meanwhile, those planning custom-built facilities can consider construction financing, which conveniently combines land acquisition, construction expenses, and related soft costs into one package.

If you're looking to expand through acquisitions, financing fixed assets like real estate and heavy equipment is possible through SBA 504 loans. For intangible assets, pairing this with SBA 7(a) loans may be necessary. Kumo streamlines this process by consolidating qualifying business listings to simplify your search.

Refinancing existing debt is another option to improve cash flow, allowing you to convert short-term loans into fixed-rate, long-term financing. Just keep in mind that at least 85% of the original financing must have been used for eligible fixed assets. Whether it’s real estate, equipment, or refinancing, the SBA 504 program is designed to support your business’s growth. Align your financing choice with your operational strategy and growth timeline to make the most of these opportunities.

FAQs

What do I need to qualify for an SBA 504 loan?

To be eligible for an SBA 504 loan, your business must operate as a for-profit entity within the United States or its territories and meet specific size requirements set by the SBA. These include having a tangible net worth of less than $20 million and an average net income after taxes of less than $6.5 million over the past two years. The loan is specifically intended for owner-occupied properties, meaning your business must occupy at least 51% of an existing building or 61% of a newly constructed one. It's important to note that these funds cannot be used for purely rental or speculative investments.

Applicants also need to show good character, capable management, a viable business plan, and the financial ability to repay the loan. Additionally, borrowers must align with the SBA’s job-creation or public-policy objectives. For small and medium business buyers interested in acquiring a property or business that qualifies for SBA 504 financing, platforms like Kumo can make the process easier by consolidating listings from different sources, helping you find options that meet these criteria.

How do SBA 504 loans support job creation for small and medium-sized businesses?

SBA 504 loans aim to boost job creation by offering long-term, fixed-rate financing for major fixed assets like commercial real estate, machinery, or equipment. These loans are specifically designed to help small and medium-sized businesses (SMBs) expand their operations and increase their workforce, with eligibility tied to meeting specific job creation or retention goals.

To qualify, businesses generally need to create one new job for every $65,000 of loan funds (or $100,000 for small manufacturers). This makes SBA 504 loans an effective option for companies planning to grow while achieving measurable employment targets. For SMBs exploring acquisition opportunities that align with these requirements, platforms like Kumo can make the process easier by aggregating business listings and identifying options that meet SBA 504 financing criteria and job creation incentives.

Can SBA 504 loans be used to refinance business debt?

Yes, SBA 504 loans can be used to refinance specific types of existing business debt, including qualifying commercial real estate mortgages and other approved loans. The main purpose of refinancing through an SBA 504 loan is to help small business owners lower their monthly payments, enhance cash flow, or secure better loan terms.

To be eligible, the debt being refinanced must align with SBA requirements, such as being connected to eligible fixed assets like real estate or equipment. This option can be particularly helpful for businesses aiming to streamline their finances while focusing on sustainable growth.